China's Full Blown Crisis

China's Full Blown Crisis

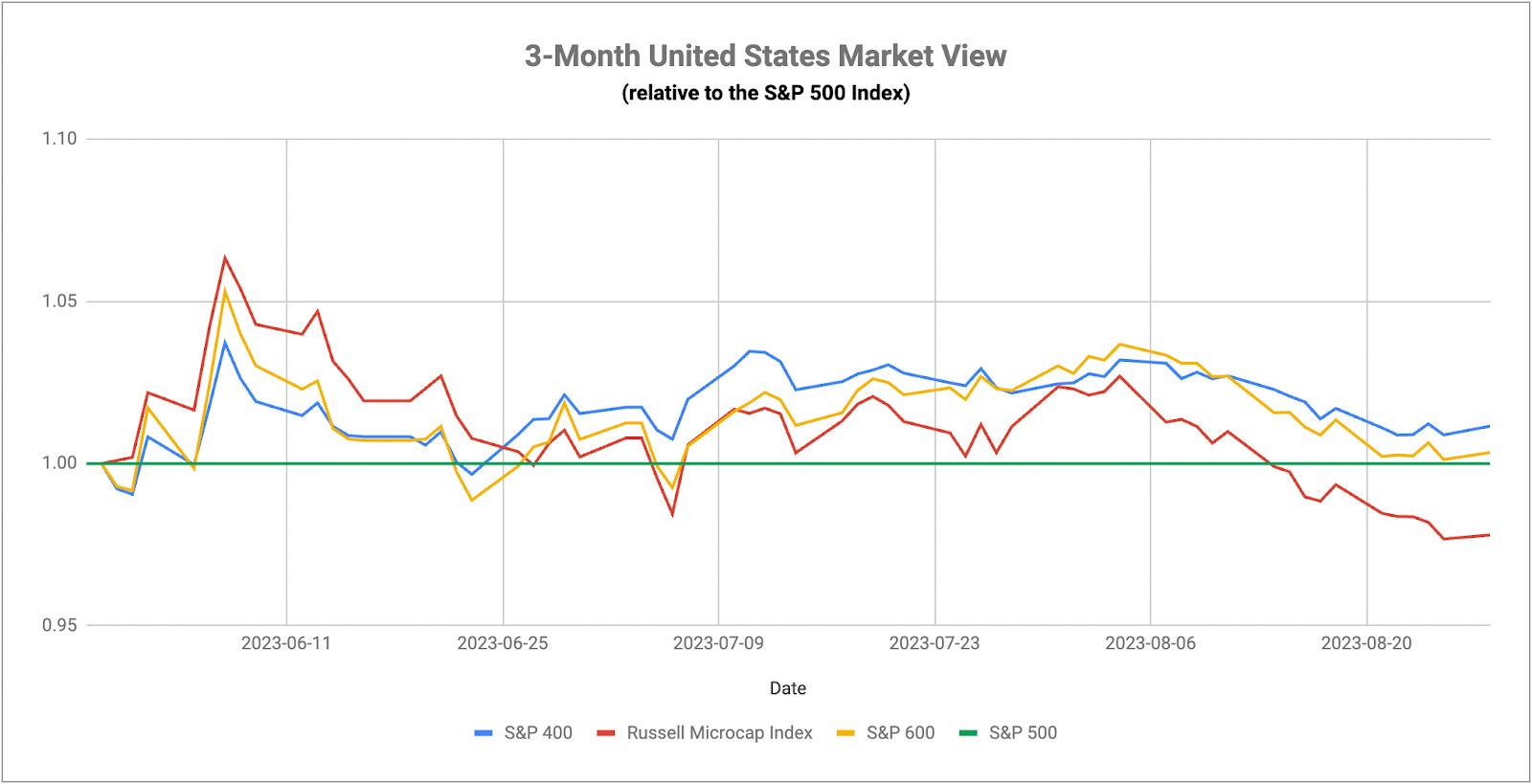

When Will It Matter For US Markets?

We’ve talked about how one of the key catalysts that would slam the brakes on the Fed’s plans to continue tightening conditions would be weakness in the labor market. While indications that the labor market is weakening have been largely minor to this point, it is looking like it’s getting closer to neutral than tight. The number of job openings in July fell to its lowest level since March 2021. While that is still running above pre-COVID trends, it’s been declining pretty steadily for more than a year. That could make Friday’s non-farm payroll data even more important. Like job openings, month-over-month job growth has continued to slow and supports the idea that we’re no longer in a “hot” jobs market, but one that looks more average than anything at the moment. Other figures, such as jobless claims, aren’t participating in the trend yet, but further weakness could indicate that the one thing that’s been propping up the economy might be starting to crack.

The trouble brewing in the commercial real estate space looks like it’s beginning to spill over into residential real estate. After a brief spike earlier in 2023, home price growth according to Case Shiller is beginning to slow again. It is looking like a tale of two markets though. Major metropolitan areas in the west, including San Francisco, Seattle and Las Vegas, are experiencing the sharpest declines, while midwestern cities, such as Chicago, are still increasing. For now, this looks like a case of the excess getting burned off of the most egregiously expensive markets, while prices are mostly holding up elsewhere. If you look at other figures, such as building permits and housing starts, it appears that a 7.5% mortgage rate is the limit where housing activity holds up. Considering Powell’s comments at Jackson Hole, it’s likely that 7% mortgage rates are here to stay, which should keep the residential sector vulnerable given what’s happening in the commercial space.

We still have a lot of economic numbers to come yet this week outside of just payrolls - GDP, inflation and PMI readings - and we could be seeing the early stages of risk-off momentum building. Over the past week or two, we’ve seen 10-year Treasury yields fall by 20 basis points as volatility remains high. The dollar has begun turning lower and gold is up about $50 an ounce from its mid-August low. This has been happening even as the S&P 500 is up 3% and the Nasdaq 100 is up 5% since the beginning of last week. We’re starting to see some really conflicting signals between risky and defensive assets. I think seasonal volatility is beginning to show up in the markets and the negative macro level data trends are urging some degree of caution here.

The Japanese economy continues to recover at a modest pace, but the latest data is likely to give the Bank of Japan some pause in how to proceed from here.

On the plus side, the country’s manufacturing sector continues to gently trend upwards over the past 6 months. While it’s still narrowly in contraction according to the latest PMI readings, it’s been doing so at a softer pace, making it a global outlier among other developed markets who are seeing manufacturing contract quickly. Composite PMI numbers are showing the economy still expanding and wage growth is still accelerating. On the other hand, the unemployment rate surprisingly ticked higher, but I don’t think that should deter the BoJ from strongly considering a tighter monetary policy position here. Whether it actually does or not is open to question since the central bank has implemented stimulative measures for years and won’t change their position easily or quickly. The BoJ and yield curve control are still among the biggest factors that could throw a wrench into market sentiment, although it doesn’t appear that any changes are imminent.

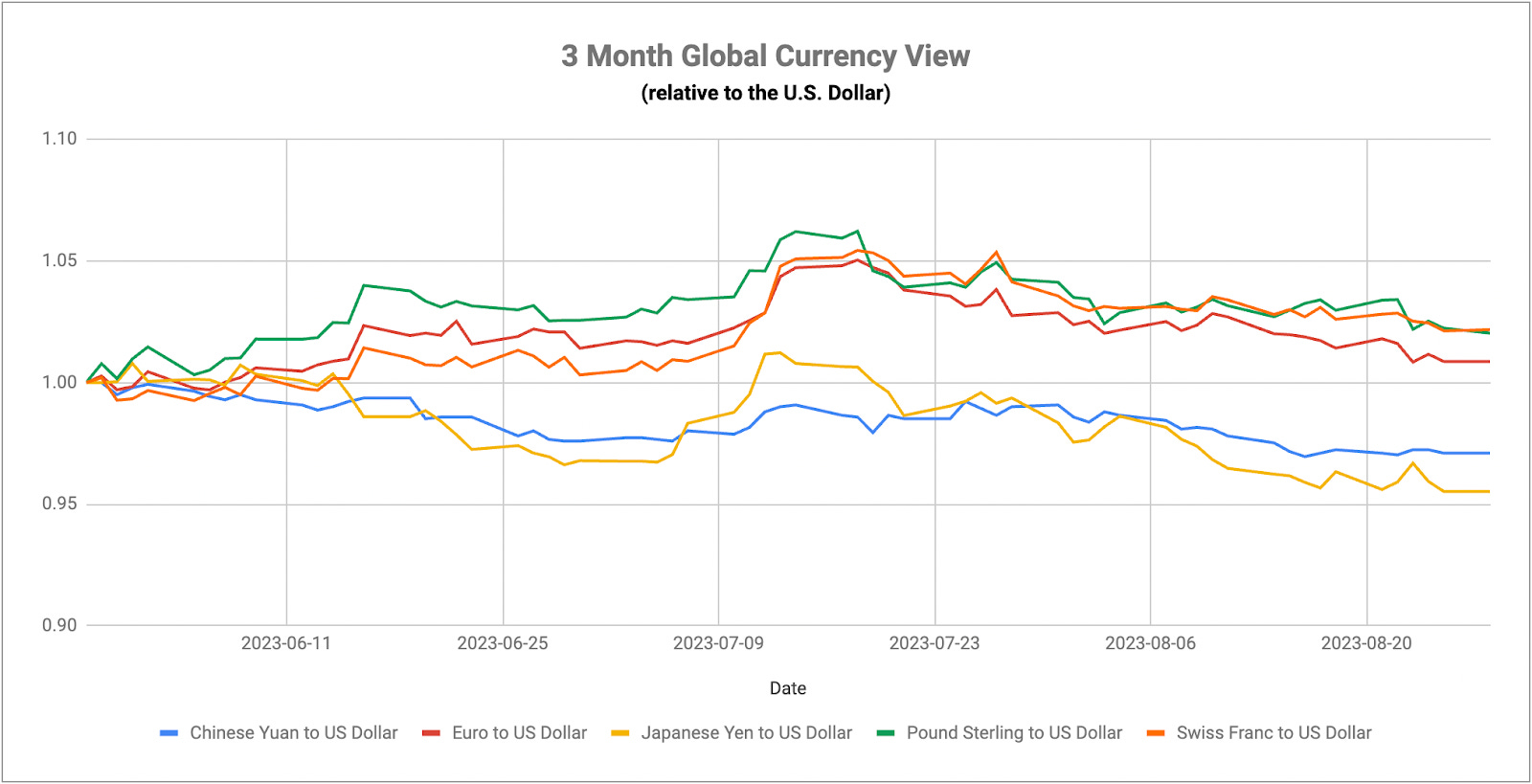

The Eurozone, however, is looking like a complete mess. The manufacturing sector in that region is in deep contraction and running at COVID era lows. The services sector has also slipped into contraction for the first time in 2023 and the latest composite PMI reading is the worst it’s been since 2020. Lending growth dropped to its lowest level since all the way back in 2015 and GDP numbers are barely avoiding the traditional definition of recession. All of this is happening with the backdrop of a sticky 5-6% annualized core inflation rate and a central bank that may have multiple quarter-point rate hikes still left in it. Compared to the United States and even Japan at the moment, Europe has a lot of issues and the steady decline in the euro relative to the dollar since mid-July is reflective of the sentiment that exists in this region.

The hot rumor of the week is that the PBoC is set to cut both mortgage and deposit rates this week. The former would occur to get consumers some direct financial relief, while the latter would encourage money to be drawn out of financial institutions and into the economy. Cutting the two in combination, in theory, would reduce the cost of deposits for banks, which would in turn give them the ability to cut mortgage rates to preserve existing margins. This is the latest step in an accelerating process by the PBoC and the Chinese government to stop the bleeding of continued consumer weakness. A huge government stimulus package would have the biggest positive impact for recovery, but China is already a heavily indebted nation and further money printing & debt issuance would put the government in a perilous financial condition. The rate cuts are expected to be between 5 and 20 basis points, the latter of which would be a huge move by a central bank that typically only moves in 5 basis point increments.

China’s real estate sector issues continue to morph into a full-blown crisis that could take down the entire economy. The latest estimate from Gavekal is that debtholders are currently owed roughly $400 billion in payments, a number that could very well be bigger if all financial information were to be disclosed. Country Garden, one of the country’s top developers, is seeking out a 40-day grace period to make payment on a maturing half billion dollar bond issue and it’s now selling off assets to raise cash. Other regional developers have reported huge declines in profits over the past year. China Overseas says its profits fell by 20%, while Poly Property reports a 50% decline. Real estate accounts for about ⅓ of China’s GDP and it touches almost every area of the nation’s economy from people who have jobs and earn wages from the sector to those businesses who are suppliers of materials & services to developers. Those people are struggling to get paid right now during a time when conditions keep deteriorating on almost a weekly basis. China Evergrande shares just started trading again for the first time in a year and half and almost immediately fell by more than 80% in value.

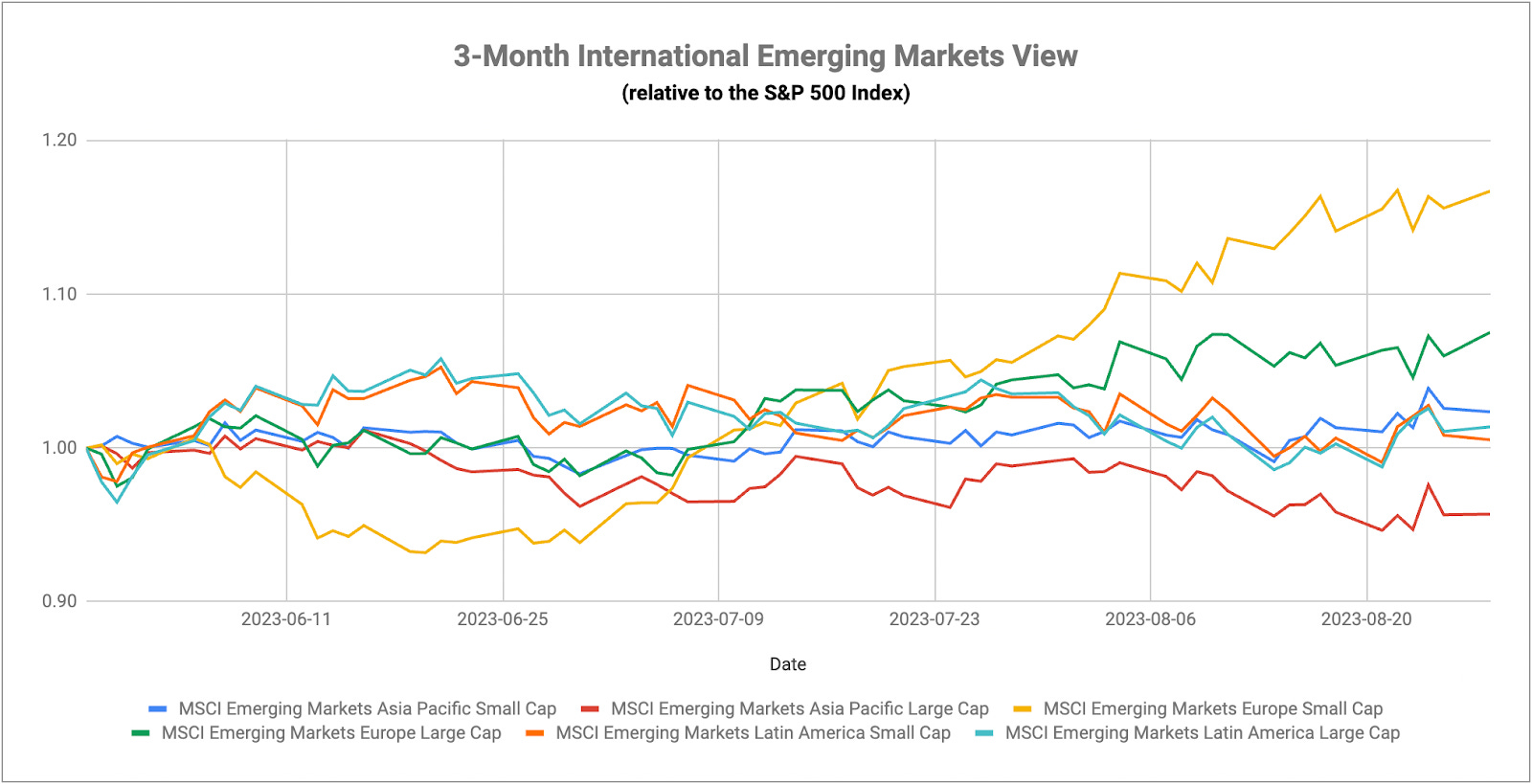

While most of the major developed markets are still raising rates (or at least holding them where they are), rate cuts look like they’re becoming the growing trend in emerging markets. The Hungarian central bank cut by another 100 basis points this week, bringing its total to 400 since May of this year. Brazil made its first 50 basis point cut in early August. Chile cut by 100 basis points in July. It makes sense since emerging markets were leading the world in hiking rates that they’re now leading in cutting rates as well. This will likely be taken as encouraging by investors, but it’s important to remember that rate cuts are typically associated with weakening conditions. Inflation, of course, played a huge part in this cycle, but don’t be surprised if we start seeing bigger central banks begin to consider cutting rates over the next 2-3 quarters as well.

The dollar continues to remain strong almost by default. It’s unquestionably been one of the strongest economies in the world by comparison and that alone has brought interest to dollar-denominated assets. Japan & China are still loosening. The ECB and BoE have lagged the Fed and are now trying to avoid recession altogether. Interest rate differentials put the dollar in an advantageous position, but so too do economic conditions. That’s kept the dollar on a nearly unstoppable ascent since the first half of July. Such a straight line rally is probably due for a breather and this week’s round of economic numbers may provide the excuse. Labor market data has already resulted in a reversal this week and it may continue depending on how non-farm payrolls and PMI numbers look later this week.

The euro is the biggest part of the dollar index basket and that’s performing perhaps the worst of the major world currencies. Almost all of the data coming out of that region looks ugly, but another rate hike by the ECB might help generate a modest rebound. The British pound could be in line for a similar boost should the Fed decide to keep holding steady. China is trimming rates left & right and may yet drop a big stimulus package on its economy, so the prevailing trend here is still down. The BoJ remains pretty tight-lipped about its policy plans, but it’s tough to imagine it loosening before tightening again.

The Lead-Lag Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by the Lead-Lag Report are independent of other services provided by Lead-Lag Publishing, LLC or its affiliates, and positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors and employees expressly disclaim all liability in respect to actions taken based on any or all of the information on this writing.