Consumer Activity Is Topping Out

Consumer Activity Is Topping Out

Meager Retail Sales Numbers Suggest The Lags Are Starting To Hit

This week’s retail sales numbers again provided more evidence that consumer activity is topping out. May’s meager growth of just 0.1% missed expectations along with a downward revision of April’s number to -0.2%. That marks the 3rd month in the past eight where retail sales have been negative and brings year-to-date sales growth to 2.3%, well below the 3-4% clip we saw in the 2nd half of last year. Optimists might point to the fact that a negative driver to these numbers was sales at gas stations. While that’s true, it also spotlights a trend I’ve been talking about a lot lately, softening global energy demand that typically picks up around this time of year. Taking all of this together, this isn’t a terribly encouraging report if you feel that the consumer is going to carry us through this economic slowdown. High interest rates and inflation are clearly still having an impact on purchasing power and I think we’re in the midst of seeing this play out.

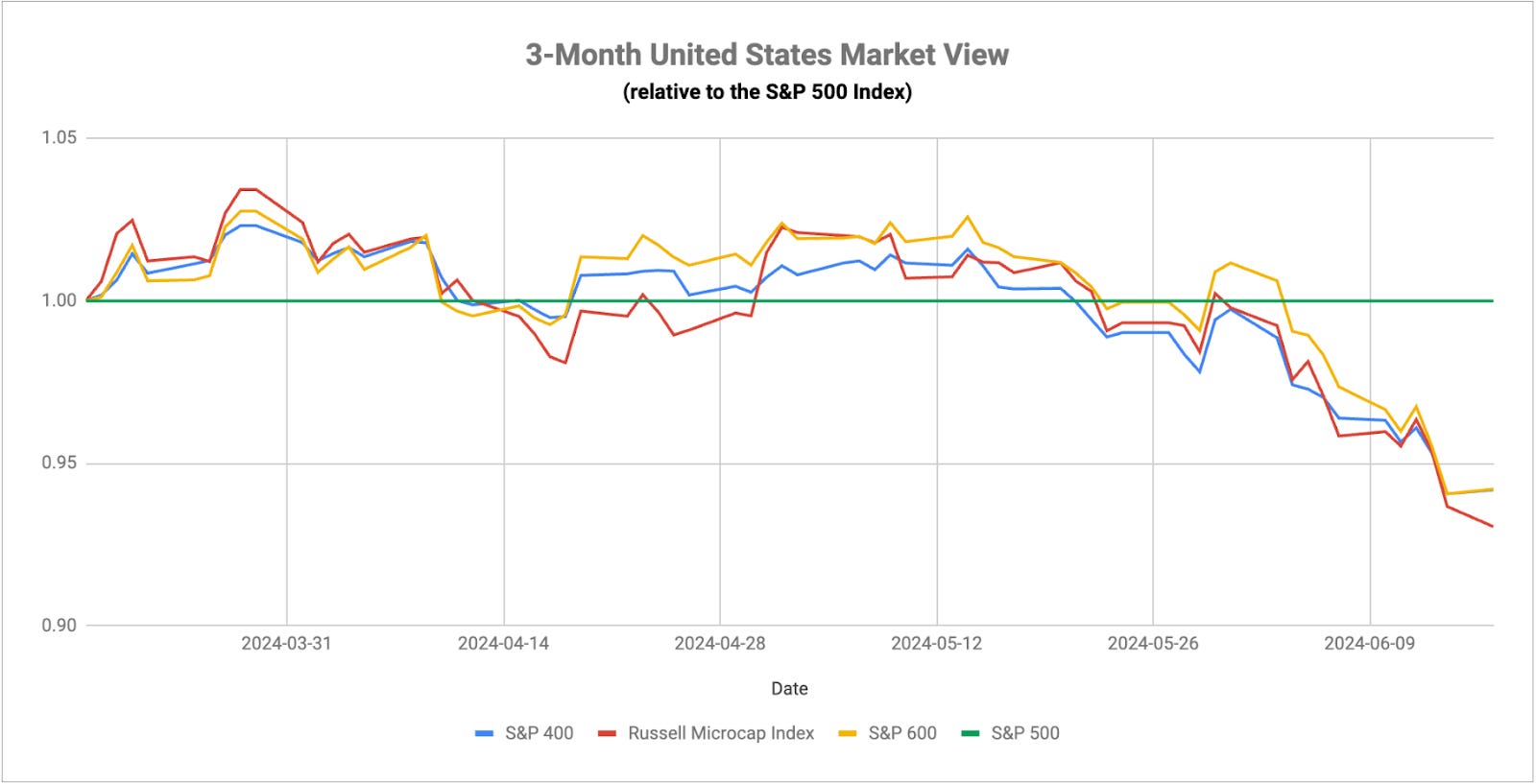

As I alluded to in yesterday’s leaders/laggards report, this is becoming a dangerously thin market environment. Just last week, every major sector except tech underperformed the S&P 500 to go along with small-caps, dividend and value stocks. Market breadth on the Nasdaq has been trending lower for more than a month even though the index is up nearly 8% over that time. All major market signs are pointing towards a, at best, sideways trending U.S. equity market and more likely one that’s getting worse. The performance of small-caps, whose deterioration is actually accelerating here, is perhaps the most telltale sign of real market sentiment. This group should be getting the biggest boost from both falling interest rates and the possibility of Fed rate cuts as soon as September. The fact that neither is having a positive effect suggests that there might be more of a flight to safety trade happening here than is obvious just by looking at the major averages. When conditions improved in the 4th quarter of last year, small-caps led large-caps by a wide margin. Today, monetary conditions are improving again, yet small-caps are underperforming badly. A lower Fed Funds rate tends to correlate with falling stock prices because the Fed usually cuts when economic conditions are getting worse. Small-caps could be telling us that this is the case today as well.

Speaking of rate cuts, the markets seem to be learning nothing from the beginning of the year and are, again, getting overly optimistic about rate cuts. Powell indicated a new forecast of one in 2024 and the markets immediately priced in two. Currently, the futures market says there’s a ⅔ chance the Fed will cut in September and will cut a second time in December. It’s still too early to know if May’s cooler than expected inflation reading is the start of a new downtrend (history suggests it probably isn’t). The St. Louis Fed president this week said that there should be months or even quarters worth of data of slowing inflation data before considering a cut (for the record, he’s not a voter though). I think we’re in this spot again where stocks (or at least some stocks) are rallying on the idea that the Fed is coming to the rescue only to be disappointed soon when Powell reiterates his previous hawkish stance.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.