The Most Interesting Week Of The Year

The Most Interesting Week Of The Year

Will The BoJ Matter More Than The Fed?

If you’re a fan of central bank meetings, this is your week! In addition to the Fed announcement on Wednesday, we’ll get policy decisions in Japan, the United Kingdom, China and Brazil. In the United States, a rate cut is effectively a done deal, the only question remaining is whether or not the move will be a quarter-point or a half-point. While 25 basis points might make for a gentler jumping off point, momentum seems to be picking up for a more aggressive 50 basis point cut out of the gate. In my opinion, a quarter-point cut should send the message that an easing of conditions is warranted, but the soft landing narrative is still intact. A half-point move, however, could send the message that the economy is deteriorating and rates need to move lower and faster in order to try to keep it contained. The data certainly warrants the latter, but Powell pays attention to the financial markets and may not want to risk a volatile market reaction, especially with less than two months until the election.

Historically, the start of a rate cutting cycle marks the start of a tougher period for equities. Rate cuts generally coincide with contracting economies or, occasionally, recessions. Where stock prices head from here really depends on whether we slide into recession. If the Fed can manage to pull off the soft landing while normalizing interest rates, there’s precedent for stocks to continue heading higher here. But if current trends continue and the global economy is headed towards recession, it’s entirely reasonable that stocks could fall by 20% or more. The last three recessions in the U.S. have been the COVID pandemic, the financial crisis and the tech bubble. The last “garden variety” recession came back in 1990 and I don’t think we want to look more than three decades in the past for guidance on how things could play out today. We really don’t know how well or how poorly stocks could perform here. While GDP growth and retail sales figures have held up and are fueling the bull case, there’s a lot of damage happening on the credit side. I think that will ultimately win out in the end.

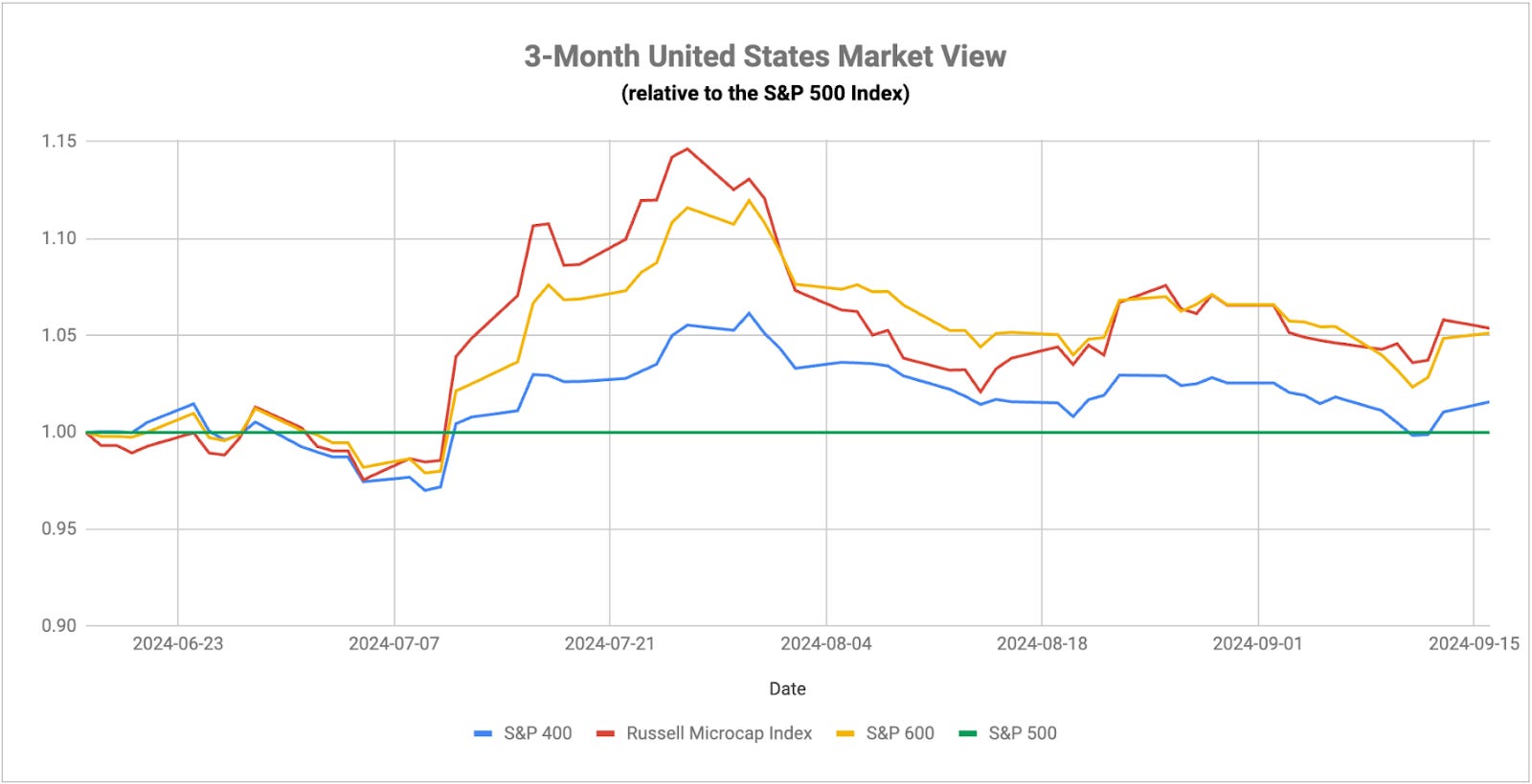

While the S&P 500 is back to all-time highs, it’s important to point out that the broader market is not signaling the same thing. Utilities are still in an uptrend relative to the S&P 500. Treasury yields continue to push lower. Gold is still setting all-time highs. A lot of traditionally risk-off asset classes are still leading the markets here and that strongly suggests that defensive sentiment is still in control. Over the past several trading days, small-caps have been outpacing large-caps by a substantial margin. I don’t view that as a risk-on sign as much as I view it as small-caps receiving a disproportionately bigger benefit from lower interest rates. I think until we see some sustained underperformance from multiple of the utilities/Treasuries/gold trio, I think we have to conclude that risk-off is still in charge here. I suspect this will be a volatile 2nd half of the week and could drive the sentiment we see heading into the stretch run of 2024.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.