A Rough Start To Earnings Season

A Rough Start To Earnings Season

One-Off Or New Trend?

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: INVESTORS ARE FALLING BACK INTO OLD HABITS

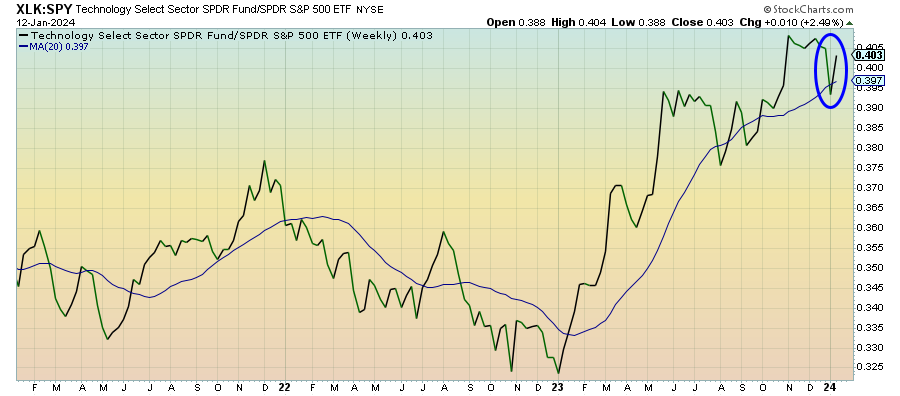

Technology (XLK) – One-Off Or New Trend?

The tech sector never seems too far away from initiating a sharp and sudden rebound. Last week’s inflation data seemed to be the catalyst and pushed this ratio back closer to all-time highs after it looked like it was buckling. Growth sectors typically see temporary spikes more often than other sectors and we really need to see the next few weeks play out before we can determine whether this was a one-off move or the beginning of a new trend.

Consumer Staples (XLP) – Interest Rates Are The Upside Catalyst

Staples took a step back last week amid the return to growth stocks, but I think the sector is still looking short-term positive. The inflation narrative from last week paved the wave for risk assets to lead again, but I think the issue of very disparate expectations for the future of interest rates remains one of the biggest risks for U.S. equities. If stocks need to correct as a result of rate forecasts updating, staples look like a good bet to lead.

Health Care (XLV) – Benefiting From Durability

Healthcare has thus far held on to early 2024 gains and remains in a strong position to be a longer-term market leader. Healthcare spending tends to be one of the most durable areas of the economy, but it hasn’t gotten a chance to shine in the global mega-cap tech rally. We’re seeing signs now that the magnificent 7 stocks may be losing their grip and that opens the door for a further breakout in this sector.

Communication Services (XLC) – Lost Its Momentum

This sector has generally been performing better than some of its growth counterparts and it’s likely due to some of the traditional media and telecom names in the space. Still, it correlates more closely with growth than other areas of the market and the fact that it’s been drifting sideways for the better part of the past three months suggests that the sector has lost its momentum despite big 2023 calendar year returns.

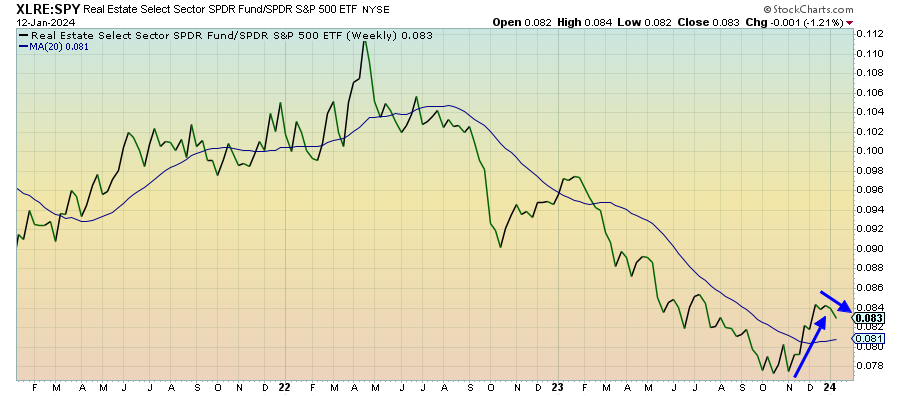

Real Estate (XLRE) – The Deteriorating Macro Narrative Takes Over Again

Real estate was able to make a nice run in Q4 when interest rates were crashing back to earth. Now that long-term rates have stabilized again, the overall macro storyline, which remains decidedly negative, is taking over again. This current situation isn’t necessarily too bad in the U.S. as falling rates take some pressure off of the housing market, but China keeps getting worse, as evidenced by the bankruptcy of one of the country’s biggest shadow banks.

Treasury Inflation Protected Securities (SPIP) – Acting Contrary To What The Stock Market Is Saying

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.