A High Yield Downside Risk Hedge That Doesn’t Provide Much Downside Protection

A High Yield Downside Risk Hedge That Doesn’t Provide Much Downside Protection

Look To The Left Of The Equal Sign

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

After another bad week for risk asset prices, it should be time for most investors to at least consider layering on some protection over their portfolios. Not just selling everything and moving into cash, mind you, but looking for ways to mitigate risk and hedge against drawdown potential. That could involve risk rotation strategies, long/short or just upping your allocation to Treasury bills. None of those strategies, however, really qualifies as high yield. To get there, you need an alternate strategy, but what can provide both a high yield yet hedge against downside risk?

The Global X S&P 500 Risk Managed Income ETF (XRMI) starts with a straight investment in the index and then layers on what’s known as a net credit collar strategy. This involves selling a covered call to generate the high yield, but using some of the proceeds to buy a protective put. The combination of the two options positions helps rein in overall portfolio volatility, but you really need to understand the structure of the fund to understand the risk/return profile. As is the case with Global X’s other covered call ETFs, the double digit yield is enticing, but would it do enough to hedge against the risk of a deeper market downturn?

Fund Background

XRMI seeks to track the performance, before fees and expenses, of the Cboe S&P 500 Risk Managed Income Index. The index measures the performance of a risk-managed income strategy that holds the underlying stocks of the S&P 500 and applies an options collar strategy on the S&P 500. It reflects the performance of the component securities of the S&P 500 combined with a long position in 5% out-of-the-money put options and a short position in at-the-money call options. The options collar seeks to generate a net-credit, meaning that the premium received from the sale of the call options will be greater than the premium paid when buying the put options.

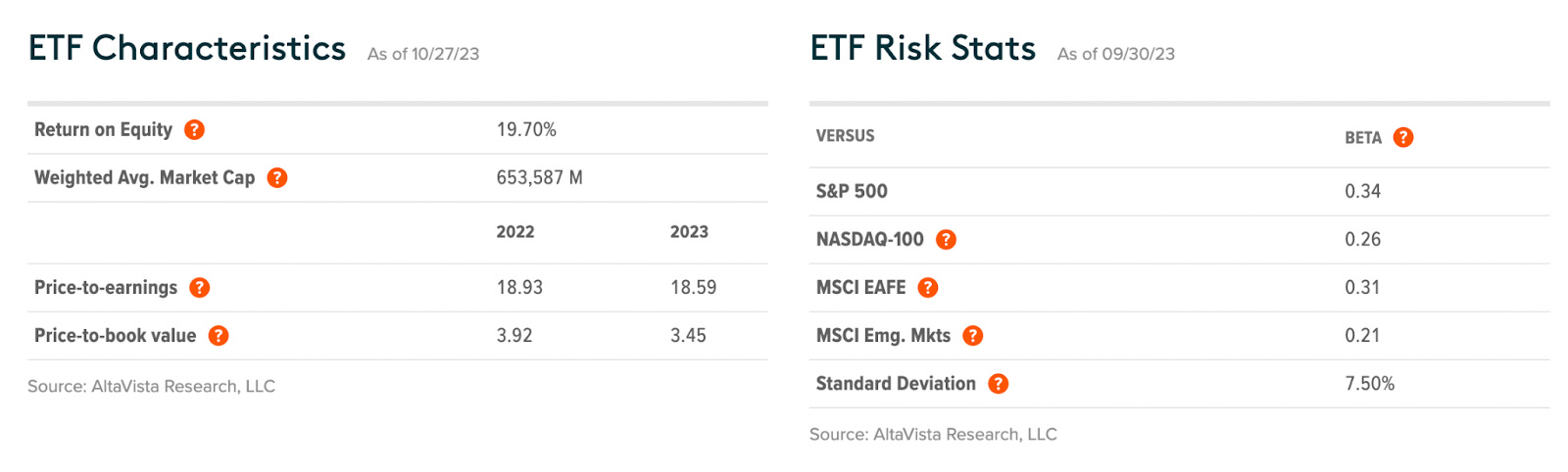

There’s no reason to discuss the S&P 500 itself since everybody knows what this is, but I will throw up some of the current risk metrics and valuation ratios for this ETF.

The valuation ratios aren’t as important as the risk stats here (although it’s worth noting that the P/E of 18-19, while lower than most of the post-COVID market period, is still well above the historical average). XRMI’s beta of 0.34 demonstrates that it’s not just less volatile than the underlying index, it’s significantly so. The covered call will cap most, if not all, of the underlying index’s upside, but the protective put also puts a floor on the index’s downside. That significantly modified range of possible returns essentially allows for the profile of a vanilla traditional covered call strategy with a downside cap at some point.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.