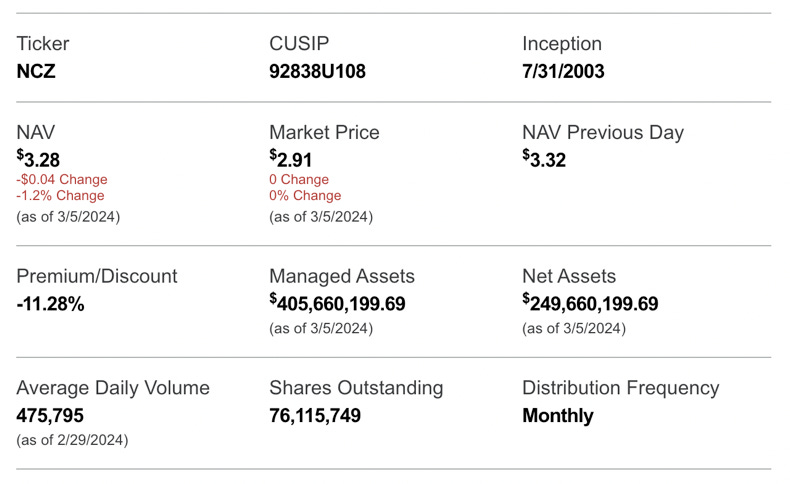

An Attention-Grabbing High Yield

An Attention-Grabbing High Yield

Without The Numbers To Support It

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

A subscriber recently sent me the following message…

“I was reading through some of the content last evening and I was interested in how you view ticker NCZ. Been around for a while and definitely has some big leverage attached. Kind of more of a rate play to me with all the leverage, but most of these funds are. Pays monthly and annual DVD yield 13.5% to 14% at these prices. Convertible aspect is a decent amount of the holdings. Just figured I would run it by you, and get some thoughts from your perspective.”

The fund this person is referring to is the Virtus Convertible & Income Fund II (NCZ). The general description is correct, but there’s a lot to consider with this fund - risk, composition, performance, leverage. Whether to add this fund to your portfolio goes beyond just deciding that you want to invest in this asset class. This group has had a solid run over the past year, riding the coattails of the magnificent 7 fueled rally in equities, but NCZ’s aggressive strategy could tilt the risk/reward profile in the wrong direction.

Fund Background

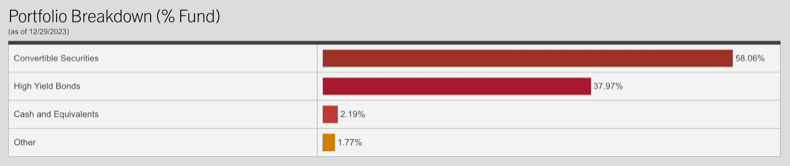

NCZ seeks total return through a combination of capital appreciation and high current income. It invests in a diversified portfolio of domestic convertible securities and high-yield bonds rated below investment grade. Under normal circumstances, it will invest at least 50% of its total assets in convertible securities, but determines its allocation based on changes in equity prices, changes in interest rates, and other economic and market factors. For the convertible portion, Voya Investment Management seeks to capture the upside potential of equities with potentially less volatility than a pure stock investment. In searching for investment opportunities, the manager looks for issuers that will successfully adapt to change, exceed minimum credit statistics, and exhibit the most promising operating performance potential.

NCZ also utilizes leverage in order to enhance yield and total return potential.

NCZ is a relatively nice mix of exposures if you’re looking to try to capture a really high yield while maintaining some equity upside. Convertibles have been a nice option over the past year during the stock market rally, although I’m not sure how much that can be counted on going forward as a return boost. The high use of leverage is an immediate red flag for me. Leverage often doesn’t enhance risk-adjusted returns under normal circumstances. Layering on so much leverage at a time when the cost of doing so has gotten really high is a recipe for underperformance.

NCZ is very roughly a ⅔-⅓ mix of convertibles and junk bonds. The convertible allocation is impactful if you’re looking for a steady fixed income instrument. In general, convertibles are about 50% more volatile than junk bonds due to their equity-like characteristics. That makes their inclusion as part of a fixed income instrument less than an ideal fit from a risk perspective. As part of a pure high yield play, it can make sense to include them as part of a total return objective, but it does add risk.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.