A Solid 10% Yielding Global High Yield Bond Fund

A Solid 10% Yielding Global High Yield Bond Fund

But Distribution Cut Risk Is High

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

Despite challenges with contracting liquidity, poor credit quality and global recessionary trends, junk bonds have still emerged as one of the best performing fixed income asset classes of 2023. It hasn’t just been limited to U.S. high yielders either. Foreign bonds, including emerging markets debt, have also performed quite well. A couple of years ago, investors were considered to be taking an inordinate amount of risk reaching for 4% yields right before inflation really took off. Today, the market has digested most of the central bank tightening cycle and 8% junk bond yields don’t seem quite as scary any more.

That doesn’t mean they aren’t without risk. In fact, the risk of owning high yield bonds today may be higher than at any point of the last decade. The PGIM Global High Yield Fund (GHY) attempts to manage some of those risks, while still allowing investors to still capture those high yields. Historical performance has been relatively good, but investors are taking a fair amount of risk in order to achieve those returns. In this environment, it might end up being a little too much.

Fund Background

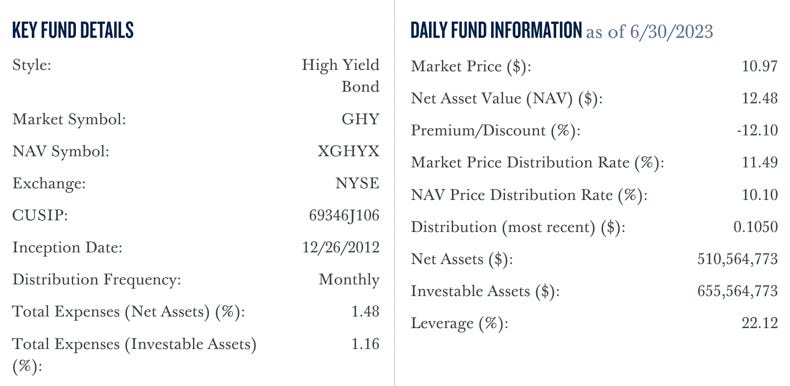

GHY seeks to provide a high level of current income by investing primarily in below investment-grade fixed income instruments of issuers located around the world, including emerging markets. The fund, however, may invest in instruments of any duration or maturity. It also uses leverage in order to enhance yield and total return potential.

GHY’s 22% leverage overlay isn’t excessive, but it may become costly. The graphic above shows a total expense ratio on investable assets of 1.16%, but as of the end of Q1, the fund’s fact sheet quoted a ratio of 1.66% with the ratio on net assets approaching 2%. That’s definitely on the higher end and with interest rates much higher than they were even a year ago, the cost of continuing to implement leverage is going to be higher. That doesn’t make it an impossible hurdle to clear, but it does make it more challenging. In terms of strategy, the fund’s objective and investing style are pretty straightforward.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.