An Imminent Breakdown

An Imminent Breakdown

But Just How Imminent?

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: EVEN SOME OF THIS MARKET’S WINNERS ARE JUST A CASE OF WINDOW DRESSING

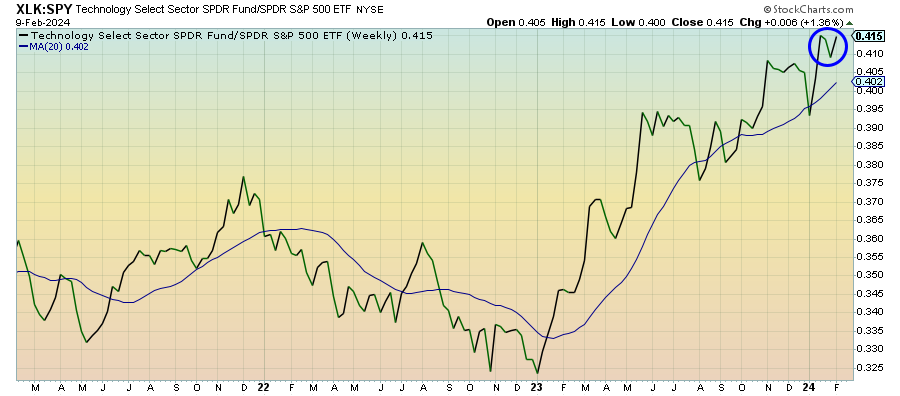

Technology (XLK) – Not A Healthy Market Advance

Every brief period of underperformance seems to quickly reverse and establish a new high. While the current environment has been great if you’re overweight tech stocks, it’s been a very bad sign for overall market health. This sector and communication services are the only ones beating the S&P 500 year-to-date, a trend that isn’t a hallmark of broad, healthy and sustainable market advances.

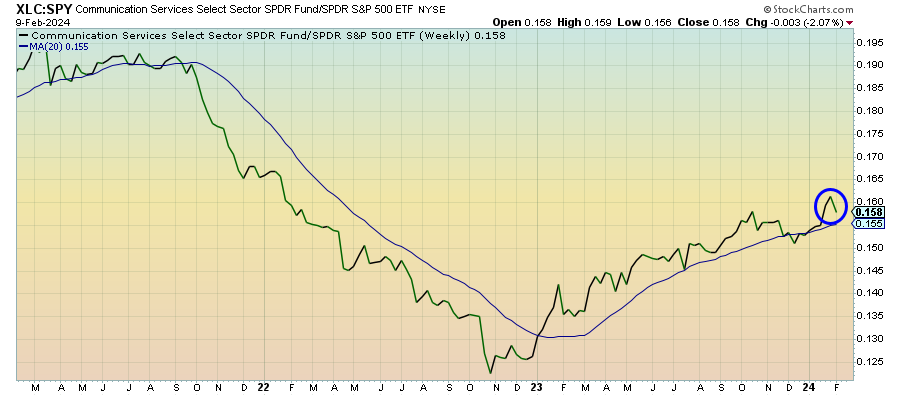

Communication Services (XLC) – A Case Of Window Dressing

Despite solid performance year-to-date, even this is just a case of window dressing. The fact that this sector is beating the S&P 500 this year is almost entirely a function of Facebook’s 30%+ YTD gain. The equal weight version of this sector is actually trailing the index by 7%. Even as one of just two sectors beating the S&P 500 this year, it’s actually performing a lot worse than it seems.

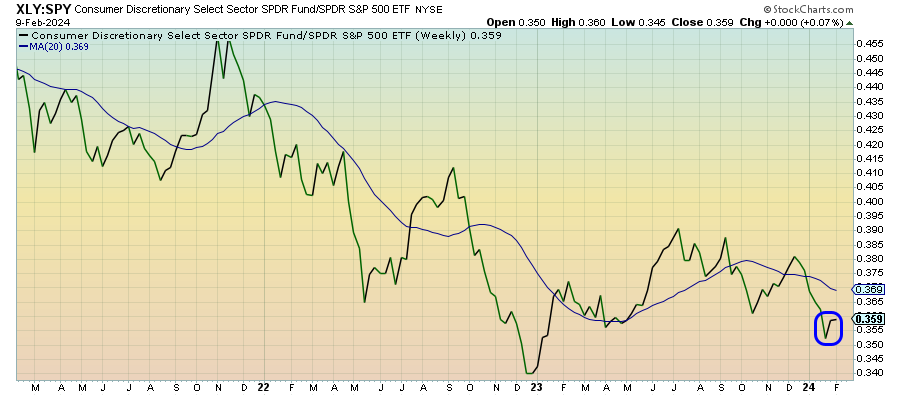

Consumer Discretionary (XLY) – Investors Are Still Fading Despite The Data

Discretionary stocks are picking up a bit of momentum here, but it should be concerning that investors are fading this sector even though spending and sales figures have remained strong throughout this cycle. The big retailers have already noted concerns with the ability of consumers to keep spending and debt delinquencies are on the rise across almost every category.

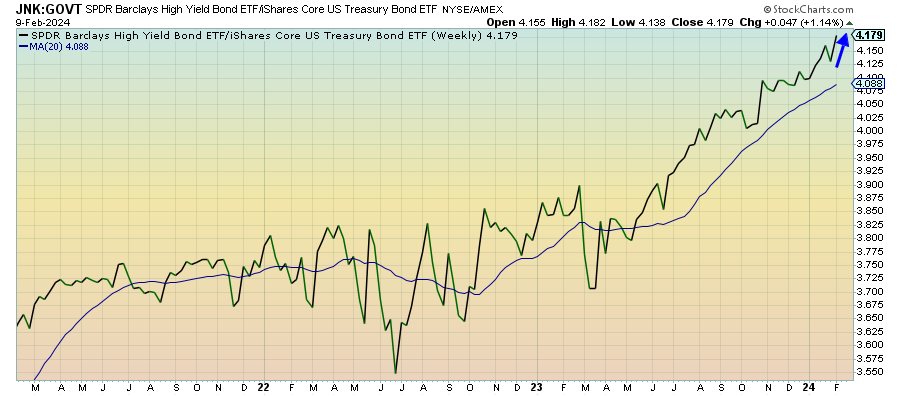

Junk Debt (JNK) – Upside Potential Just About Capped Out

As long as investors remain focused on the high level economic growth narrative and ignore the evidence of building consumer weakness, there will probably be a floor under junk bond prices. It just doesn't seem, however, that there’s much more room to go higher. The market is pricing in a nearly best case scenario for these bonds and historically low credit spreads offer little upside in terms of spread contraction. The risk/reward tradeoff keeps looking worse.

Emerging Markets Debt (EMB) – Solid Growth Backdrop Without The Overvaluation

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.