Are Spreads Finally Starting To Blow Out?

Are Spreads Finally Starting To Blow Out?

This Rally IS Different

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: THE FLIGHT TO SAFETY TRADE CONTINUES TO BUILD AND EXPAND

Health Care (XLV) – Not Providing Confirmation Yet

Outside of utilities, defensive equities remain quietly under the radar. Underperformance is pretty consistent across most subsectors, but it’s been hit particularly hard by weakness in biotech. With this sector largely moving sideways and consumer staples still lagging pretty significantly, I think we need to see more confirmation outside of just utilities to feel better saying that we’ve entered a broader risk-off regime.

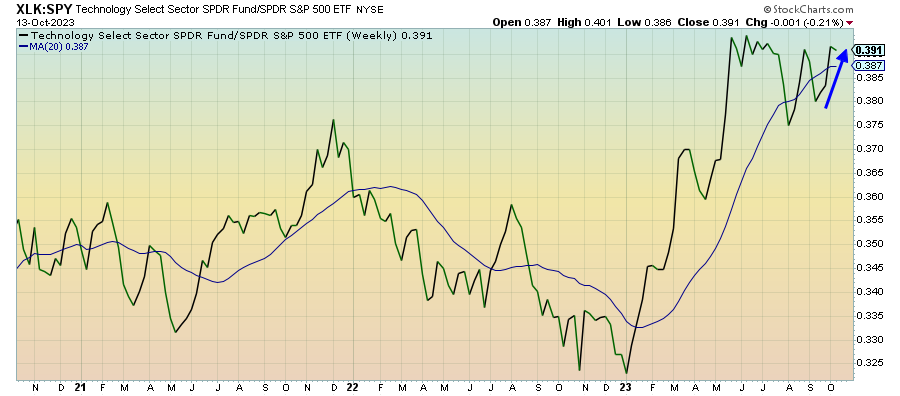

Technology (XLK) – Signs Of Instability & Weakness

While tech stocks at least took a one-week break from whipsawing relative to the broader market, most of October’s relative outperformance is, again, being driven by large- and mega-cap stocks. The equal weight version of the tech sector has only returned about half of the cap-weighted index year-to-date, so this sector isn’t nearly as strong as it appeared. Continued volatility within this group would not be a good sign for market stability going forward.

Communication Services (XLC) – Earnings Loom

This sector has overtaken tech as the best performer of 2023 with a return of more than 40%. Its consistency of outperformance is perhaps the more impressive factor. Next week will be the big one for this sector as Meta and Alphabet, which account for nearly half of its overall weighting, will deliver their quarterly earnings results. As always, expect some heightened volatility around the first half of the week.

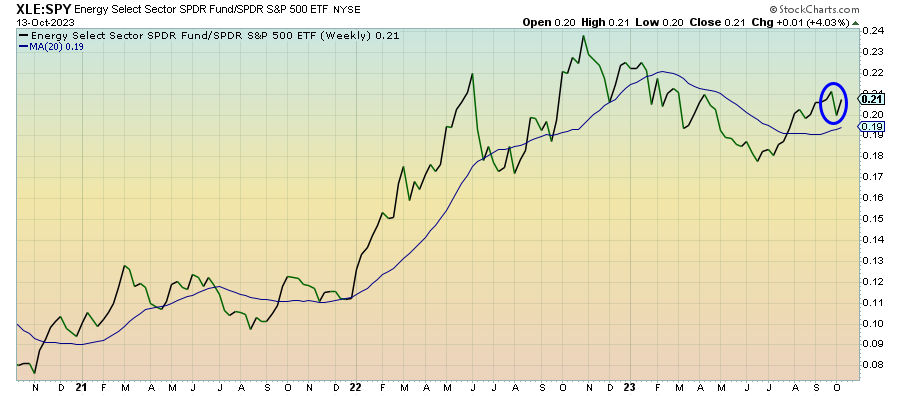

Energy (XLE) – The Geopolitical Backdrop

Global geopolitical risks usually serve to spike energy prices and the conflict in Israel is no exception. Crude oil prices are up more than 6% from their low earlier this month on anticipated supply chain disruptions and those concerns don’t look like they’ll be letting up soon. While that’s negative from a human impact, it does help energy stocks move higher. The longer-term concern of lower energy demand takes a back seat for now.

Junk Debt (JNK) – Are Spreads Finally Starting To Blow Out?

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.