Aren’t Rate Cuts Supposed To Happen When Conditions Are Deteriorating?

Aren’t Rate Cuts Supposed To Happen When Conditions Are Deteriorating?

Few.

I talk a lot about housing correction, credit contractions and other macro events as catalysts for a pullback in the markets, but I think the biggest short-term reasoning for a pullback here is simply investor euphoria. After getting the data they wanted on the inflation front and the long-anticipated Fed pivot, investors seem to have shifted from hoping for a soft landing to believing that there will be no landing at all. If the unemployment rate is below 4%, GDP growth is still running at 3% annually and now the latest housing starts number indicates that homebuilders are getting more optimistic, should investors really be worried about recession at this point? Clearly, they don’t think so, but by almost any measure, they’ve gone way overboard in the short-term.

The question I have is if everything is so awesome right now, why did the Fed just pivot and forecast three rate cuts in 2024? Aren’t rate cuts supposed to happen when conditions are deteriorating? If we’re in this goldilocks economic environment, shouldn’t this at least be the argument for keeping rates where they’re at, if not raising them again? After all, the core inflation is still at 4% right now. By historical standards, cutting rates when inflation is at 4% would be considered absurd. Plus, the latest economic projections released by the Fed at the latest meeting showed that they’re calling for a 4% unemployment rate through 2026! It would seem that the Fed isn’t expecting a recession at all if they think the jobless rate is going to hold at 4%. So again, why are they talking about cutting rates three times in 2024 if they don’t see a recession? Either the Fed is just following the market & Treasury yields here or they believe something that they’re not telling us.

Investors, however, have gotten even more disconnected from reality. They’re acting as if there’s going to be no recession at all, yet they’re also expecting the Fed to cut rates 6 times over the next 12 months? This sounds more like a recipe for another round of inflation than anything if we’re already starting at 4%. Powell said more than once that he’d rather overtighten and risk a recession than undertighten and risk higher inflation. Last week’s messaging would seem to be a 180 reversal from that stance. Perhaps the economy can manage to avoid a recession altogether and it can bring inflation back down to a sustainable 2% target by launching an extended rate cutting cycle here. It seems more likely to me that they’re going to break something by drifting off course again.

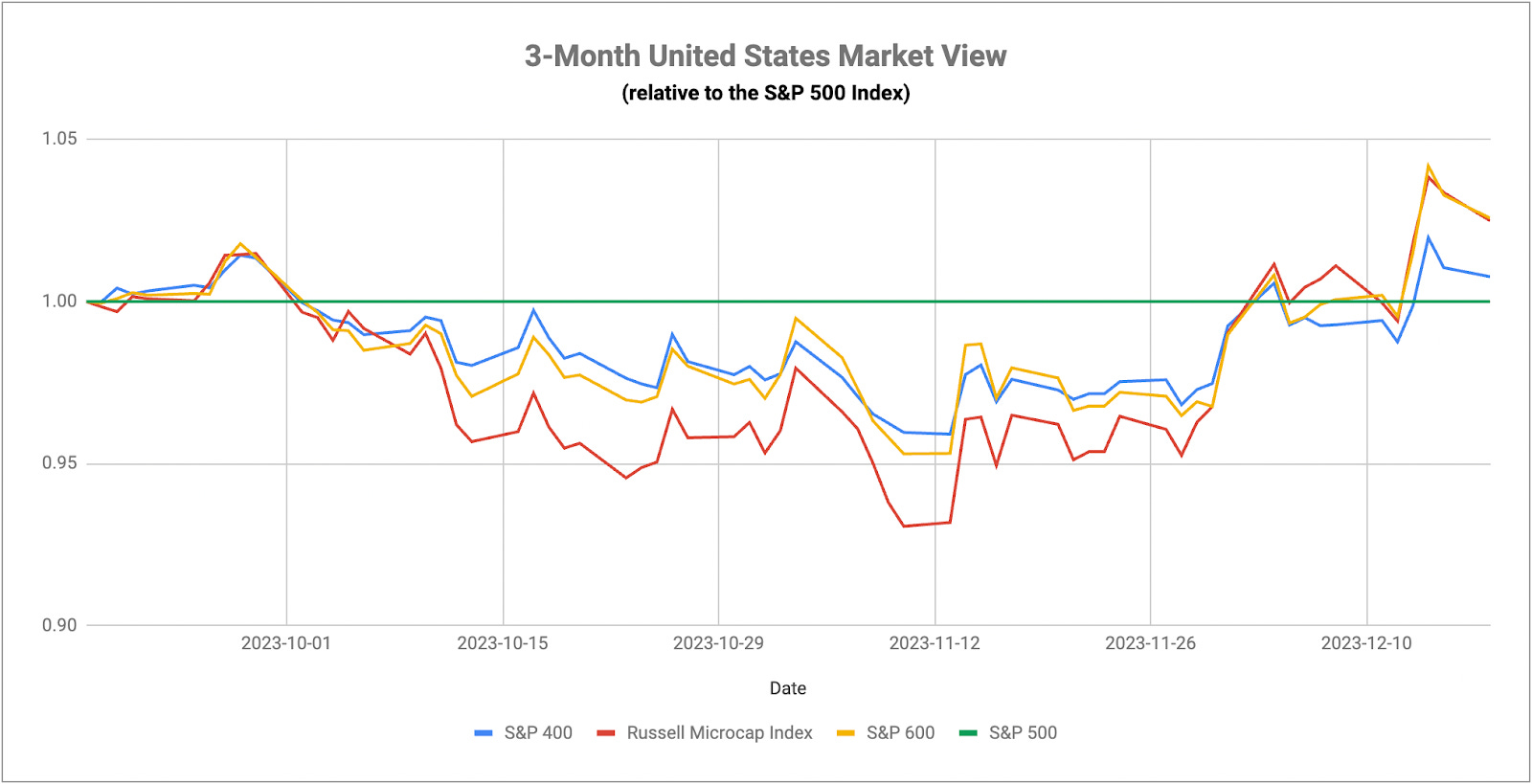

Small-cap leadership, like the kind we’ve seen over the past several weeks, is a sign that market breadth is expanding and moving past the leadership of just a handful of mega-cap stocks. It’s encouraging because it could be signaling an extension of the current rally, but we’re not quite there yet. The Russell 2000 has just broken above the nearly identical peaks it hit in August 2022, January 2023 and July 2023. If small-caps can break through this ceiling and keep moving higher, the case that this is a genuine bull market rally gets stronger. If it hits this mark for the 4th in the past 18 months and gets turned back yet again, then I think we’re looking at an equity market that’s still showing some underlying sign of weakness. It’s important to remember that the S&P 500 is still about 10% below its inflation-adjusted highs. While the current rally in both stocks & bonds has been unquestionably strong, I think at least a modest pullback from deeply overbought levels would be a healthy thing at this point.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.