Housing Boom to Lumber Crash: Now Is Not The Time To Pay Attention To Tech Stocks

Housing Boom to Lumber Crash: Now Is Not The Time To Pay Attention To Tech Stocks

Priorities

Investors seem to be trying hard to talk themselves into the idea that a soft landing isn’t just possible, it’s likely. If GDP growth is still positive, the labor market is still strong and the Fed may finally be done raising rates (which doesn’t look like a sure thing any more), we shouldn’t be that worried about recession, right? There was a brief scare when a few regional banks were failing, but the S&P 500 just touched its highest level of the year. Things can’t be that bad, right?

Let’s revisit the one asset class that keeps telling us that things aren’t alright - lumber. It’s down about 80% from its post-COVID peak and has been in a steady downtrend for nearly a year and a half.

You know my belief on the importance of lumber - lumber is a tell on housing and housing is a tell on the economy. If lumber prices are rising, it stands to reason that the economy is probably doing well and vice versa. Still, lumber is a leading indicator and we have to respect the lag. Lumber prices signal a lack of demand today. It takes time for that to filter through economic activity including the home construction process all the way down to the end consumer purchase. After a year and a half of crashing prices, we’re finally starting to see the effects of this filter through the system. I’ll touch on that more in a moment.

From an investment standpoint, the behavior of lumber in conjunction with the behavior of gold prices is concerning. The last time these two asset classes really diverged was in the second half of 2020 when we were just coming out of the COVID bear market and consumers were starting to swim in stimulus cash. Lumber shot higher and gold sank for several months, a signal which proved correct for risk asset prices.

Today, we’re seeing the same, but in the opposite direction. Gold has been climbing higher since December, suggesting a fairly strong risk-off signal. I think we’ve seen some of that playing out since April, but the outperformance of a handful of mega-cap stocks are masking some of the market’s true weakness.

The reason why lumber is so important is because it’s really the best indication of the wealth effect. Most people have their net worth tied up in their house. For many, it’s the only real asset they have. If they see home prices rising (or at least holding steady), they’re probably going to feel better about where they’re at financially, which could lead them to feeling more comfortable spending. If they look at Zillow and see comparable home prices falling, they’ll probably begin being more cautious and slow down their spending.

Now that we’re seeing some of those lagged effects of lumber’s price decline showing up in the numbers, we might finally be in the early innings of a big swing in consumer sentiment.

Let’s take a look at some of the latest figures and what they’re telling us.

Most of the housing market activity centers around existing homes, so it makes sense to use this metric as a fairly broad proxy.

In early 2022, existing home sales figures started dropping at almost the same time that lumber prices started plunging. I’m not sure this trend has as much to do with lumber prices as it does mortgage rates. Higher rates have significantly reduced how much home potential buyers can afford and caused some to pull themselves out of the market altogether.

We got a spike in activity in early 2023, which was consistent with the surprising strength in other numbers, including GDP and retail sales. That helped fuel this year’s early gains in risk asset prices, but it’s beginning to look like a temporary phenomenon, not a trend.

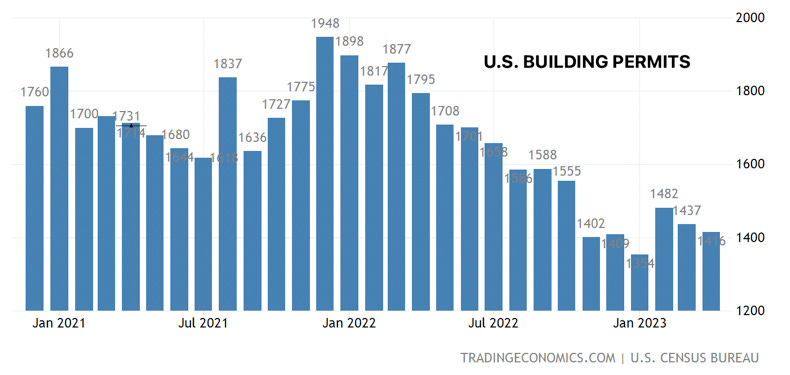

The chart for U.S. building permits looks almost identical to that of existing home sales and probably for the same reasons. People considering breaking ground on new homes are going to be less inclined to move forward if the cost of doing so is going to be much higher than anticipated. We know that affordability and declining consumer sentiment have been issues in this cycle, which resulted in the percentage of new home contracts getting canceled was skyrocketing. This is a pretty good reflection of that.

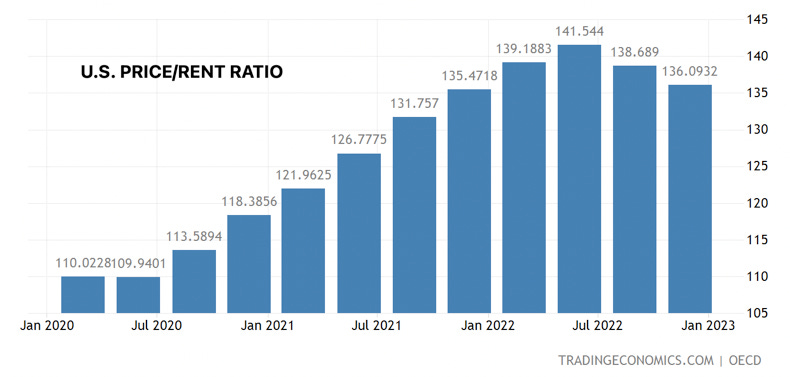

Home prices are usually one of the last dominoes to fall in the entire timeline, but those are finally starting to turn lower as well.

This ratio has been a function of both the numerator & denominator rising rapidly and has been a major variable in the high inflation problem over the past year. Today, both home prices and rental rates are coming back down. The latter was almost inevitable as rents were climbing at a clip of more than 10% year-over-year. As those 12 month leases start rolling over, rental rates are coming back down to earth.

Home prices, however, are starting to fall faster. The refi market has become virtually non-existent and higher mortgage rates have drastically impacted how much home people can afford. The inevitable result is that home prices start coming down to compensate and this is what we’re seeing today.

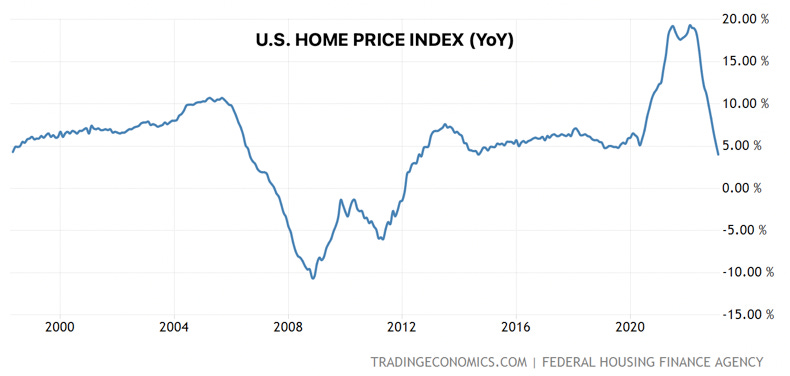

The rate of change in home prices has also turned drastically lower. Based on the past few months, we could soon see the annualized rate of change in home prices approach financial crisis levels. Part of this is some of the COVID era excess getting worked off, but most of it is due to affordability and economic conditions. As wage growth continues to decelerate and the unemployment rate creeps higher, the situation is likely to get worse before it gets better.

While this trend shows up most obviously in the data above, it’s also starting to carry over into corporate bottom lines.

Home Depot said just this past week that roughly half of its quarterly decline in sales was due to falling lumber prices. A lot of companies won’t be as directly impacted by falling lumber prices as Home Depot, but we are seeing the generalized behavior in stocks that is consistent with a broader economic slowdown.

Small-caps have been underperforming large-caps badly in recent months. Consumer discretionary stocks are lagging consumer staples. Pretty much every cyclical sector has underperformed the S&P 500 over the past month. I know people look at the Nasdaq 100, see it’s up about 24% on the year and figure that the good times are back, but there’s a lot here, both intermarket relationships and economic data, that suggest a market and an economy that’s in trouble here.

The Lead-Lag Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by the Lead-Lag Report are independent of other services provided by Lead-Lag Publishing, LLC or its affiliates, and positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors and employees expressly disclaim all liability in respect to actions taken based on any or all of the information on this writing.