Is Japan’s Fiscal Situation Not As Bad As It Seems?

Is Japan’s Fiscal Situation Not As Bad As It Seems?

All Sides Of The Argument

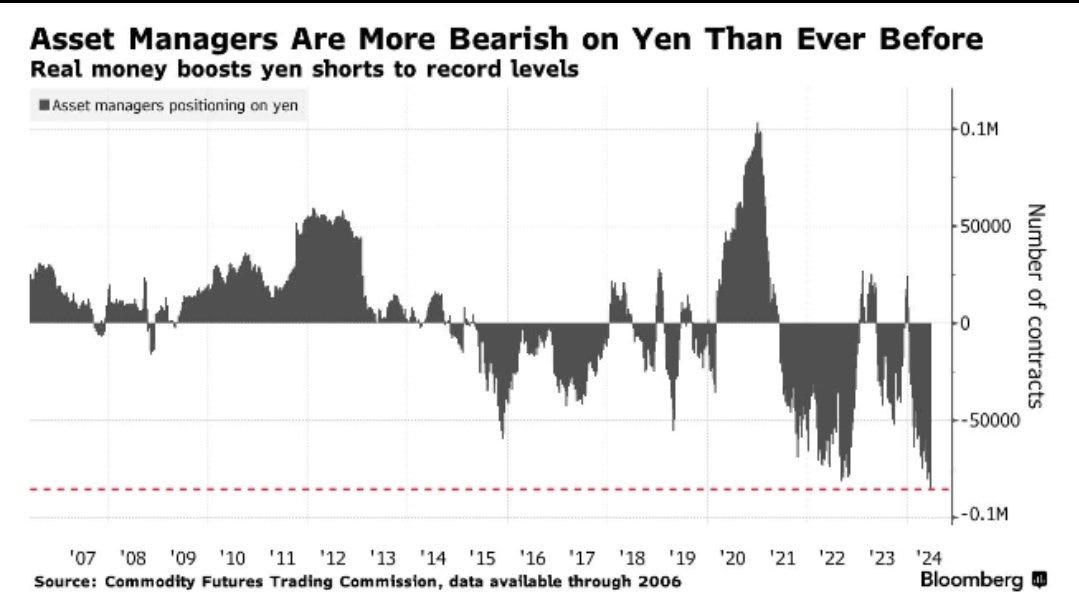

By now you’re probably very familiar with my thesis that the reverse yen carry trade presents one of the biggest tail risk threats to the markets today. For years, traders have borrowed ultra-cheap yen in order to invest the proceeds in higher returning assets, but now the short yen positioning is getting excessive. Right at the point where the BoJ may be forced into raising interest rates.

While I believe this is still the case, I received a message from a follower who wanted to take the other side of this argument (very politely, thankfully). He suggested that the situation might not be as dire as is being portrayed in the media and the true Japanese debt scenario might not be all that different from what we’re seeing in other developed markets.

In the spirit of considering all sides to an argument, let’s take a look at each one of the points mentioned to see if its risk is as large as it seems.

Japan’s Net Debt

If you look at gross debt-to-GDP levels around the world, Japan is right near the top of the list with a ratio currently more than 250%.

This is the number that gets most often quoted in the financial media and, while it’s accurate, the reader says that the net debt situation isn’t nearly so bad. And he might be right.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.