Catching China's Falling Knife

Catching China's Falling Knife

Meanwhile, The Dollar

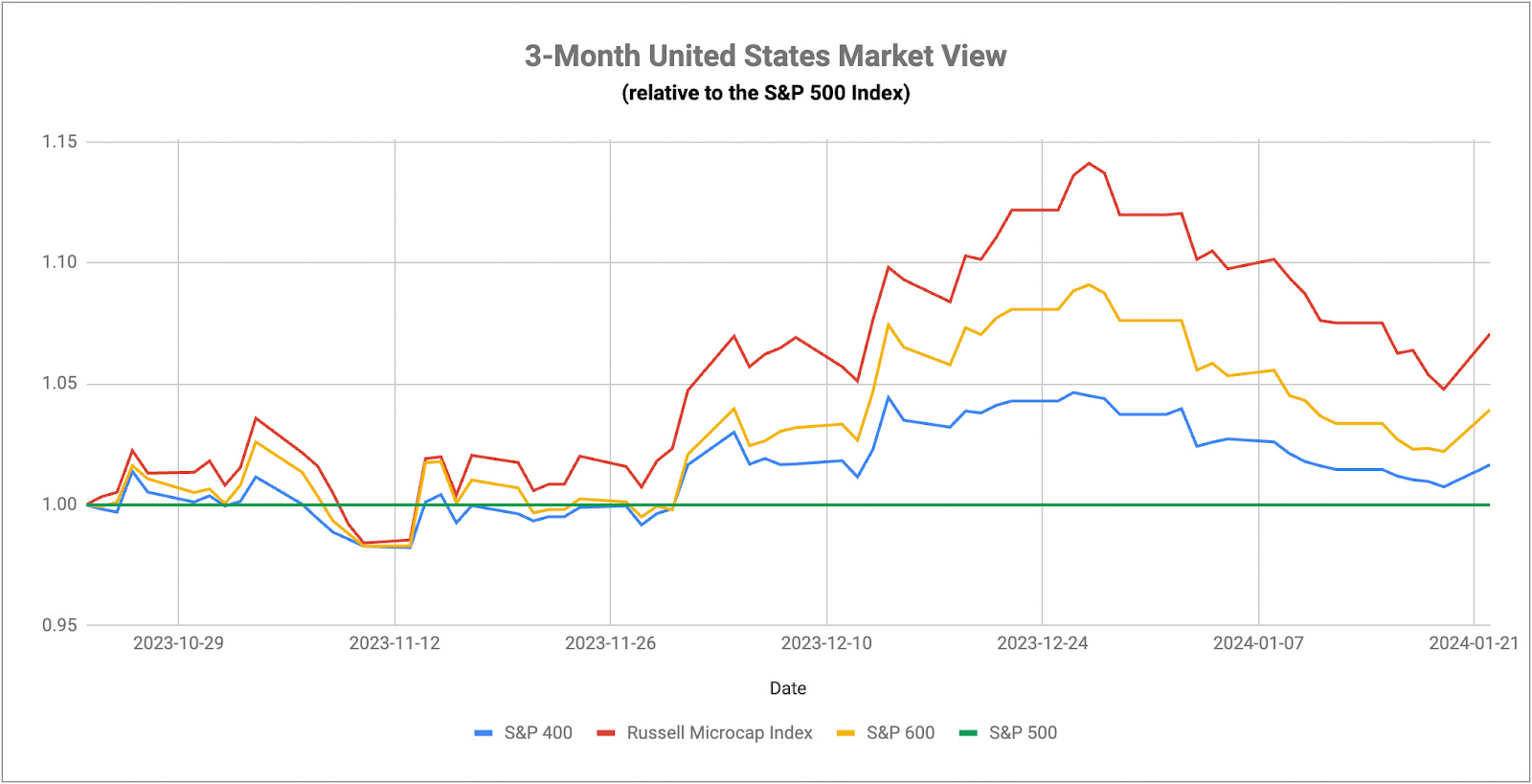

In the U.S. equity markets, the performance of small-caps relative to large-caps remains the key signal to watch here. It’s pretty clear looking at the chart above that small-caps have been driven heavily by the projected path of interest rates over the past two months. When the Fed telegraphed that the rate hiking cycle was ending just before the December meeting and then forecasted multiple rate cuts in 2024 at the meeting itself, small-caps got the cyclical recovery bounce that pulled industrials, materials and other sensitive areas of the market higher. The markets, however, got overzealous and decided to price in 6 rate cuts. Now that the economic data is still looking healthy and the Fed is trying to temper expectations, investors have grown a bit more hawkish again and some of those rate cuts are getting priced back out. We’re seeing that in 10-year Treasury yields, which have risen by about 35 basis points in the past month, and in U.S. equities, where the cyclical rally has faded and mega-cap tech has returned to take its place.

Small-caps are obviously more leveraged than large-caps and that’s a part of the problem here. The markets are indicating this isn’t a “rising tide lifts all boats” scenario like it was in December when a lot of 2023’s laggards started leading the way in a show of improved market breadth. Today, we’re back to where we were - large-caps, tech, growth and that’s about it. If the Fed follows through on its plan to keep rates higher for longer (and at this point I don’t think there’s any reason to believe that isn’t their thinking right now), small-caps are positioned to keep lagging until we get signs of a firmer pivot from the Fed. The longer the Fed waits, the greater the chances that the damage for small-caps gets worse before it gets better. A lot of smaller companies (and large ones as well for that matter) are facing a potential debt refinancing crisis over the next 24 months. If they’re forced to refi at elevated rates, we’re going to see a number of those zombie companies start to fail and that will send ripples throughout the risk asset market. If they can take advantage of lower rates, there’s a chance they can still survive and ultimately lead the market on the way back up.

From a fundamental standpoint, it’s tough to make a justification for why the Fed would cut a half dozen times in the next 12 months. If you want to make the case that we’re past peak inflation, so monetary policy levels can be normalized a bit, I think that’s fair and I think that’s what the Fed is trying to say. But to say that the Fed Funds rate needs to be taken down by 150 basis points while the core inflation rate is still trending at 4% annualized, real wage growth is at a 5-year high (not counting the volatile COVID period) and unemployment is still below 4% seems off-target. That could be to the continued detriment of small-cap stocks, but it could also be what helps the economy achieve the soft landing.

The Q4 earnings season is in progress and the results are decidedly mixed. Earnings growth is trending negative, which was kind of expected, but the banks look like they may be in a tougher spot than we thought. The financial sector has come in well below expectations, although some of that has been due to special assessments that have impacted earnings. Financials saw a nice rally in Q4 last year, but the short-term trend for interest rates appears to be higher at the moment. Bank margins were under pressure as rates were rising in recent years and could be again if the next leg in rates is higher again.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.