A Good Fund Getting Dragged By A Shady Management Team

A Good Fund Getting Dragged By A Shady Management Team

What A Wild Story

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

I recently got an email from a subscriber asking about the Dividend & Income Fund (DNIF). It says…

“My interest is that the fund trades at a 35% discount to NAV and is yielding 9-10%. We know there are no free lunches and discounts can always widen and are volatile, but I have watched and invested in this fund for about 6 months and I cannot figure out the reason for such a material discount.”

I covered DNIF in this space more than two years ago, so it’s definitely time for a revisit. The title of the piece at the time included the phrase “what a wild story!”. The backstory for the fund still applies, but we have a better chance today of judging it purely as a fund instead of a “story”. I think some of the steps that the fund’s management team has employed to maintain control of the fund and who owns it still apply and have the potential of impacting its investment potential, but it’s time to see if that backstory creates an opportunity today.

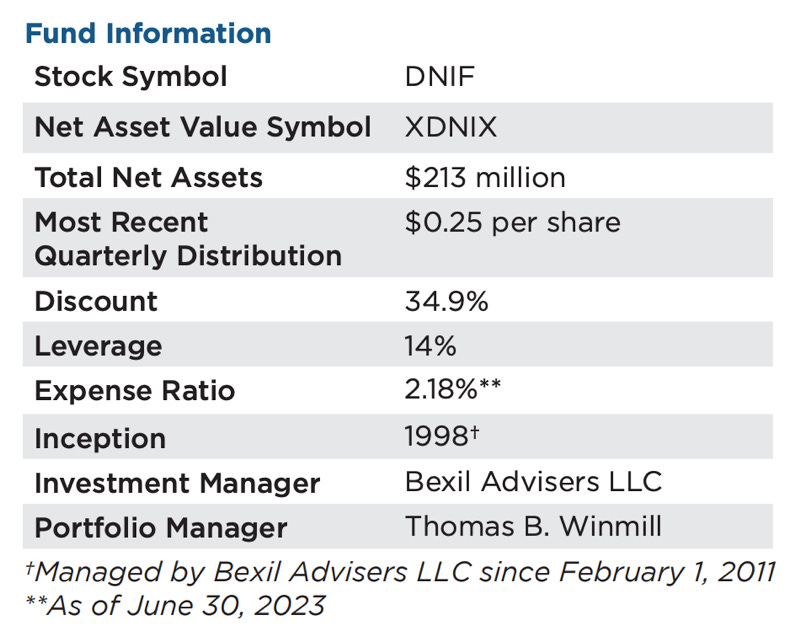

Fund Background

DNIF has a primary objective of seeking high current income with capital appreciation as a secondary objective. The fund seeks to achieve its objectives by investing, under normal circumstances, in income generating equity securities, including dividend paying common stocks, convertible securities, preferred stocks and fixed income securities, including bonds issued by domestic and foreign corporate and government issuers. In other words, it’s pretty unconstrained within the income-generating security universe. It also uses leverage in order to enhance yield and total return potential.

As a pure investment, DNIF is pretty straightforward and doesn’t offer many surprises. You can’t talk about the fund, however, without at least mentioning its history. The fund first debuted in its existing format in 2011 when Bexil Advisers took over. In its earlier years, it took a number of steps to exert control over the fund. Many of those steps weren’t necessarily beneficial to shareholders. It executed a number of rights offerings, which essentially increased the number of shares outstanding, and diluted the value of existing investments into the fund. This was a big part of the reason that the fund began trading at a larger and larger discount. At one point, activist investors started to get involved to try to take over the fund, so Bexil passed an amendment that forbade investments of 5% or more into the fund, essentially preventing these activist investors from obtaining a more influential position. They also decided to de-list the fund (it now trades on the pink sheets) in order to get around regulatory requirements. In all, it’s tough for me to feel comfortable investing in a fund where the management team has gone to great lengths to line their own pockets and put up walls to prevent anybody from breaking it up.

That being said, we can still look at the fund purely as an investment.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.