Is Jerome Powell Hinting at a September Rate Cut?

Is Jerome Powell Hinting at a September Rate Cut?

The Truth Revealed!

Jerome Powell’s first appearance before Congress this week didn’t indicate that the Fed was preparing to cut rates in September, but it didn’t discount the possibility either. His prepared statement was essentially a repeat of comments he’s made in the past week or so - that he’s encouraged that the path of inflation is moving in the right direction, but still wants to see more data that would confirm it. Some of that data could come later this week in the form of the June CPI and PPI readings, but it seems that we’re again heading in this disinflationary direction based on recent trends. At this point, I think there’s enough momentum building to suggest that a September rate cut is probably more likely than not at this point, but my main concern is that this is no longer just an inflation story. It’s an economic growth story.

We’ve seen evidence that consumer credit and spending are increasingly becoming concerns in this era of elevated inflation and high interest rates. If the labor market is showing us that it’s slowing down as well, suddenly there’s no obvious catalyst that would support the “higher for longer” narrative. GDP growth slowed substantially in Q1 and the Atlanta Fed’s GDPNow forecast stands at 1.5% for Q2. That doesn’t signal an imminent recession, but it does demonstrate that the economy is slowing down. The unemployment rate is at multi-year highs and the rate of wage growth is at multi-year lows, while initial jobless claims are on the rise. If the Fed wants to get in front of an economic slowdown that is starting to see a lot of evidence supporting it, it probably wants to strongly consider cutting in September in order to avoid a repeat of 2022 where they started adjusting policy rates many months too late. If inflation gets “close enough”, September and December rate cuts probably become the base case scenario.

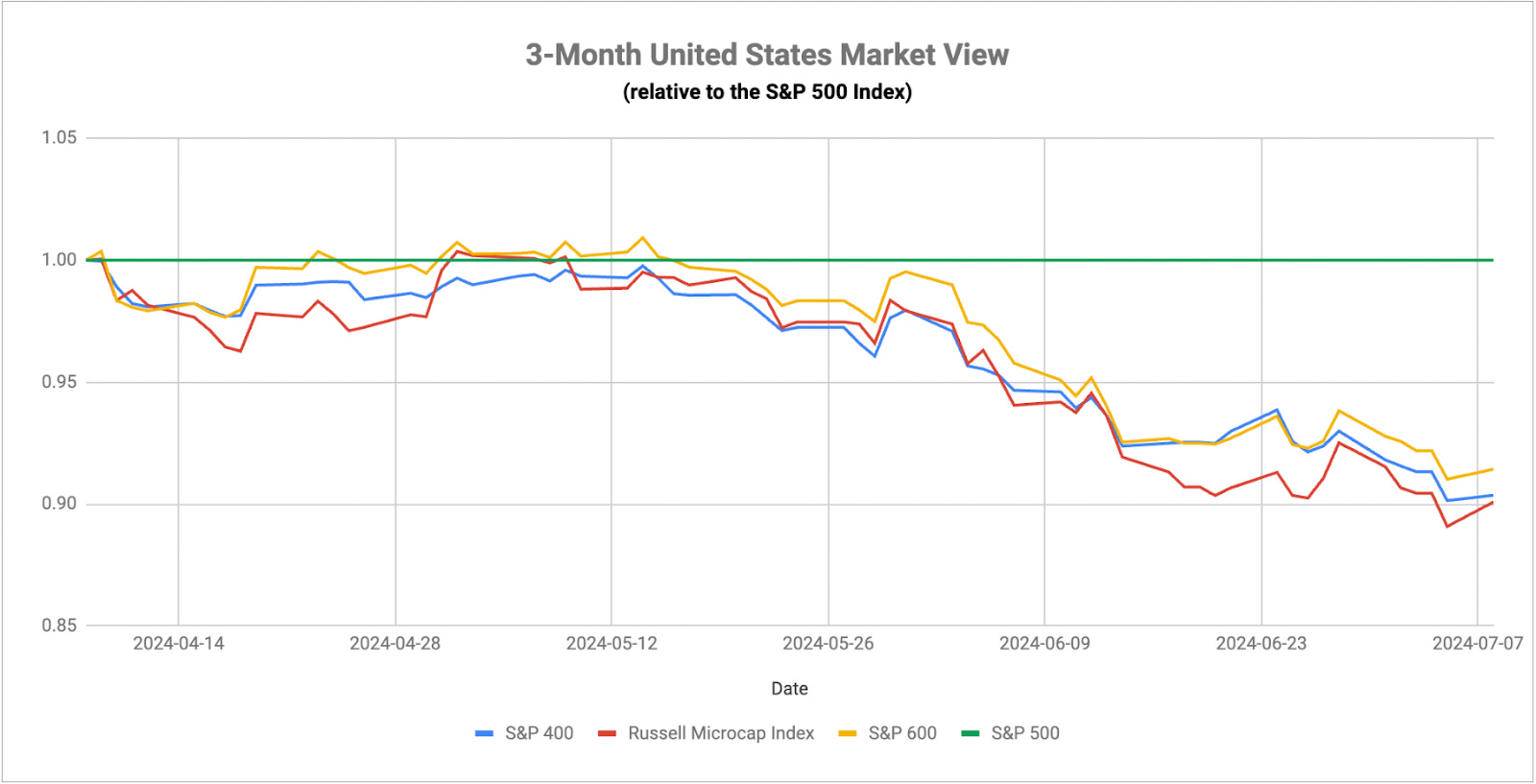

I think some of the best evidence in the financial markets that the U.S. economy is quickly slowing is the behavior of small-caps, as seen in the chart above. I think a lot of investors view the rallies in the S&P 500 and Nasdaq 100 as evidence that the market is strong and the economy is good. The outperformance of just a handful of mega-cap names could also be viewed as a flight to safety trade. If you think about it, it makes sense. If the economy is slowing, you want your money to be invested in companies that are durable and can withstand tough economic environments. What better way to do that than invest in the companies that have generated some of the biggest earnings and revenue growth over the past 1-2 years and are also positioned to benefit from the AI revolution? Why would you want to put your money in more speculative small-caps, many of which are unprofitable to begin with and more prone to volatile market reactions?

Right now, tech and communication services are the only two sectors beating the S&P 500 year-to-date. With long-term Treasury yields trending lower and gold prices trending higher, the composition and performance of the S&P 500 may not be signs of strength. The lack of breadth is a sign of weakness.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.