High Risk, Poor Performance

High Risk, Poor Performance

A Likely Distribution Cut All For A Premium Price

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

Even as credit conditions continue to deteriorate, the commercial loan market starts to contract and the Chinese real estate market looks ready to implode, junk bond prices just keep outperforming. Investors satisfied that the economy is in good shape as long as consumers keep spending and jobs remain plentiful (with a potential assist from the Fed) seem to have no interest in pricing in credit risk at the moment. Even as a huge increase in corporate debt refinancing begins in the 1st quarter of this year at much higher interest rates, investors seem to feel more than comfortable reaching for yields while ignoring some of the underlying fundamental risks.

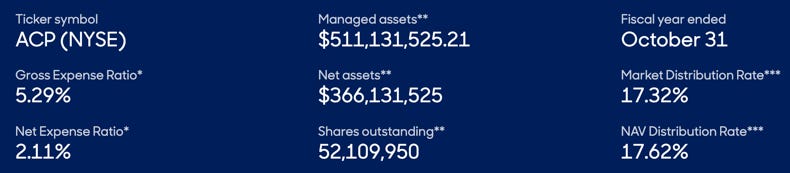

The abrdn Income Credit Strategies Fund (ACP) aims to take advantage of this trend. However, it’s taking a lot of risk to get there, both through security selection and the use of leverage. Right now, an artificially high yield of 17% is luring in unsuspecting income seekers who might be buying a package that looks shiny on the outside but has a lot of broken parts on the inside. ACP is a large and popular fund, but are investors getting appropriate value?

Fund Background

ACP seeks to achieve its investment objectives by opportunistically investing primarily in the debt & loan instruments of issues that operate in a variety of industries and geographic regions. The fund may invest, without limitation, in credit obligations that are rated below investment grade by one of the major ratings agencies. The fund also utilizes leverage in order to enhance yield and total return potential.

On the surface, this is sort of your standard actively-managed junk bond fund, except that it invests in lower quality bonds than most funds and is more globally diversified than most. The problem here (as it is with a number of funds) is “is the yield masking the risk”. ACP has managed to build a pretty rock solid distribution history, but a steadily declining NAV has pushed the yield about as high as it’s ever been. I see a number of red flags with this fund that need to be examined more closely because this fund is much more than just an attractive yield.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.