A Fragile Place

Special Announcement

Where Sophisticated Investors Access Private Markets

For individual investors, sourcing and vetting high-quality, sub-scale private market opportunities poses challenges – information asymmetry, adverse selection, insufficient resources, etc.

Enter 10 East.

10 East, led by Michael Leffell, allows qualified individuals to invest alongside private market veterans in vetted deals across private credit, real estate, niche venture/private equity, and other one-off investments that aren’t typically available through traditional channels.

Benefits of 10 East membership include:

Flexibility – members have full discretion over whether to invest on an offering-by-offering basis.

Alignment – principals commit material personal capital to every offering.

Institutional resources – a dedicated investment team that sources, monitors, and diligences each offering.

10 East is where founders, executives, and portfolio managers from industry-leading firms diversify their personal portfolios.

Join with complimentary access at 10east.co

DISCLAIMER – PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided in the link is solely the creation of 10 East. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the link or make any representation as to its quality. All statements and expressions provided in the link are the sole opinion of 10 East and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the link.

Jerome Powell gave the markets the clarity they were looking for at Jackson Hole. By saying that “the time has come for policy to adjust”, he cemented the idea that a September rate cut is a done deal. The markets are anticipating that the Fed’s first move will be a more modest 25 basis point cut, but a half-cut reduction can’t be ruled out. Which way the central bank chooses to go could go a long way in understanding how much risk they feel the economy is at right now.

The most notable development is that Powell in his comments referenced the labor market more than inflation. Up to this point, the Fed has largely pointed to elevated inflation readings, particularly on the core side, as evidence that more work needed to be done, while stating that the labor market is in good shape. Last week, however, Powell indicated that the labor market might be the greater concern. We’ve already seen the unemployment rate rise by 0.9% from its low and the massive downward revision in jobs added over the past year raises questions about where the labor market is actually at right now. Powell sees “downside risks”, which would suggest the coming rate cutting cycle could be very prolonged. The Fed hasn’t had to deal with a sustained rise in unemployment since the financial crisis (the COVID recession saw a sharp spike, but a rapid decline once stimulus measures took effect) and it’s unlikely the central bank has a good grip on how to handle it.

If the slowdown in the labor market is here to stay, the current inflation problem is likely to take care of itself via a drawdown in demand. An aggressive rate cutting cycle could eventually trigger a second wave of inflation, but that’ll be an issue for the Fed to deal with down the road when & if it happens. Over the past half century, every sustained rise in the unemployment rate hasn’t stopped until the jobless rate hits at least 6% with several hundred thousand jobs lost in the process. We’re not to the point of negative monthly growth yet, but the constant downward revisions in the BLS data suggests we may not be far off.

As far as financial market reaction goes, U.S. stocks are behaving in much the same way that they did back in mid-July when a below expectations inflation report stirred up the rate cut frenzy. Small-caps are outperforming again since they would be most impacted by lower rates. Value is getting another look as is low volatility. We may be in the early stages of a rebound in utilities. There’s a lot still up in the air right now and we may need a few days for the dust to settle to see where we land. Investors tend to initially get bullish on the prospect of lower interest rates until they realize there’s usually a reason why rates need to be cut in the first place. While inflation initially got the blame, it looks like the labor market is the real culprit. As that trend continues, consumer and business activity contracts and then we head towards the credit event.

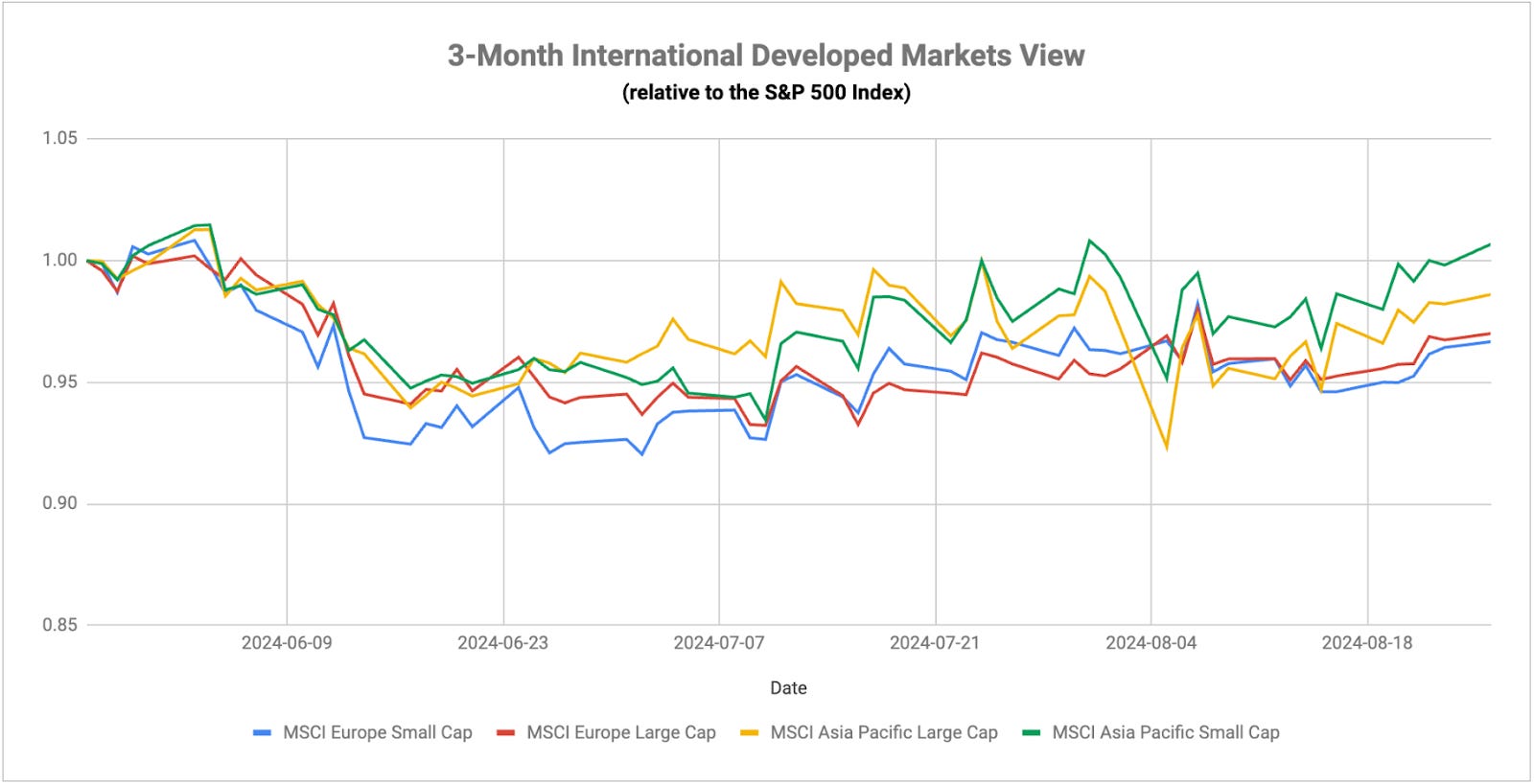

BoJ governor Ueda was called before the Japanese parliament to defend the central bank’s recent rate hike that destabilized the markets. If they were hoping for a dovish pivot, they didn’t get it. Ueda instead reaffirmed his intention to move rates higher again if inflation remains above the BoJ’s target (it’s currently steady at 2.8% annually and roughly 0.3% month-over-month). That gave new strength to the yen and pushed JGB yields higher, but stocks showed little reaction. This could ultimately trigger the next rally for the yen and potentially catapult stock prices higher in the longer-term. With the Fed poised to likely cut rates by 75-100 basis points by the end of the year and the BoJ probably hiking at least once more over that time frame, interest rate differentials could close substantially. Of course, that hawkish position could still be undone quickly if growth levels start to trail off in the next couple quarters.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.