How Many Ways Can I Say No To This 16% Yielder?

How Many Ways Can I Say No To This 16% Yielder?

Many.

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

A lot of people might be surprised to find out that one of the best-performing fixed income asset classes over the past year is emerging markets bonds. It may seem counterintuitive given how EM stocks have been lagging, but the reasoning actually makes sense. Expectations were low and some governments did default on their debt, but several of them were able to make deals to restructure their debt. For others, a rebound in commodities and a belief that a soft landing isn’t entirely out of the question has brought buyers back into the space. These regions still face many challenges, but the notion that “things aren’t that bad” can ignite rallies.

The Virtus Stone Harbor Emerging Markets Total Income Fund (EDI) is one of those funds that’s benefited, albeit with a high degree of volatility. Investing in lower-grade emerging markets debt right now comes with a high degree of corporate, government and geopolitical risk, but value is high, the dollar is weakening and we could be entering a decade of international investing once we get past this era of high inflation and recession risk. Yield seekers, however, need to be careful about chasing extremely high yields because they are often fraught with danger.

Fund Background

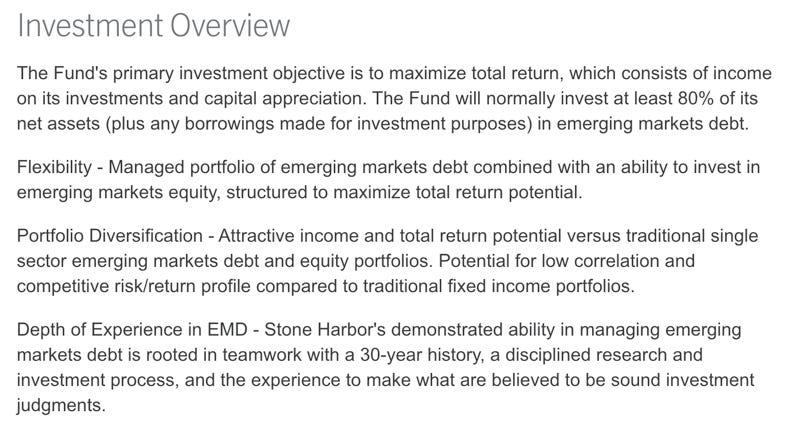

EDI’s investment objective is very straightforward. It aims to maximize total return, which consists of income and capital appreciation on its investments in emerging markets securities. It seeks to achieve its investment objective by investing primarily in emerging markets debt. It also utilizes leverage in order to enhance yield and total return potential.

EDI’s 70/30 split between government and corporate debt is a reasonable asset mix for this portfolio, but the risks really get ratcheted up from there. As we’ll break down in a moment, this fund tilts much more heavily towards areas that typically aren’t targeted as much in broader EM debt funds and it delves much further into lower quality bonds. Those factors alone make it much riskier than the typical emerging markets bond fund, but the near-20% use of leverage magnifies it even further. The high yield of EDI is clearly the big draw for investors, but this volatile fund should probably only be considered for small pieces of your portfolio.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.