Strong Bond Market Diversification

Strong Bond Market Diversification

With A Surprisingly Durable Distribution

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

Now that the Fed has officially launched its rate cutting cycle, it’s time to give the broader fixed income space another look. A lot of investors have felt satisfied leaving their cash parked in a 5% yielding T-bill or money market account without any risk. Since the Fed already cut by 50 basis points and has many more cuts in its plans, those previously juicy yields are going to start shrinking quickly. That means it’s time to give traditional fixed income another look.

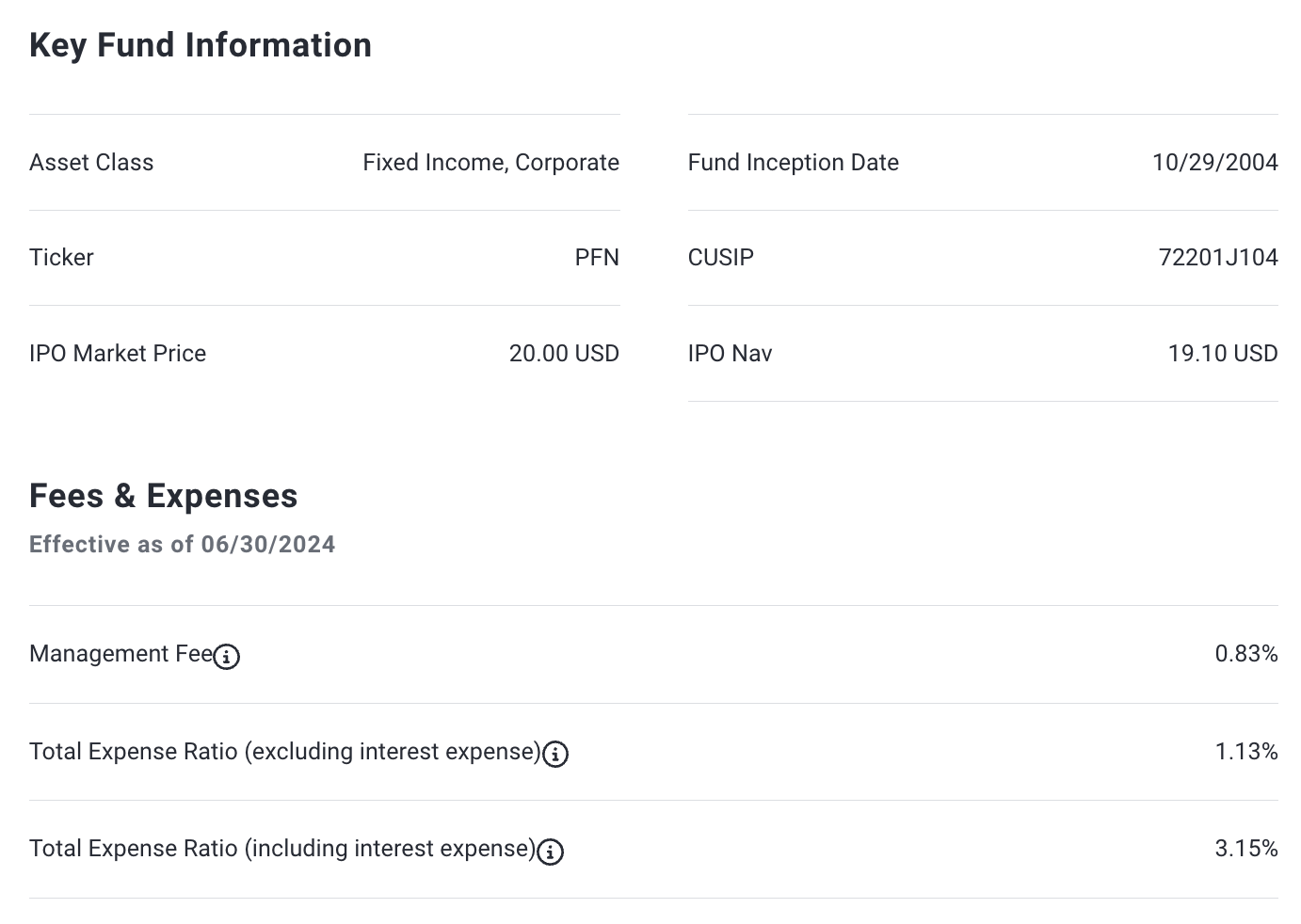

If rates are heading lower, that means bond investors could be in line for some share price appreciation potential in addition to that yield. The PIMCO Income Strategy Fund II (PFN) invests in a diversified mix of government & corporate, investment-grade & non-investment-grade, fixed rate and floating rate notes from around the world. In other words, it’s relatively unconstrained, which could make it the ideal choice for this environment. Being able to tactically shift to where the opportunity is could help maximize total return while limiting downside risk exposure.

Fund Background

PFN employs a multi-sector approach seeking high current income consistent with the preservation of capital. It invests in a diversified portfolio of floating and/or fixed-rate debt instruments. The fund has the flexibility to allocate assets in varying proportions among floating- and fixed-rate debt instruments, as well as among investment grade and non-investment grade securities. The fund’s duration will normally be in a low to intermediate range (zero to eight years). PIMCO also considers capital appreciation and principal preservation through intensive fundamental, macroeconomic, industry and company-specific research. The fund also utilizes leverage in order to enhance yield and total return potential.

The “go anywhere” approach of this fund might be its biggest draw. Its mix of securities across the credit quality spectrum from all around the world give it a diversification that you find in few other fixed income CEFs. Since many funds in this group focus deep into the low quality end of the pool, a fund that maintains a roughly 60/40 split between investment-grade and junk bonds holds particular appeal. Annual turnover is relatively modest at 26%. That means there isn’t a great deal of movement to reposition the portfolio regularly, but I like the flexibility it has to tilt away from potentially troublesome areas of the market.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.