2024 vs. 2007

2024 vs. 2007

There Are More Similarities Than You Think

For the past many months I’ve talked about how conditions are suggesting the market is vulnerable for a major downturn. The thesis has been that consumer credit conditions have been getting worse, the housing market is topping out and corporate bankruptcies and debt-related stresses are on the rise. Historically, these are the things that are precursors to an economic slowdown or even a recession. I’ve warned about the potential risks that are looming if credit spreads finally blow out (the “credit event”) and how that could cascade into significant declines for risk asset prices.

So far, that hasn’t happened. Even though credit conditions worsen, credit spreads have yet to budge (save for that brief period in August during the yen carry trade unwind). Now that the Fed has started cutting interest rates and is gearing up to add more liquidity to the system, a major credit event may have just become a little less likely in the short-term. That could also mean that a recession will be delayed as well.

Or does it?

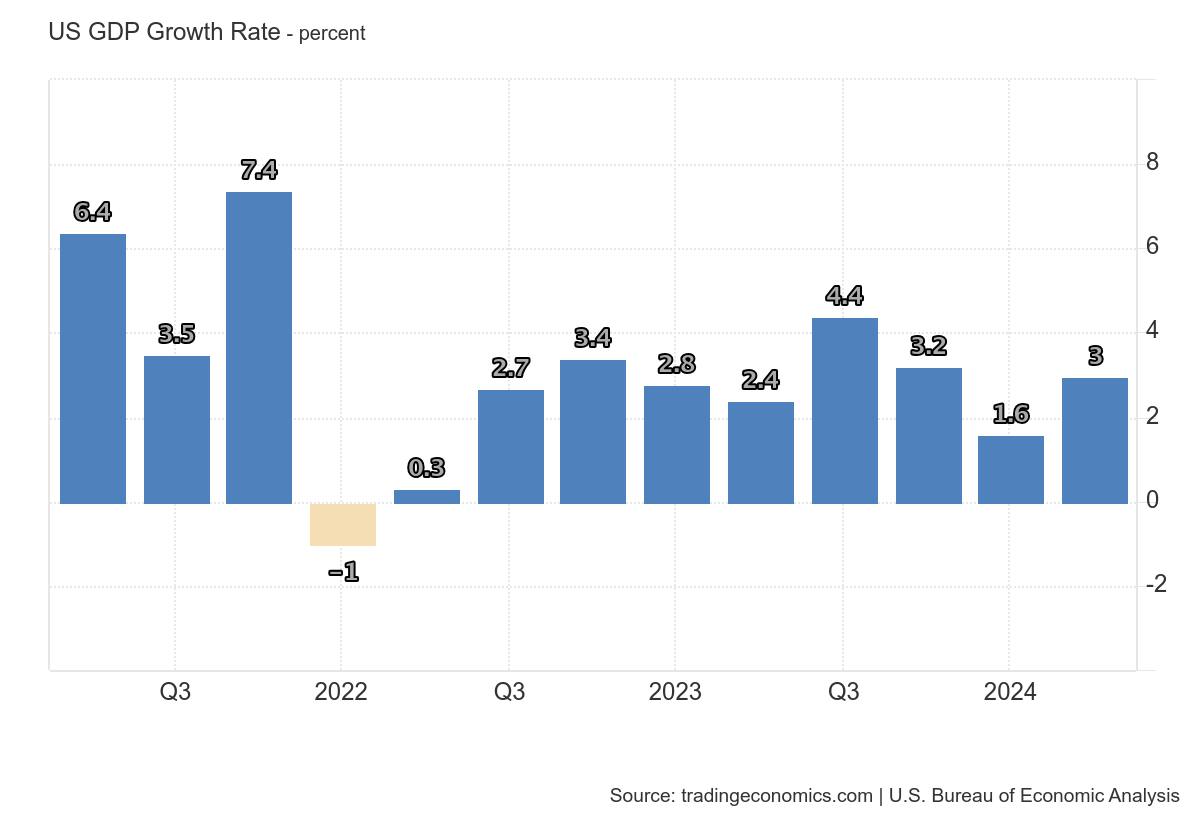

When it comes to the recession argument, the market bulls usually specify a couple of data points. First, the annualized GDP growth rate in the 2nd quarter was 3%.

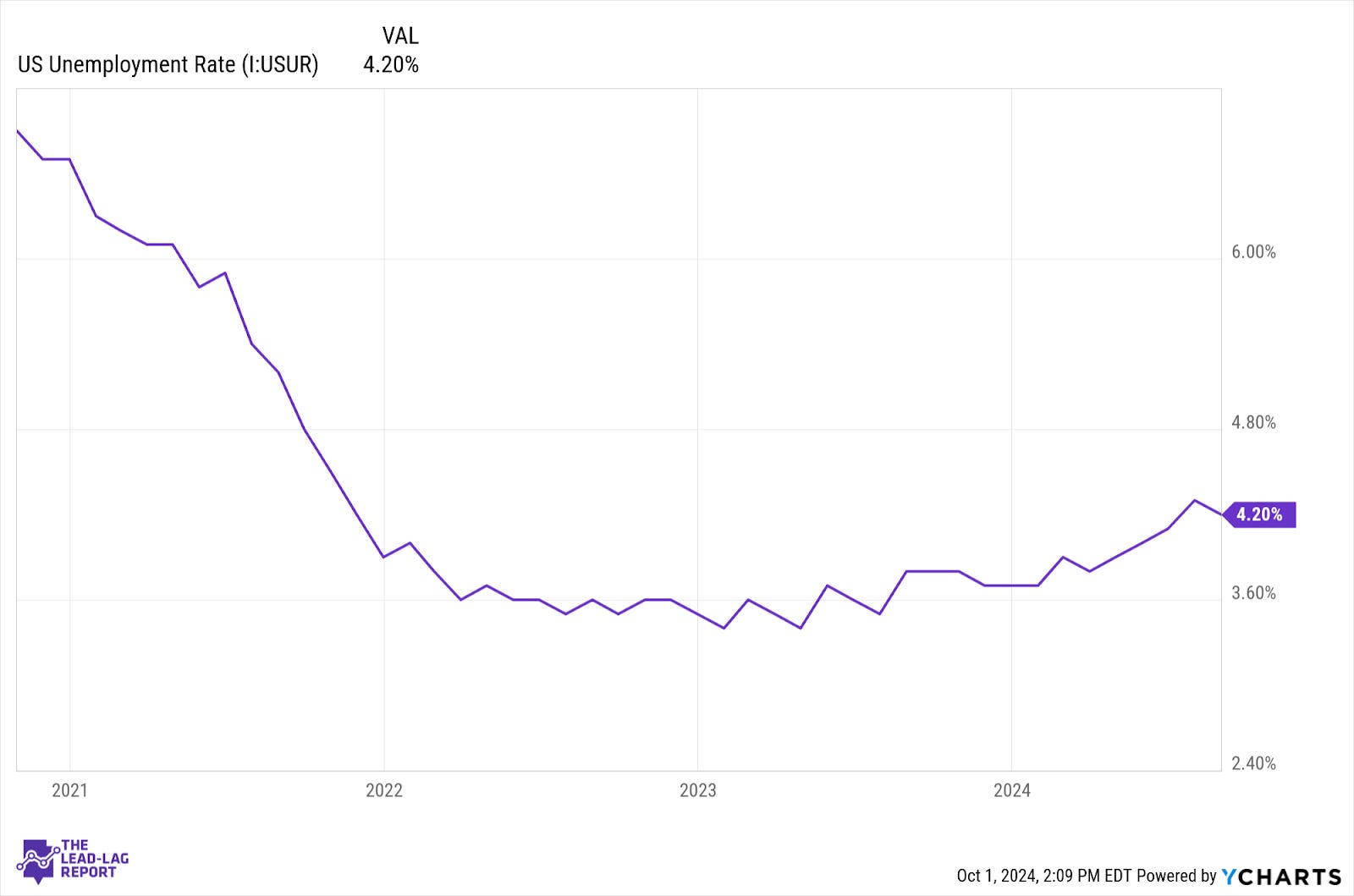

Second, the unemployment rate in the United States is still an historically low 4.2%.

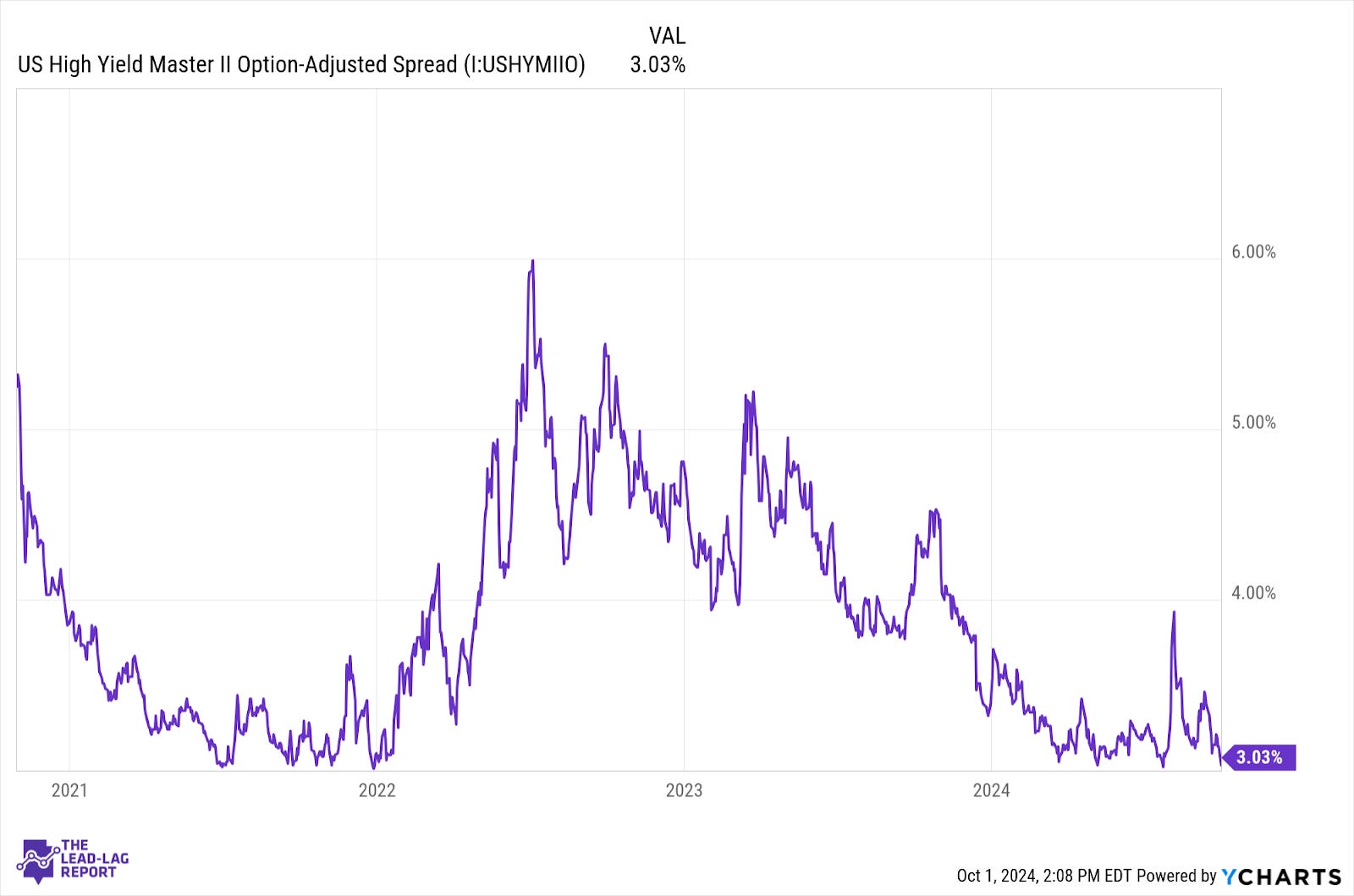

Third, as mentioned above, high yield credit spreads are hovering near all-time lows at just a hair above 300 basis points.

The argument is that a GDP growth rate of 3%, an unemployment rate of just above 4% and an inflation rate that’s back down to around 2.5% doesn’t really suggest that anything is wrong. In fact, it makes the U.S. economy look pretty good! If you ignore underlying credit conditions and focus only on the high level numbers, I’ll concede that it does paint a pretty nice picture.

But then I was struck by something I saw on Twitter/X.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.