Beware Seasonality

The “NVIDIA effect” is starting to have the impact on the financial markets that I feared it might, although it took longer than expected. The company didn’t really deliver any bad news per se during last week’s earnings call, but when expectations are already sky high, even meeting forecasts can feel like a letdown. As growth rates inevitably begin to moderate and valuations start to constrict, several of the big name mega-caps are going to struggle to keep up the momentum amid changing conditions. NVIDIA is now down about 17% from where it was just a week ago and sits more than 20% below its all-time high. As a result, most market sectors look comparatively better and performance is definitely spreading out beyond just a handful of tech names.

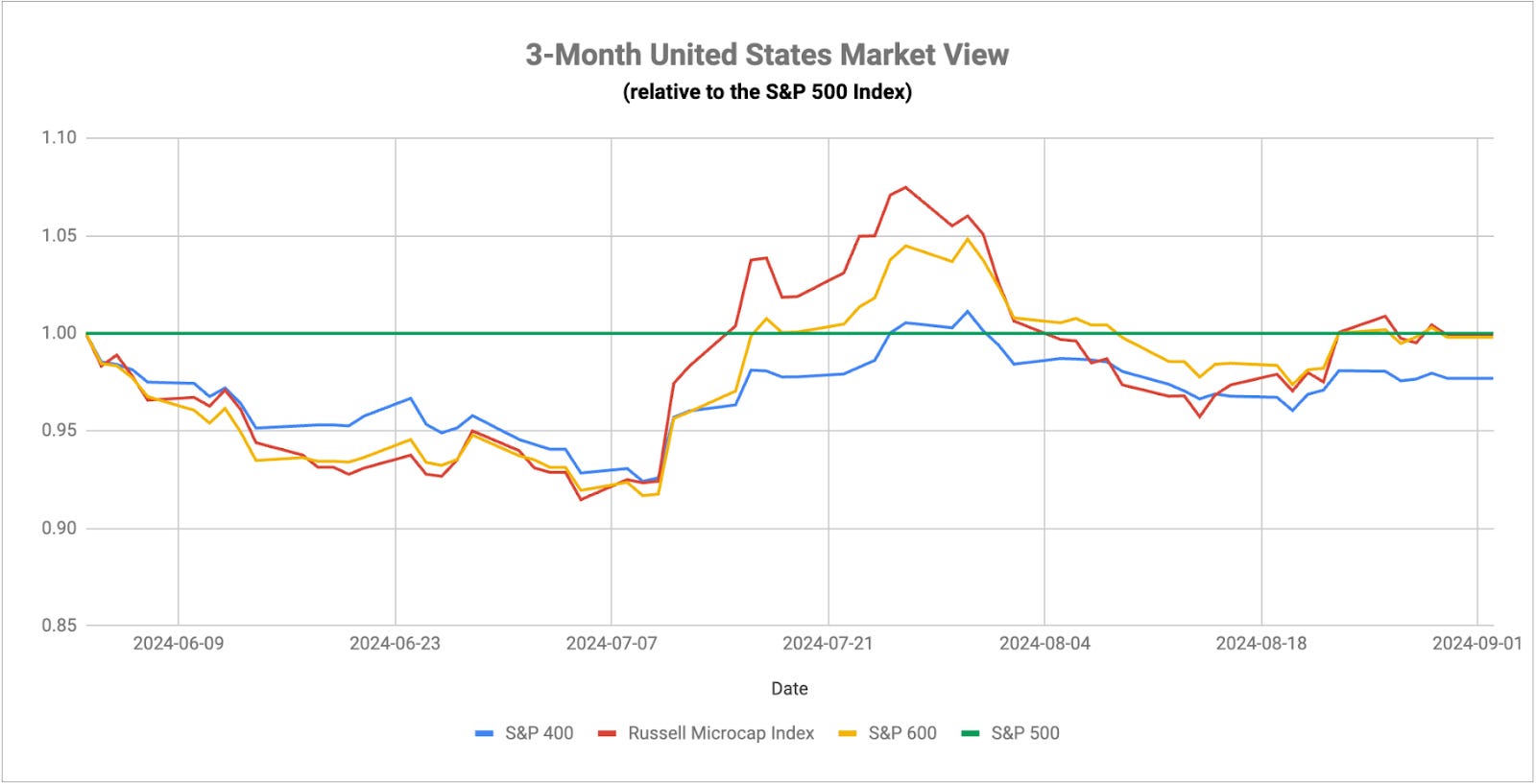

As some of the tech momentum begins to cool, the big beneficiary hasn’t yet been small-caps in the way it was back in July. Instead, it’s been defensives and cyclicals within the large-cap arena. The fact that they’re all outperforming in unison (energy being the one notable exception) suggests that there is a fairly strong rotation away from past winners and towards economically-sensitive sectors (should GDP growth remain steady) or defensive sectors (should the economy slow or even contract). The one thing that risk rotation strategies need is broad participation from the equity markets and risk-off behavior from Treasuries. Over the past few weeks, we’re starting to see evidence of that on both ends. Broad market participation creates a better opportunity set for outperformance from the risk-on position (should small-caps or emerging markets, for example, lead instead of just mega-caps). If Treasuries show strength in the face of more volatile conditions, which they did a month ago and have the Fed rate cut tailwind at their back, this could turn into a very favorable period.

The biggest stumbling block this week will be Friday’s jobs report. Depending on how much faith you want to put into that given the massive downward revisions we’ve seen recently, all eyes will be on the unemployment rate, which has moved from 3.7% in January to 4.3% in July. With the Fed turning its focus to the labor market instead of inflation, this could be an incredibly consequential report that drives Fed policy decisions into 2025. If we get a number that meets expectations, we’re likely headed for a quarter-point cut in September as the launching point for a slow & steady easing cycle. If we see more weakness, a half-point cut could be on the table, which would raise fears that 1) recession risk is growing and 2) the Fed is falling behind the curve again in its ability to deal with it.

Another thing that could begin impacting the markets is seasonality and the upcoming election. This is one of the traditionally weaker periods for equities and I think we’re already starting to see sentiment deteriorating. There’s a very large discrepancy between the two potential economic paths depending on who wins in November. The markets seem to be taking the threat of huge tariffs at least somewhat seriously and that could put a cap on significant upside until the cloud of uncertainty is lifted.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.