Is The Fed Satisfied With Inflation At 4% Right Now?

Is The Fed Satisfied With Inflation At 4% Right Now?

Spoiler Alert: Nah

If you take a read through the minutes from the June FOMC meeting, there appears to be a lot of debate surrounding whether the central bank should pause on tightening conditions or continue raising interest rates to fight inflation. You could easily make a case either way given the discrepancy between the stories that certain economic numbers and narratives are telling.

The “pause” camp could argue that the manufacturing sector is already contracting, the commercial real estate sector looks like it’s in big trouble if recent events are true and the inflation number itself is one of the economy’s most lagging indicators. The “hike” camp would say that GDP in the United States is still growing at a 3% annualized clip and the labor market is still incredibly tight.

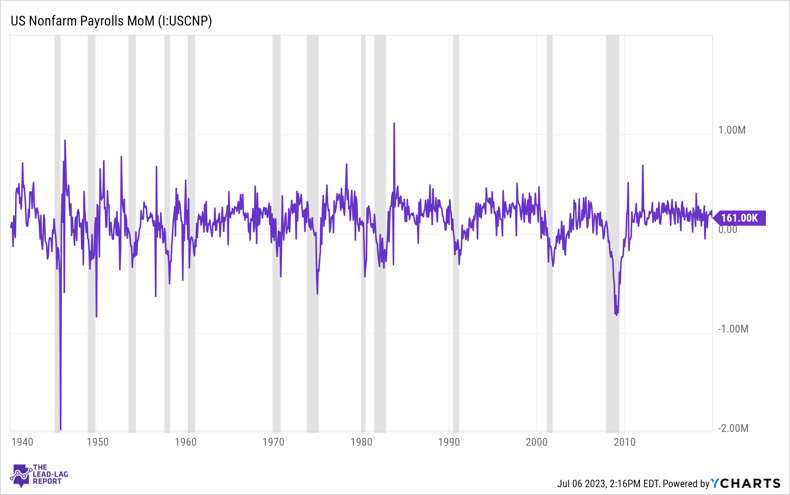

That latter point was evidenced this past week in the ADP employment report, which showed a gain of nearly 500,000 new jobs in June, the highest reading since early 2022. If we look back at non-farm payroll data over the past 80+ years, it’s consistently shown that slowing or negative job growth precedes virtually every recession. As of right now, we just haven’t seen that.

That begs the questions: what is the Fed’s feeling on the current inflation rate and how far does it feel comfortable pushing rates higher in order to tame inflation without risking recession?

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.