BoJ's Loose Policy Nightmare: The Japanese Yen's Unraveling Drama & Its Impact on Global Currency Markets

BoJ's Loose Policy Nightmare: The Japanese Yen's Unraveling Drama & Its Impact on Global Currency Markets

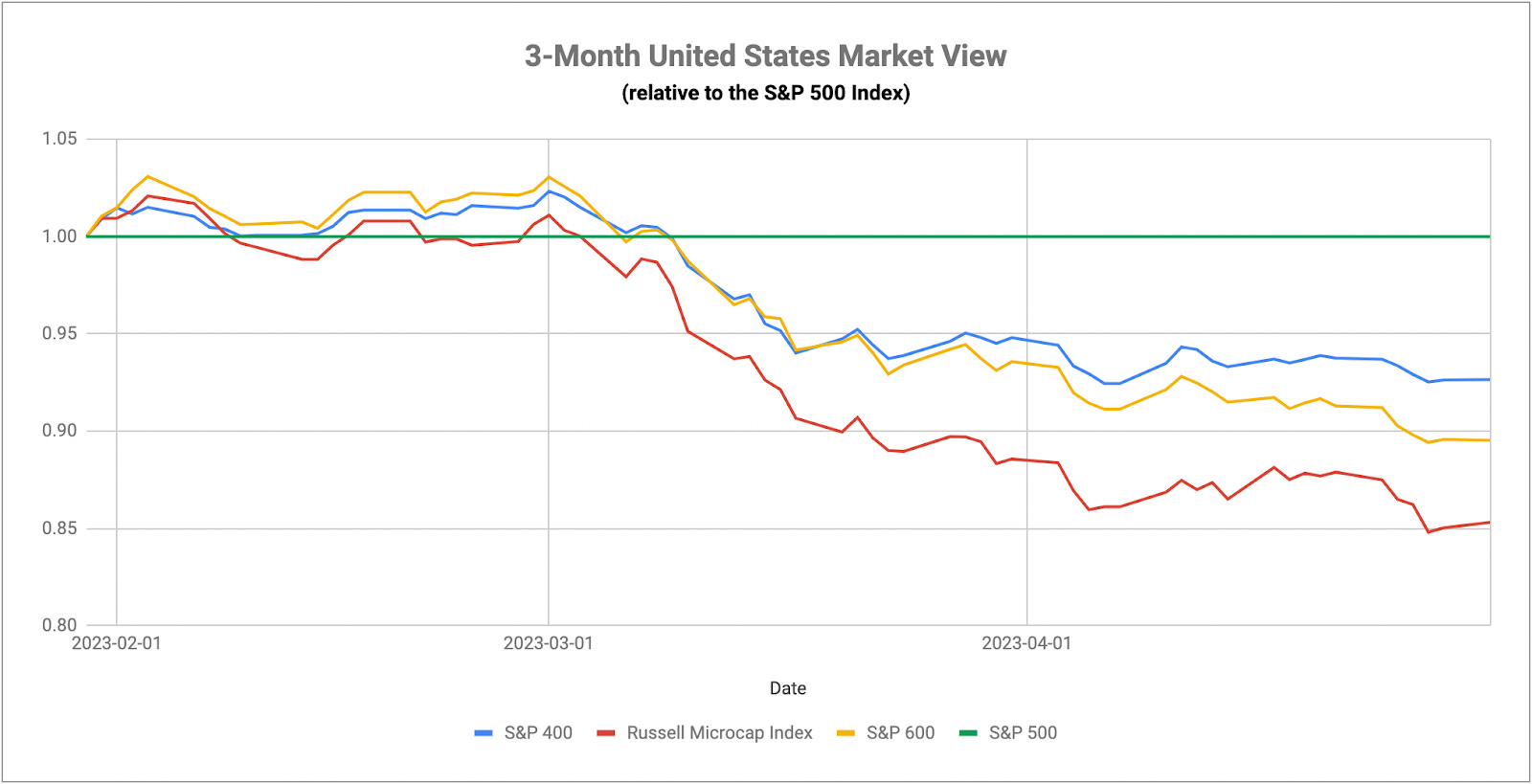

The Ugly Turn

It’s another big Fed week. So far, the markets think they know what to expect, but they’re still not optimistic. It’s now week 3 of the window where I said conditions look ripe for a correction. If you look at the headline indices against the backdrop of a generally positive earnings season, you may get the impression that everything’s fine and no correction has occurred. Take a look at the broader market though. The equal-weight S&P 500 is down more than 1% since April 17th even though the traditional index is nearly unchanged over the same time. The Russell 2000 is down 3%. The equal-weight tech index is down 4%. Regional banks are down 8%. There is very much a corrective phase going on under the surface. It’s just that mega-caps are masking what’s happening more broadly. Lumber has been signaling it. Utilities & Treasuries are still moving sideways in a choppy pattern, so it hasn’t been a universal risk-off signal, but the conditions I identified a few weeks ago look to still be in place.

The markets are widely expecting another quarter-point hike from the Fed this week, perhaps the last in this cycle, but it will be Powell’s tone that they’ll be watching. I think investors believe that a pause in future rate hikes from the Fed is synonymous with a dovish pivot where they’ll begin cutting rates imminently. I think a more likely outcome could be that the Fed stops with further rate hikes, but keeps the Fed Funds rate elevated until it gets more evidence that inflation is getting down closer to its target level. That would effectively accomplish the idea of additional QT without making conditions even tighter. I think Powell has enough ammunition - an overall positive Q1 GDP report, a strong earnings season, a tight labor market and stubbornly high core inflation - that it can, and perhaps even will, push rate cuts out into 2024. The wild card is the banking sector. Three of the country’s biggest bank failures have occurred in the past few months. I don’t think that will go unnoticed, but the Fed and the big banks seem to have a plan in place that backstops additional downside risk.

The other big market catalyst to watch here is the debt ceiling. Janet Yellen said this week that extraordinary measures could run out as early as June 1st, further accelerating the timeline for Congress and the White House to get a deal done. If we use 2011 as the playbook for how this whole thing could play out, we see similarities between then and now. Both will feature a split Congress with conservatives looking to get future spending cuts in exchange for a debt limit increase. Both risk stifling future economic growth as a result of limiting spending and both are expected to come down to the wire. In terms of financial market reaction, both U.S. stocks and Treasuries remained relatively flat up until about a week before the deadline. That’s the point where stocks plunged and Treasuries took off, despite the risk that the U.S. government could default on its debt. About two months after the debt deal was reached, the S&P 500 fell roughly 15% and long-term Treasuries were up more than 30% from pre-crisis levels. Of course, no two situations are alike, but things could get ugly the longer this gets dragged out.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.