2023 Redux

2023 Redux

This Narrow Market Isn't Healthy

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: A REPEAT OF 2023: THIS NARROW MARKET RALLY ISN’T HEALTHY

Technology (XLK) – The Return Of 2023

In 2023, tech stocks were the dominant market sector as growth remained surprisingly strong, yet the Fed was nowhere near lowering interest rates. The past few weeks makes it look like we’re in that position again - positive growth plus “higher for longer”. The problem with this type of market is that leadership is very narrow and that masks the broader weakness that exists beyond the major large-cap averages.

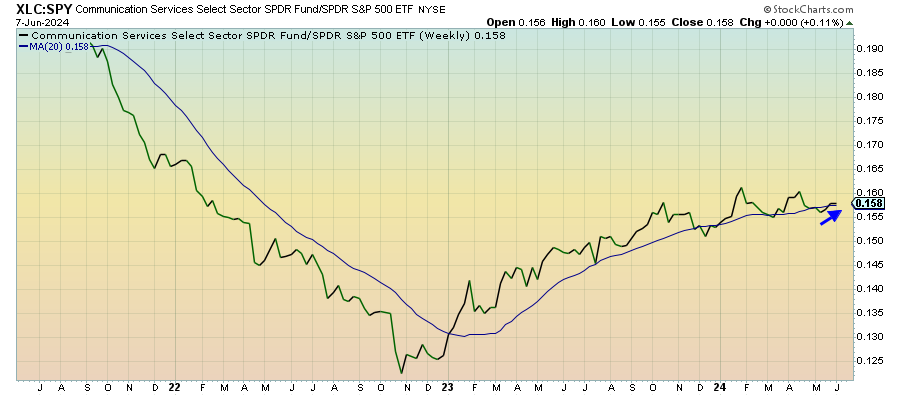

Communication Services (XLC) – Heavy Mag 7 Influence

This sector appeared to be fizzling out relative to the S&P 500, but the re-emergence of tech has been pulling this adjacent sector up with it. There’s a heavy “magnificent 7” influence here again. Facebook dominated the 1st quarter’s returns and Alphabet is driving those from the 2nd quarter. This sector is still quite broadly weak and emphasizes that the consumer discretionary aspect of this group is struggling.

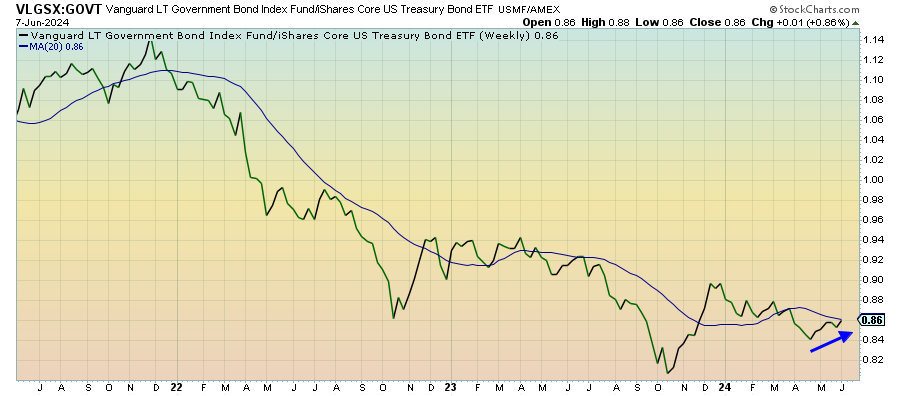

Long Bonds (VLGSX) – Could Be A Volatile Week

Treasuries are making a comeback here and you can see it in long bond outperformance. Yields took a hit last week on the non-farm payroll number and could turn volatile again this week with inflation and the Fed decision. If Powell walks back his multiple rate forecast from earlier this year, which seems more likely than not at this point, we could see a short-term reversal unless investors view it as a reason to migrate to safety assets.

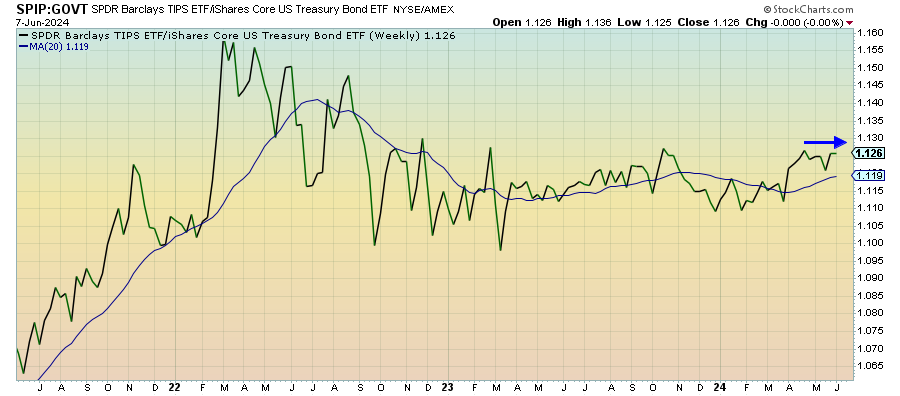

Treasury Inflation Protected Securities (SPIP) – Breakout

Inflation protection has only been of modest interest over the past few months, but that could very much change this week. Not only is the latest monthly inflation report going to drop this week, we’re also going to hear from the Fed and what they think about the path of inflation. I suspect Powell will talk about the dangers of sticky inflation and the central bank’s rate cut expectations will get dialed back. If the message gets delivered strongly enough, it could bring buyers back into TIPS.

Junk Debt (JNK) – Not A Rotation Quite Yet

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.