Is the Peak Near? How Germany's Economic Sentiment Echoes European Trends

Is the Peak Near? How Germany's Economic Sentiment Echoes European Trends

Unveiling Europe's Economic Peak

The debt ceiling fight in Congress remains the biggest tail risk facing the financial markets and there appears to be no progress getting made. So far, neither the bond nor the stock market has shown any reaction to the potential risks. That, unfortunately, less of an urgency for Congress to move now if there’s no direct consequence to the markets. Complicating the matter now is the growing belief that June 1st may not be the actual deadline. Some estimates say that the government may be able to hold out until as late as August before there’s actually a default. In 2011, the financial markets started to really react to the debt ceiling about 1-2 weeks before the deadline. Conditions look likely that we could see a repeat this time around (which means we would see volatility pick up any day now if it were to happen). If there’s uncertainty around when the government might actually default, the financial market reaction to it might get kicked down the road as well.

Gold, however, has been moving higher pretty steadily since March, but really all the way back to November. It’s followed a pretty clear risk-off narrative too. Prices declined at the beginning of February when several economic reports, including GDP and retail sales, came in stronger than expected, but shot higher again when Silicon Valley Bank failed. Since then gold prices have remained firm, supporting the idea that investors are genuinely taking a cautious approach here. Earlier this month, gold touched a new high on what feels like a response to the debt ceiling drama. It feels like the combination of this, high inflation and the build towards recession is likely to keep gold looking relatively strong at least until the point where the debt ceiling finally gets resolved.

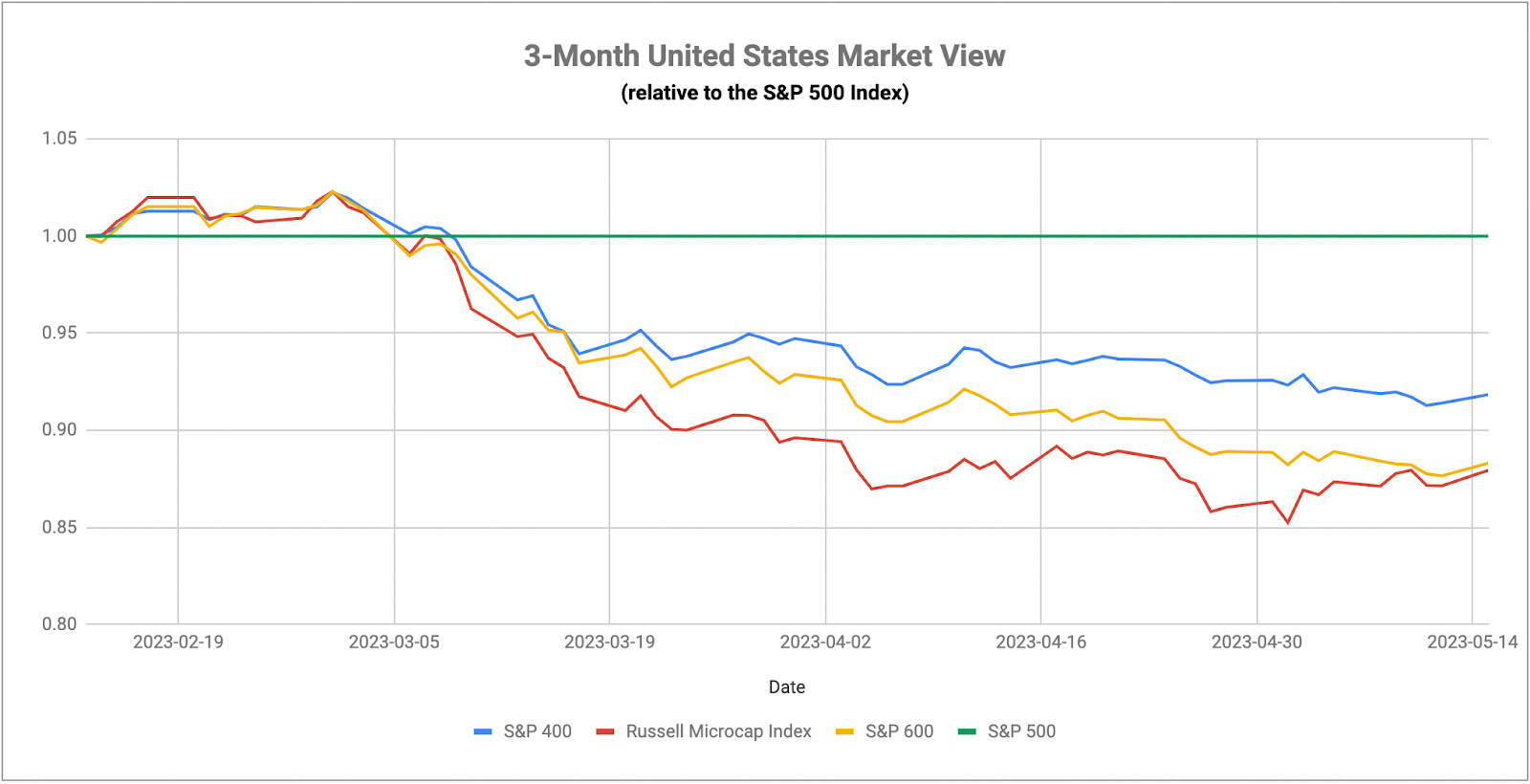

This is turning out to be a week heavy with new economic data and most of it isn’t encouraging. Prior to the April reading, U.S. retail sales were negative in four of the past five months. Last month, they were up 0.4%, but that was well below estimates of 0.8% growth month-over-month. The warning bells for consumer behavior keep getting louder and, since that’s what fuels the economic engine, shouldn’t be ignored despite positive GDP growth and a tight labor market. Home Depot just this week delivered disappointing quarterly results and, like other retailers, signaled that consumer spending is getting weaker. Especially worth noting is that HD’s management team said that lumber deflation caused nearly half of the company’s 4.5% sales decline in Q1. When I talk about lumber being a leading indicator of economic activity, this is exactly what I’m talking about and how it plays out in real life. Lumber prices have been crashing, which signifies slowing demand, which hurts the manufacturing sector & corporate earnings and ultimately sends stock prices lower. It’s very unlikely that Home Depot is the only company being impacted by this.

Overall, I think we’re really starting to see the effects now of the Fed’s rate hiking cycle. In general, there’s a 12 month lag from when the rate hike occurs to when it’s really felt in the economy. A year ago, the Fed Funds rate was 0.75%, which means we’re likely still in the very early innings of this. There’s still more than 400 basis points of rate hikes which have yet to be really baked into the cake. If we’re seeing manufacturing already significantly slowing, major retailers warning about slowing consumer demand and banks failing, imagine what still might be ahead for the U.S. economy.

If Germany is an indicator of broad European economic sentiment, it looks like the top is in.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.