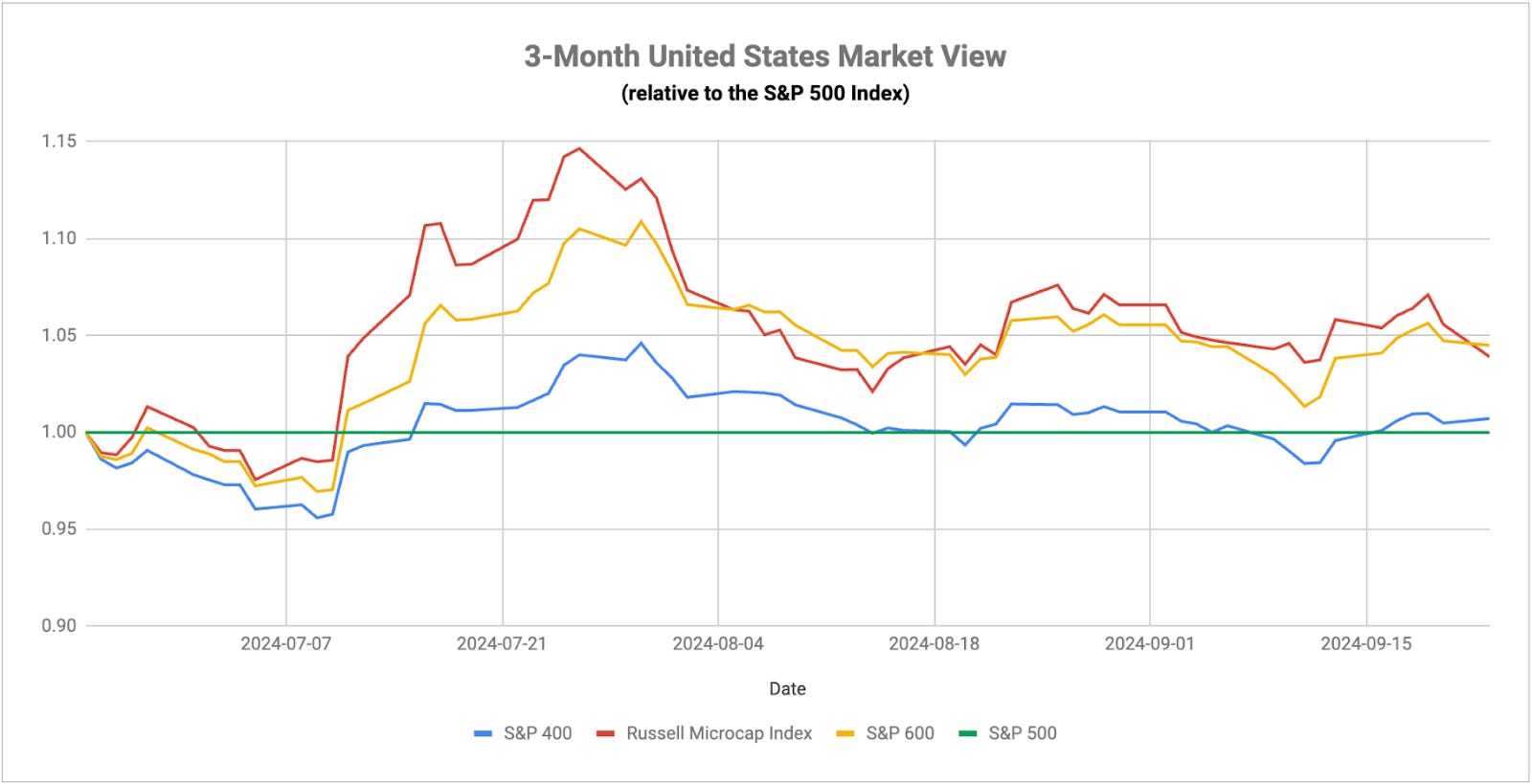

Why Aren't Small-Caps Rallying Despite The 50 Basis Point Cut?

Why Aren't Small-Caps Rallying Despite The 50 Basis Point Cut?

The Biggest Catalysts

The rally that started last week with the Fed’s 50 basis point rate cut looks like it’s trying to carry forward into this week. In the absence of any high level data indicating short-term stress, such as GDP growth or the unemployment rate, the markets seem satisfied in viewing the Fed’s move as a positive development. Historically, rate cuts delivered when conditions are still viewed as positive have resulted in further gains for equities. That’s a short-term effect though. How equities fare in the longer-term will depend on whether the economy is actually in good shape or it’s actually showing signs of deterioration below the surface.

We saw a similar phenomenon back in 2007. In the 4th quarter of that year, when the financial crisis recession is generally accepted to have begun, the GDP growth print was still 2.5% and the unemployment rate was under 5%. The high level data that’s widely watched looked fine, but stresses were also being indicated. Specifically, high yield spreads had been widening in the lead-up to the end of 2007. That, of course, isn’t happening in today’s economy, but it’s not improbable that it’s still coming. Back then, the S&P 500 had already fallen by about 9% at the onset of the recession on its way to falling more than 50% from peak to valley. We may be a bit earlier in that cycle today than we were 17 years, but the signs suggest an eerie similarity.

On the economic side, the manufacturing PMI for August came in below expectations at 47, the lowest reading since June 2023 and marking a continued contraction in the sector. Manufacturing is still a relatively minor subset of the overall economy, but it’s directionally telling in terms of consumer demand and factory activity. With the labor market weakening and consumer confidence falling, it’s confirming the lack of demand we’re currently seeing for goods and other “things”. It’s important to recognize that this isn’t just a local phenomenon either. This is happening globally, most seriously in Japan and China, but in areas of Europe as well. This is perhaps the strongest evidence along with deteriorating credit conditions that demonstrates how not all is well under the surface.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.