A Mix Of Good And Bad

A Mix Of Good And Bad

The First Target

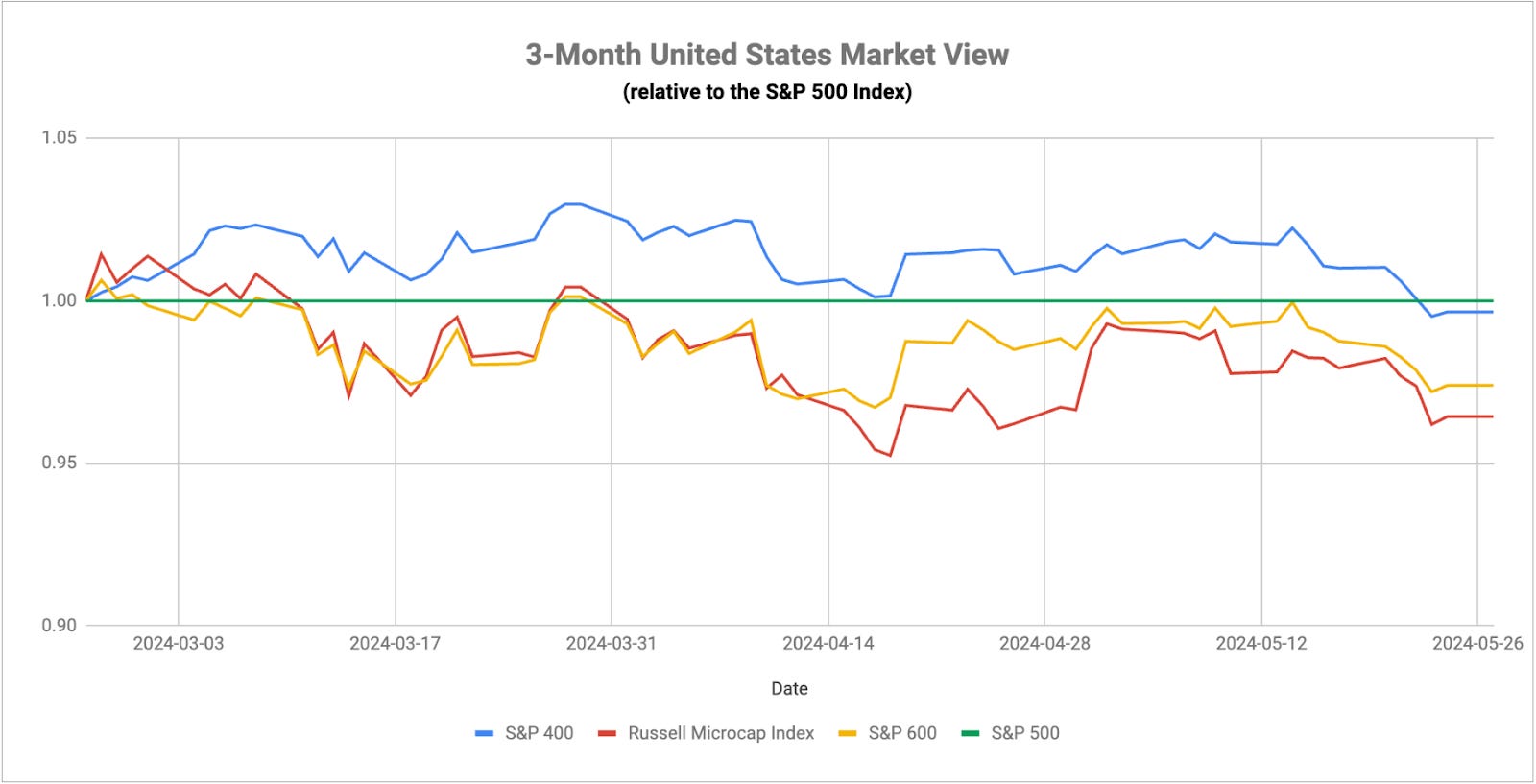

For much of the past few months, investors have been under the belief that 1) the economy is still in good shape and recession does not pose a threat and 2) the Fed will be imminently lowering interest rates in order to ensure the soft landing. That provided a strong backdrop for the cyclical rally that lasted from February through April. Now that inflation doesn’t look like it’s cooling any time soon and rate cuts are no longer imminent, that’s created a rotation back into tech & growth stocks and out of cyclicals. The rotation, however, has been incredibly narrow, being limited mostly to just mega-cap tech, in particular, NVIDIA. Over the past month, tech has gained more than 8%, but the equal-weight S&P 500 is up just 2% over that same time frame. In fact, the only two sectors to gain so much as 4% over the past month are tech and utilities. Translation: NVIDIA is hiding a lot of what’s going on outside of the magnificent 7 stocks and it isn’t good.

Needless to say, it’s an incredibly unusual market where the two best performing sectors are tech and utilities, but this is where we are. While gold takes a step back after a huge 20% rally, which is understandable, Treasuries have begun to step in and take their place. This is a group that has been closely correlated to changes in Fed expectations and, by extension, inflation, but we may be seeing some changes here. Sticky inflation and “higher for longer” generally translate into higher yields on the long end of the curve, but long bonds are up about 3% during the month of May so far. One thing we’re also seeing right now is the inversion of the Treasury yield curve getting worse, something which is usually consistent with recessionary expectations. Are we starting to see a bit of a flight to safety trade developing? It could still be in the early innings, but when utilities, Treasuries and gold are all outperforming at the same time, it’s usually for a reason.

Last week, the S&P U.S. Composite PMI reading surged to 54.4 in May, well above expectations and the highest print since April 2022. This was fueled by a big increase in services sector activity, the area of the economy that had been causing concern because of its recent downtrend. Clearly, this is good news for the economy at large, but bad news if you’re still waiting for rate cuts from the Fed. PPI inflation was already running hot and this report won’t do anything to dispel the idea that this is eventually going to translate over to the consumer side. There is a fair amount that would be supportive of higher interest rates at the margins, including consumer confidence and weaker than expected demand at recent Treasury auctions, but the fact that long bonds have been mostly holding up to this point suggests that safety seekers might be sniffing around.

Speaking of inflation risk, the Case Shiller Home Price index showed 7.4% year-over-year growth in March, the highest annualized gain since 2022. With housing accounting for a large chunk of the inflation basket, it looks more and more likely that we’re running out of catalysts that would push inflation back closer to the Fed’s 2% target any time soon. I still maintain that there’s a lack of price discovery playing a factor here because most homeowners are locked into 3% mortgages and aren’t moving any time soon, even if they wanted to. Contrast that with buyers, who are still getting priced out of the market due to soaring asking prices and expensive mortgage rates. All of this together suggests that the only way the economy might be able to get back to 2% inflation any time soon would be for something in the economy to break or enter a recession. Conventional means don’t seem to be working right now.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.