Do Regional Banks Deserve To Be Getting Pulled Higher By Small Cap Momentum?

Do Regional Banks Deserve To Be Getting Pulled Higher By Small Cap Momentum?

The Value Trade In Focus

While the markets remain enamored with the small-cap rally, there are other areas of the market that are experiencing a renaissance of their own. One of those groups is value stocks. This is the segment of the market filled with things, such as financials, healthcare and industrial stocks. You know, the sectors that have largely gone ignored as the Nasdaq 100 and magnificent 7 ripped higher.

Since July 10th, when the market rotation unofficially started, value has outperformed growth by more than 10%. Over the same time, the Russell 2000 has beaten the S&P 500 by 13%. The fact that these two rallies are happening at the same time - small-caps leading is generally considered bullish, while value stocks leading is considered more bearish - shouldn’t actually be surprising. The Russell 2000 trades at a 40% valuation discount to the S&P 500. Small-caps are effectively a value play themselves.

The value trade is pulling a lot of segments of the market higher right now, even one that may not seem like it deserves it - regional banks.

Why Are Regional Banks Rallying Despite The Risks?

Regional banks jumped into the spotlight back in March 2023 when Silicon Valley Bank and Signature Bank failed. The primary reason was improper risk controls. These banks overexposed themselves to long duration bonds in order to squeeze out a little extra yield in a low rate environment. When the Fed started raising interest rates aggressively, those bonds suffered huge losses and eventually rendered the banks insolvent. Within a few months, First Republic Bank, Citizens Bank of Sac City, Iowa and Heartland Tri-State Bank all went under.

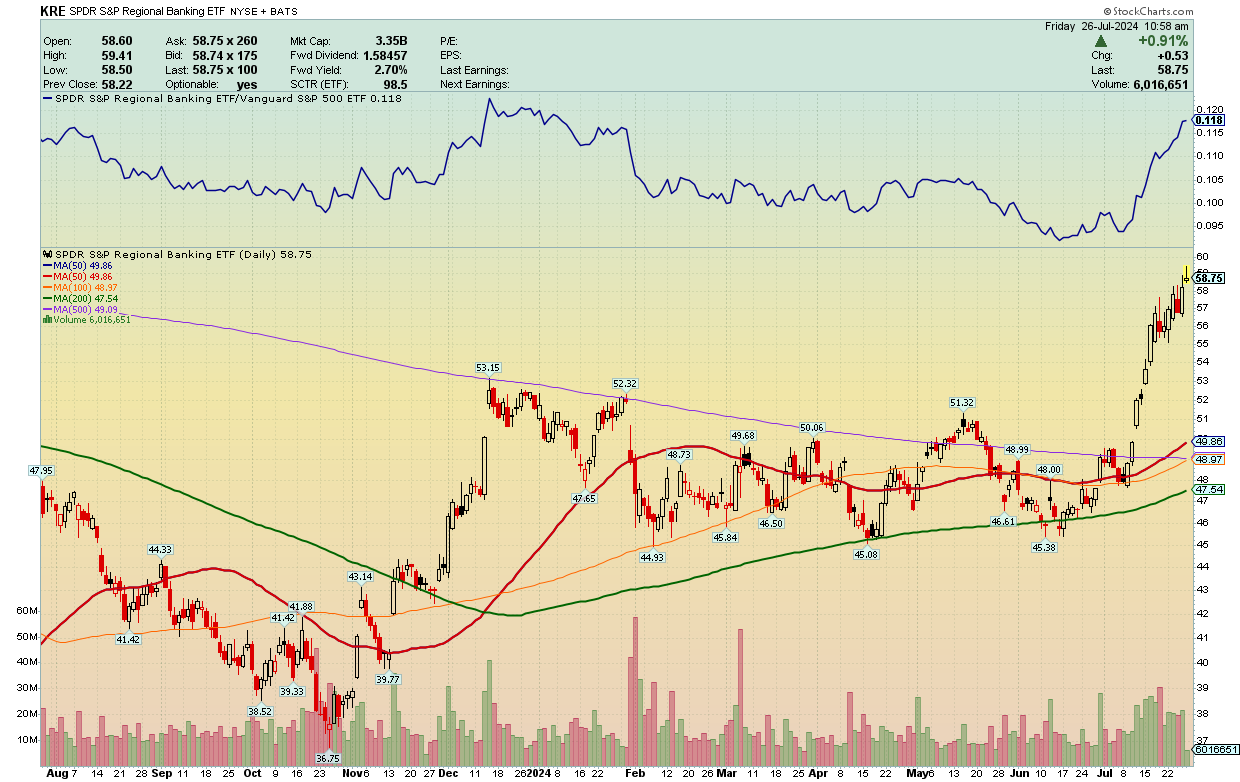

In the 16 months since those first failures, regional banks still haven’t come close to getting back to where they were relative to the S&P 500. But look what’s happened over the past few weeks.

While this has been great news for long suffering regional bank shareholders, the group is up 20% since July 10th, it raises questions about whether the group really deserves it.

The biggest question surrounds their exposures to the commercial real estate sector. Regional banks generally have larger relative exposures to CRE than the big banks. Why? Commercial real estate tends to be much more niche and local. The desire to build and develop depends heavily on local conditions since different markets can experience very different levels of economic health. Regional lenders can specialize in local market knowledge and are often preferable to larger banks, who may have a broader worldview.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.