A Surprisingly Steady 8% Yield

A Surprisingly Steady 8% Yield

It Could Be Ready To Hit Its Groove

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

The markets have shifted over the past month, first because of the 50 basis point cut from the Fed and then because of the China stimulus package. With monetary and fiscal policies easing, there’s a fresh opportunity for risk assets to keep pushing higher, even the ones that look overvalued as it is. In particular, interest rate sensitive sectors have performed well as have cyclical ones with heavier exposure to the commodities space. No longer is this a market where the magnificent 7 stocks control the major indices. The markets have broadened out, which means new opportunities in the high yield space.

One such fund is the InfraCap Equity Income ETF (ICAP). On the surface, it may sound kind of like a traditional dividend equity fund. Underneath, there’s options strategies, liquid alts and a few other odds and ends that make this fund anything but traditional. But it has delivered consistently on one front - high yield. With the markets changing and cyclicals getting new life, this could be a strategy that has some high potential.

Fund Background

ICAP is an actively-managed fund that seeks to achieve high yield by investing at least 80% of its net assets in a diversified portfolio of equity securities of companies that pay dividends. Through active management, security selection and weightings are based on rigorous, fundamental analysis and global macroeconomic factors. The fund also utilizes a covered call strategy in order to enhance income, which generally lands at around a 50% overlay.

As mentioned up top, ICAP is much more than just a dividend equity fund. In many ways, it looks like a lot of unleveraged closed-end funds, just without the premium/discount to NAV. That includes the expense ratio, which is egregiously high by ETF standards, even before you consider the costs of overlaying the options strategy. It also includes the variety of security types held in the fund, which includes cash and preferreds, but it’s all designed in the pursuit of high yield. The covered call strategy caps some upside and lowers risk by a modest amount, but this is still going to be on the high end of the risk spectrum.

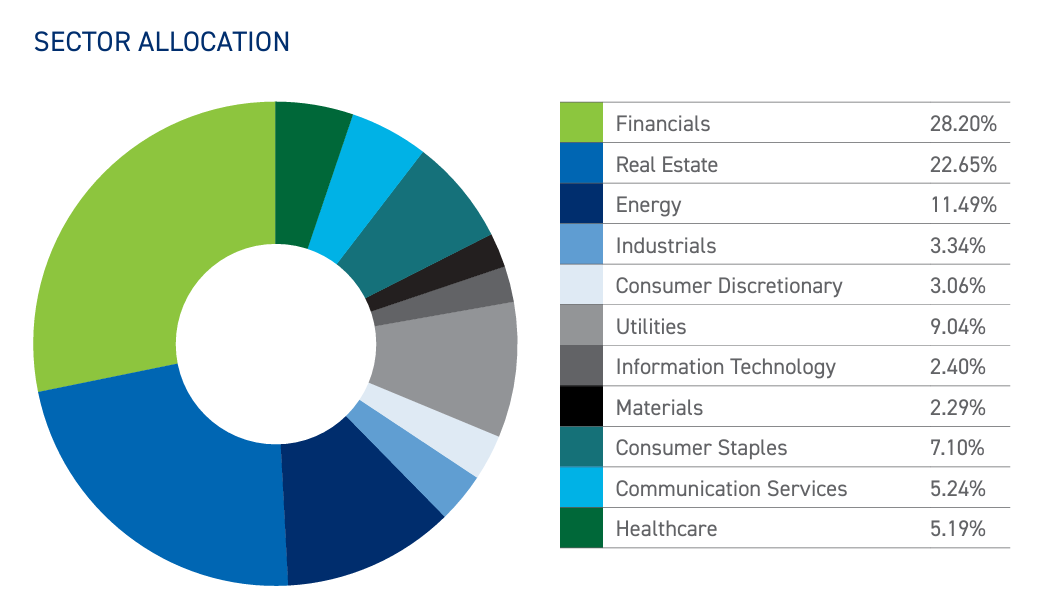

We can see right off the top that this is going to be a very rate-sensitive portfolio. Financials and real estate, two sectors perhaps most impacted by changes in rates, account for half the portfolio by themselves. The next 20% of assets are dedicated to the combination of energy and utilities, two more sectors influenced by rates. Within that energy sector allocation is also some exposure to MLPs. It’s not a lot, so it doesn’t really have a meaningful impact on yield or volatility. Overall, the portfolio is roughly 80% equities and 20% preferreds, giving it a mix of income sources.

At the top of the portfolio, you get several of the traditional equity names, but you can see some of the diversity as you work your way down. MPLX is an MLP. Equinix is a data center. BXP is a REIT. SLM issues school loans. There’s really a wide variety of exposures here that go far beyond what you’d expect to see in more traditional dividend income strategies.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.