Here Comes The Bank Of Japan Surprise

Here Comes The Bank Of Japan Surprise

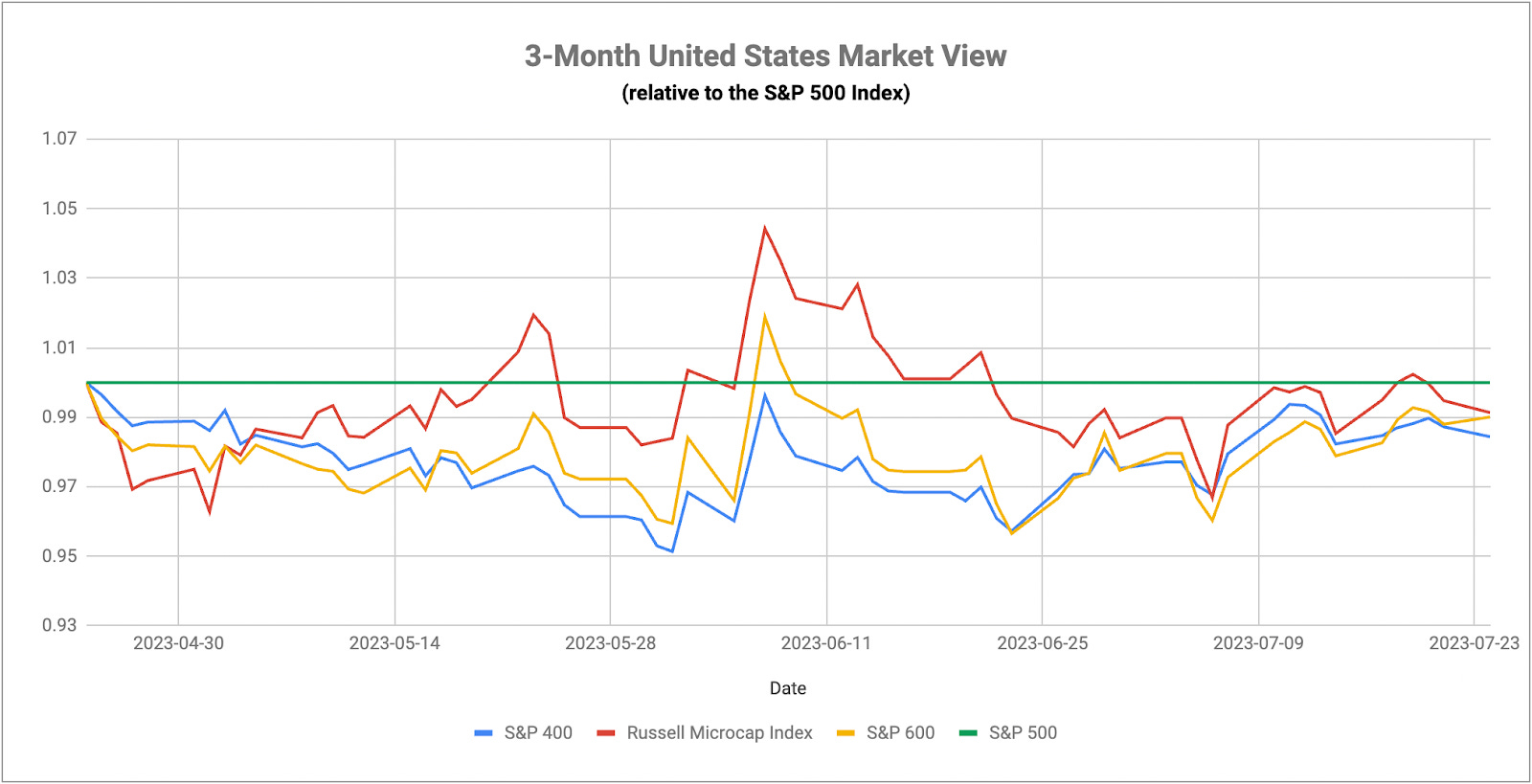

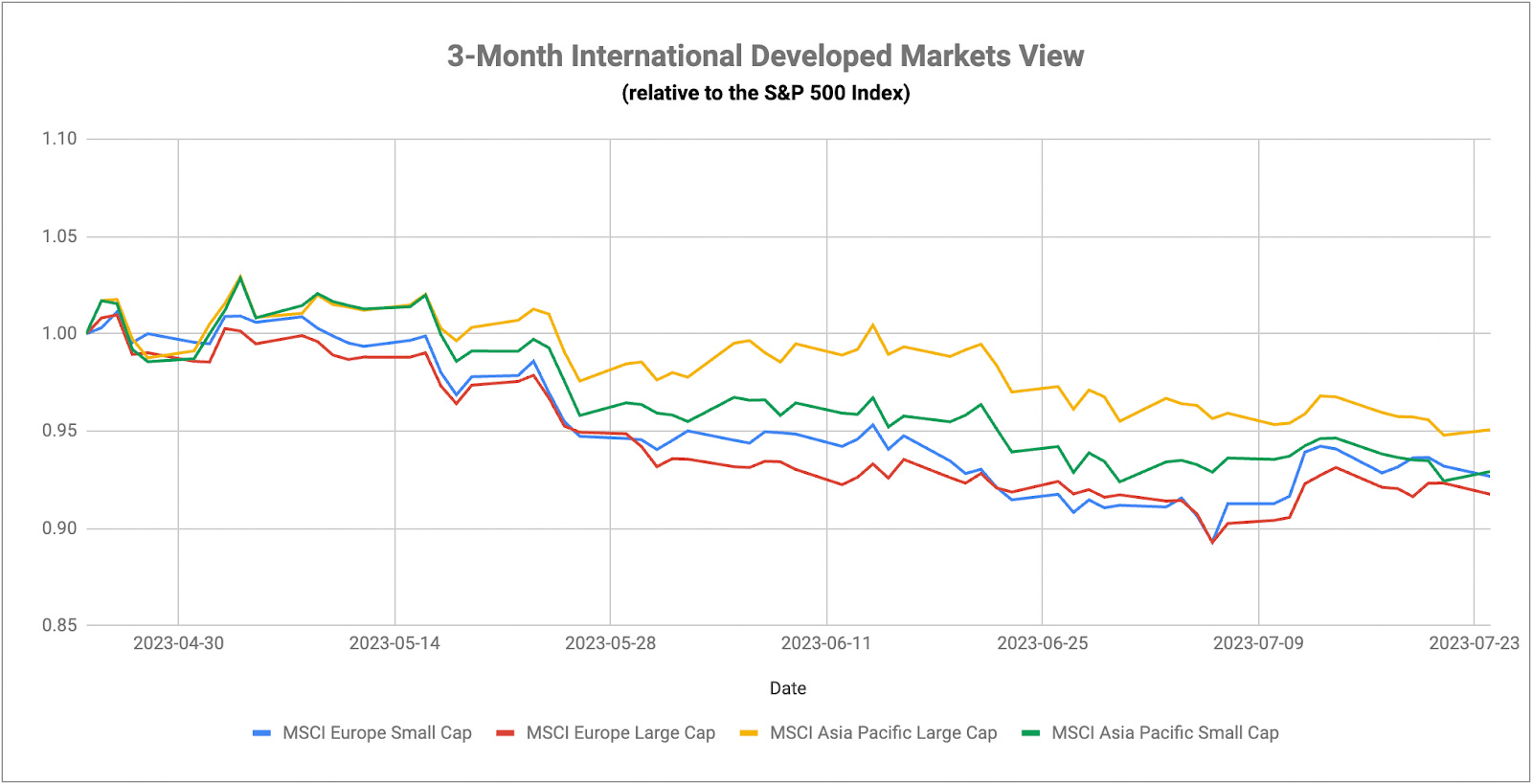

The Most Important Central Bank Now Isn't The Fed

Unlock the power of AI to beat the market. Danelfin brings AI technology, once reserved for hedge funds and elite investors, to everyone, revolutionizing stock & ETF picking. Start now for free.*

*DISCLAIMER – PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided in the link is solely the creation of Danelfin. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the link or make any representation as to its quality. All statements and expressions provided in the link are the sole opinion of Danelfin and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the link.

We have yet to see the carryover from last week’s risk-off reversal, but there are plenty of catalysts to make it a looming threat. Q2 earnings season has generally been pretty positive so far, but the results from the big mega-cap tech names later this week are likely to drive the narrative. So far, we saw good results from Google, mixed numbers from Microsoft and a huge miss from Snap. Results to come later this week could be particularly interesting since they might offer some insight into how companies and consumers are spending or if they’re beginning to cut back in anticipation of a tougher economic environment ahead.

The main event, however, is going to be the Fed. The market has fully priced in a quarter-point hike this week, but no more than a 40% chance of a second rate hike beyond that. Given that core inflation in the U.S. is still running at a 4-5% annualized pace despite the headline rate looking likely to fall below 3% in July, I think we’re probably looking at another “skip” from the Fed instead of an outright pause. Price pressures are still high enough that Powell will be unable to take his foot off the gas anytime soon, but conditions may have cooled enough that further action isn’t warranted for now. I expect the Fed will be open to hiking again if core inflation is unable to come down, but it may take another month or two of data before determining the overall trend. The fact that core inflation came in at just 0.16% month-over-month in July could be a good sign that the fever is about to break.

Forward guidance from the Fed is what everyone will be watching. Will Powell’s tone remain hawkish or is he going to pivot towards neutral? Will he say the Fed will continue hiking if it’s needed or will he say that more rate hikes are “likely”? Most investors will pay attention to the wording here and likely react to it since volatility usually picks up in the immediate aftermath of both the rate announcement and the commentary.

On the economic front, global PMI readings show activity slowing all around the world, including on the services side, which to this point is what’s been holding up the global economy. July’s PMI numbers in the U.S. showed a complete reversal of the trend that’s been in place for months. The services PMI slowed to its lowest reading since February, while manufacturing picked up to its highest level since April. The composite PMI reading of 52 shows that the economy is still expanding, but it’s also down for the 2nd consecutive month. If the services segment of the economy slips into contraction and stays there, it might be very difficult to avoid a recession. With the Eurozone looking ugly on a lot of fronts and Asia struggling to get things going, the global economy could break down quickly if the U.S. isn’t able to prop things up.

The theme throughout the world outside of the U.S. this week has been slowing economic growth.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.