A Solid “All Quality” Corporate Bond Fund With A 7% Yield, But It Isn’t Built For Safety

A Solid “All Quality” Corporate Bond Fund With A 7% Yield, But It Isn’t Built For Safety

Looking for high yield options in this market often leads investors towards lower quality securities, including junk bonds.

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

When Janet Yellen said this week that the government’s “extraordinary measures” could run out as soon as June 1st, the markets were put on notice. We walked this same path back in 2011 and it didn’t end up well for the risk asset markets. About a week before the debt ceiling deadline, equities fell by more than 15%. Junk bonds dropped nearly 10%. But investment-grade corporate bonds held up pretty well. While Treasuries were the asset class of choice in this volatile environment, higher quality corporate bonds served as a more than adequate replacement for safety.

Looking for high yield options in this market often leads investors towards lower quality securities, including junk bonds. Given how questionable conditions look at the moment, it might be a good idea for investors to more strongly consider investment-grade fixed income. The Western Asset Premier Bond Fund (WEA) doesn’t invest entirely in high quality bonds, but it has most of its assets there. There are few CEFs out there that offer high yields, yet completely stay away from junk bonds. This fund could be a happy medium by delivering a high yield, quality-tilted portfolio and an historically good track record.

Fund Background

WEA’s investment objective is to seek current income and capital appreciation by investing primarily in a diversified portfolio of investment-grade bonds. The fund must invest at least 80% of assets in a combination of government, corporate, agency & mortgage-backed securities and at least 65% of assets in bonds that are rated investment-grade at the time of purchase. The fund expects that the average effective duration of the portfolio will range from 3.5 to 7 years. The fund also uses leverage to enhance yield and total return potential.

You can see clearly from the fund’s objective statement (and later when we look at the fund’s composition) that this is NOT an investment-grade bond fund, it’s a mostly investment-grade bond fund. Still, that’s going to be much better than most fixed income CEFs that dive mostly, if not entirely, into junk debt, sometimes deeply into junk debt. The comparatively better risk profile should help mitigate some downside risk, especially when spreads start blowing out. There’s a distinct possibility that leverage could offset some of that, but the overall tilt towards higher quality bonds should be more fitting for the current environment.

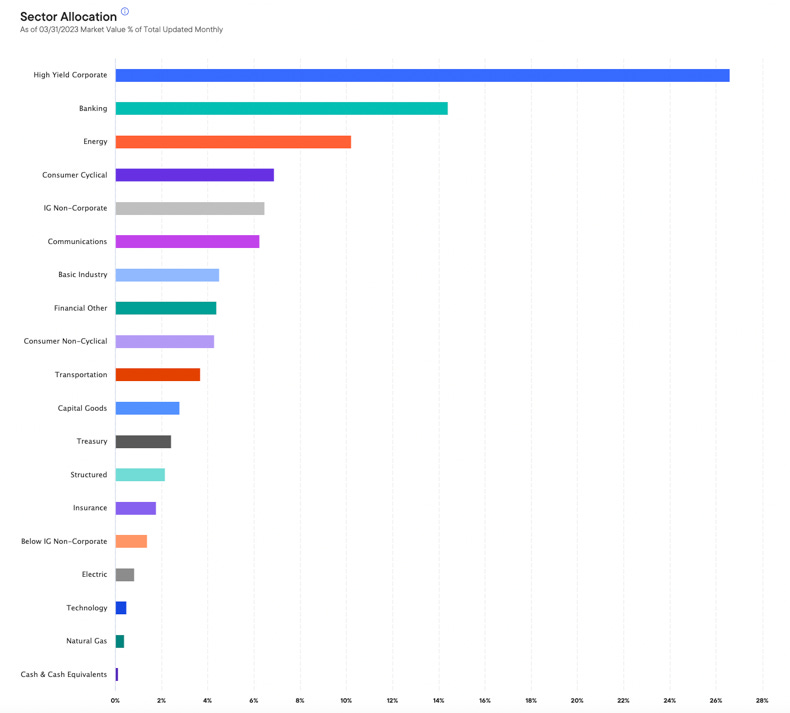

On the surface, WEA looks pretty well diversified, but the lean towards economically-sensitive areas of the market is cause for caution.

We’ve got the 26% allocation to junk bonds right off the top, but the next ~30% of assets go to a combination of financials, energy and consumer cyclical issuers. That’s not necessarily defensive by any means and could pose trouble if the economy continues to slip-slide towards recession later this year. On the flip side, WEA looks like it could also be well-positioned to outperform coming out of any downturn since cyclicals and higher risk securities tend to lead on the way back up. Short-term questionable, but longer-term potential.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.