This 12% Yield Is Hiding Some Warts

This 12% Yield Is Hiding Some Warts

Atrocious.

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

As conditions start looking less and less favorable for risk assets, investors would do well to start considering alternatives within their portfolios. Bonds, gold or cash usually come to mind first, but convertibles could also work. These are the stock/bond hybrids that possess characteristics of both asset classes. They often provide the income of a bond, but also some of the share price appreciation potential of stocks. That makes them potentially attractive regardless of the macro environment.

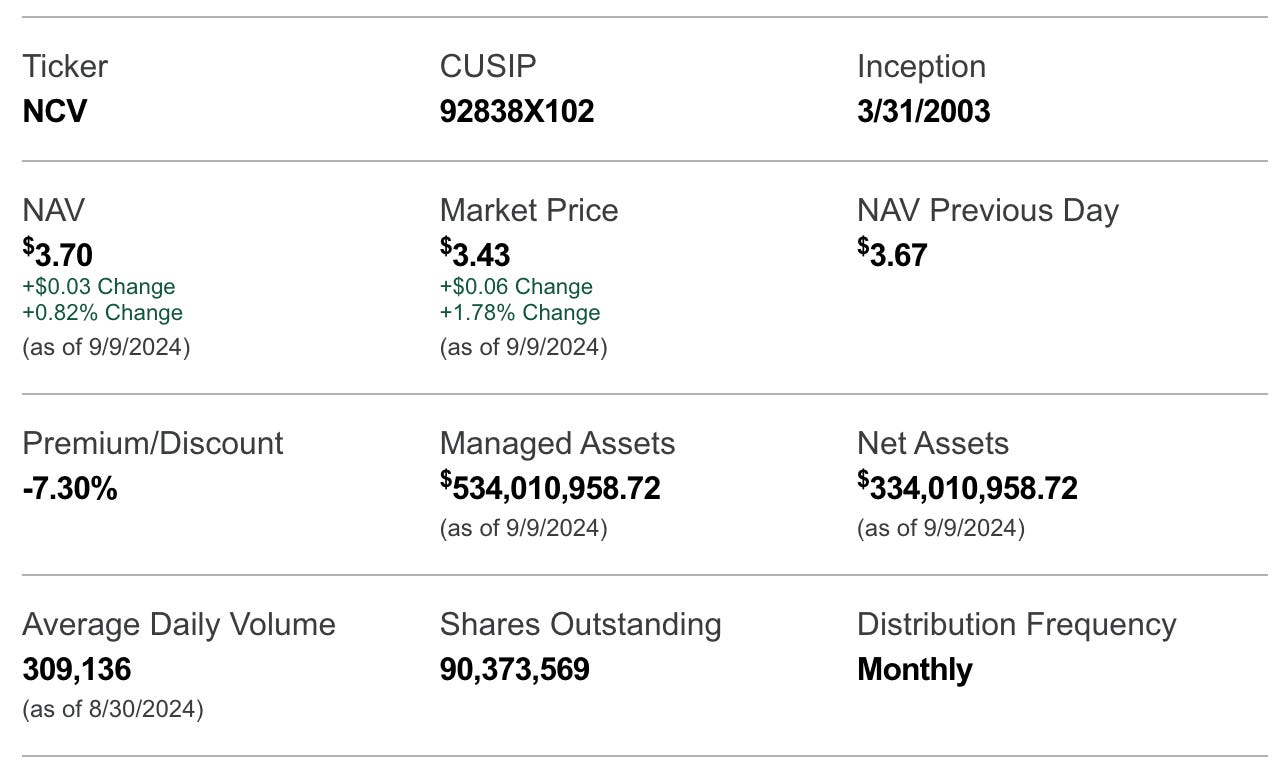

The Virtus Convertible & Income Fund (NCV) combines convertible securities with high yield bonds in order to maximize income potential. While some may find the stock/bond hybrid structure attractive, the risk profile should be the primary concern. The use of leverage along with the relatively high allocation to junk bonds could meet the definition of “wrong place, wrong time”. The yield on this fund is well above 10%, which is the area where investors tend to neglect the risk factors and fall in love with the yield. The composition of the fund strongly suggests that they shouldn’t.

Fund Background

NCV seeks total return through a combination of capital appreciation and high current income. It invests in a diversified portfolio of domestic convertible securities and high yield bonds rated below investment grade. Under normal circumstances, it seeks to invest at least 50% of its total assets in convertible securities, but determines its allocation based on changes in equity prices, changes in interest rates, and other economic and market factors. In searching for investment opportunities, the manager looks for issuers that will successfully adapt to change, exceed minimum credit statistics, and exhibit the most promising operating performance potential. NCV also uses leverage in order to enhance yield and total return potential.

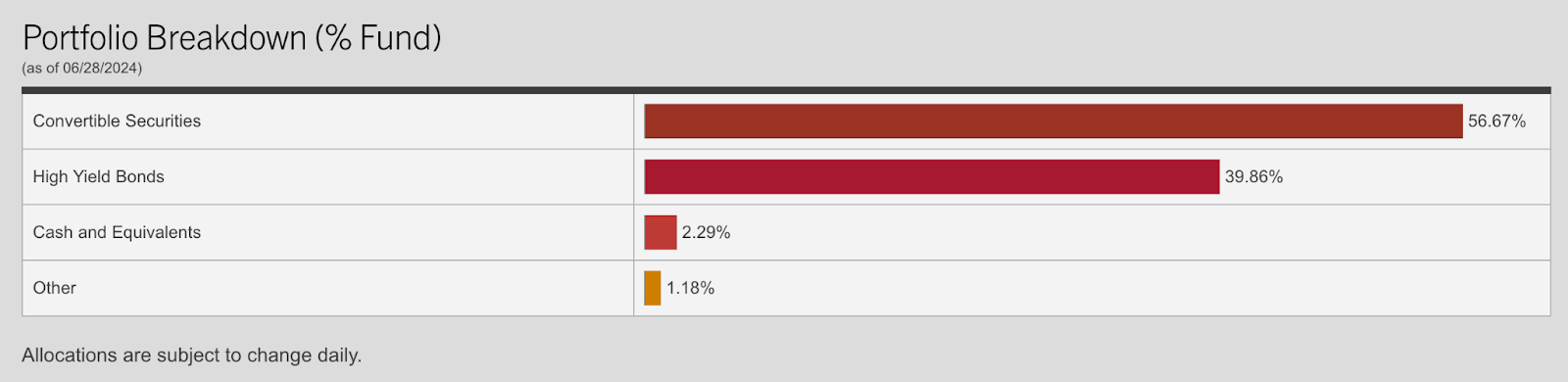

The combination of convertible securities and junk bonds may on the surface seem a little curious, but I think it does help create a reasonable stock/exposure. The convertible piece may offer some equity upside, but yields are traditionally pretty low. Therefore, the pairing with higher-yielding junk bonds makes some sense. If viewed as a fixed income investment, the risk level is high, based on not just the composition of the fund, but the high use of leverage that’s involved, currently at about 37% of managed assets. With a very high distribution yield and low share price, warning flags should go up immediately that the fund is overdistributing, something that we will see is indeed the case as we continue.

NCV by mandate leans towards a heavier weighting in convertibles, but the current 60/40-ish mix of assets represents a relative balance. This could be due to recent outperformance within the junk bond category where investors have found the best returns in recent years even though risk/reward is skewed negatively right now. With Treasury bills yielding around 5%, lower-yielding convertibles may prove not nearly as attractive in this environment. Convertibles have been a below-average performer within the fixed income space going back several years and that could be why we’re seeing a larger emphasis on junk bonds right now.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.