A Solid Long-Term Growth Play

A Solid Long-Term Growth Play

Even If It Doesn’t Work For Income Seekers

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

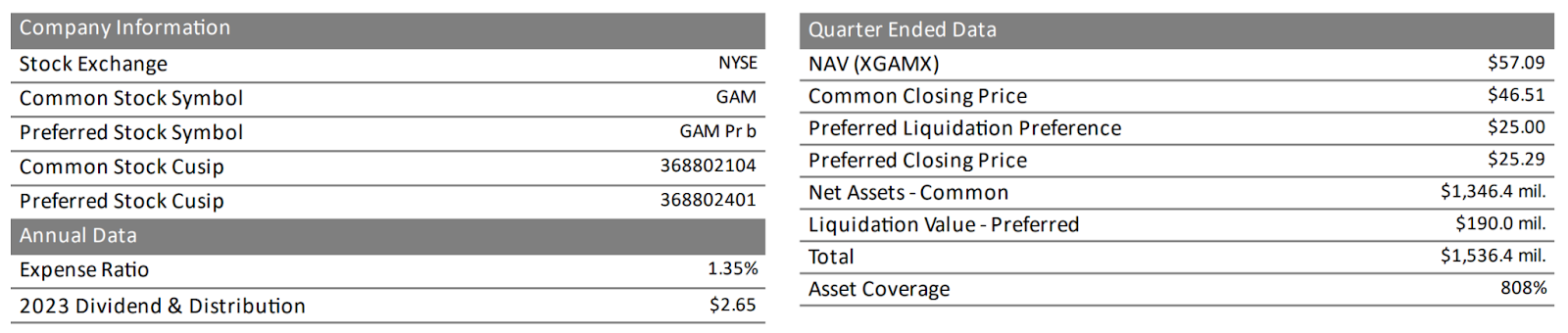

It’s not often that you can find a fund with a track record of nearly 100 years, but that’s the case with the General American Investors Fund (GAM). Originally launched in 1927, it has experienced the Great Depression, the COVID pandemic and everything in between! GAM is a little different from many other closed-end funds in that it focuses more on long-term growth than current income. That can make it a little less than ideal for individuals relying on their portfolios for steady and predictable income.

The fund’s ultra long-term track record, however, is undeniable and the strategy of targeting higher growth companies might be particularly appealing to those looking to ride the current tech/AI rally. Returns have been a little more mixed in the near-term and the use of leverage in addition to the core strategy could add a little too much risk for some. It’s somewhat unique within the CEF space though and worth taking a deeper dive on.

Fund Background

GAM’s objective is long-term capital appreciation through investment in companies with above average growth potential. The fund approaches portfolio diversification by selecting companies individually without reference to industry weightings in the S&P index. The managers believe that adequate diversification can be achieved with a limited number of holdings (50 to 70) in diverse industries. Individual security weightings depend upon the assessment of the company’s potential for growth as well as the market liquidity of the security.

Overall, the fund tilts towards growth, but not by much. With a focus on large- and mega-cap names, it doesn’t look like it will behave substantially differently than many other large-cap funds that are out there. The 12% use of leverage is very reasonable and allows for an improvement of risk-adjusted returns without overdoing it on risk, something that’s especially important considering the high cost of implementing leverage nowadays. The fund’s website boasts an 18% average annual turnover rate, which could be considered relatively low for what you might expect from an active strategy.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.