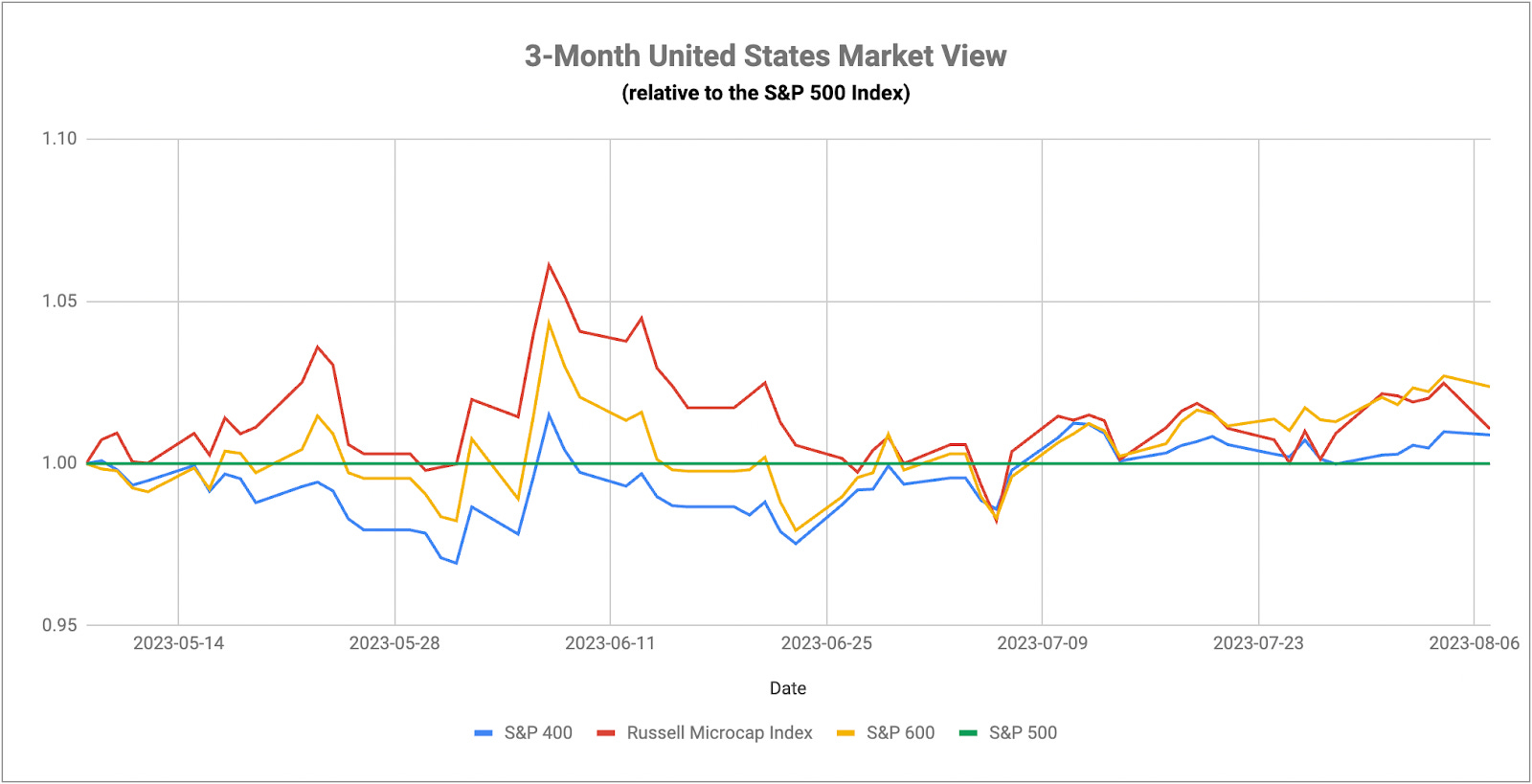

Conditions Are Deteriorating

Conditions Are Deteriorating

And At A Rapid Pace

If Fitch’s downgrade of the U.S. government’s credit rating wasn’t enough to shake investors out of their lull and realize that larger credit problems are building, Moody’s ratings downgrade on a big chunk of the banking sector should do it. In total, the agency cut the ratings on 10 mid/small size banks, changed the outlook to “negative” on 11 others and put six of the big banks, including Bank of New York Mellon and Northern Trust, under review. It’s perhaps the strongest sign yet that the fallout from the banking crisis earlier this year might be more widespread than originally thought. Moody’s cited the risks of holding long duration fixed income securities on their balance sheets (the very same issue that sank Silicon Valley Bank and Signature Bank) as well as the decline in the commercial & office real estate spaces, where smaller banks are particularly exposed.

This is why I’ve been pounding the table on the risks of the lagged effects of the Fed’s rate hiking cycle. Much of the work that was done by the central bank in 2022 is only showing up in economic activity today. More pressure is very likely ahead and the financial & real estate sectors are already showing signs of buckling. I noted a tweet from Bill Gross earlier this week where he talks about how the conditions that hit SVB and others this year - long duration risk and pervasively high interest rates - are likely still present elsewhere. Moody’s seems to agree and it’s very interesting that it’s at least considering downgrading the big banks as well as the smaller regional ones. We read throughout that the risk was in the regional banks, but the big banks were in good shape. Maybe that’s not the case after all.

The one thing that’s been encouraging to see this week is how stocks and bonds have interacted in their traditional risk-on/risk-off manner. The inverse correlation, if it were able to hold here, would suggest that the markets are beginning to move past the impacts of the Fed’s interest rate hiking cycle and other factors, including inflation, and resuming looking at Treasuries as a risk-off asset. So far this week, utilities, Treasuries and the dollar outperformed when stocks have declined and vice versa. The path of returns is going to be really important as we move towards the end of the earnings season. If we see investors begin taking risk off the table because they’re concerned about the credit environment and it’s utilities and Treasuries taking the lead in their place, it could be a larger sign that this bear market rally could be coming to an end.

A few other odds and ends: Lumber prices are still well below their July levels indicating that it’s not buying into the cyclical rally we’re seeing in stocks. UPS just lowered its forward guidance, which could be a sign that it’s seeing weakness ahead for the consumer. And consumer credit card debt just topped $1 trillion for the first with student loan payments about to resume. Don’t let anyone tell you otherwise. Conditions currently are deteriorating at a quicker pace.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.