It’s Here

If there’s one thing that’s consistently shaken investors’ confidence over the past two years, it’s been higher than expected inflation readings. People have spent so much time trying to talk themselves into the idea that a disinflationary trend is in place and/or the Fed is going to come to their imminent rescue that they have trouble handling any evidence to the contrary.

We saw that again this past week when CPI again came in hotter than expected and the market turned south. Both stocks and bonds got slammed, but anything interest rate sensitive got hit particularly hard, including utilities, real estate, high beta stocks and small-caps. Long-term Treasury yields shot higher in anticipation of the Fed delaying any planned rate cutting cycle. That, in turn, helped send the dollar higher.

Inflation, however, is only one piece of a very large puzzle here. It’s the most visible because, well, it gets all of the media attention, but it’s far from the only consequential left tail risk that’s out there right now. In fact, I’d argue that it’s not even the biggest risk factor facing investors right now.

When you take all of these factors into account collectively, it leads me to believe that this might actually be one of the riskiest markets we’ve faced since the COVID recession in 2020. It’s one that could react sharply, decisively and swiftly with little warning should conditions come together in just the wrong way.

I’ve talked about preparing for the credit event for a while. I think it might finally be getting close.

Let’s run down the evidence piece by piece.

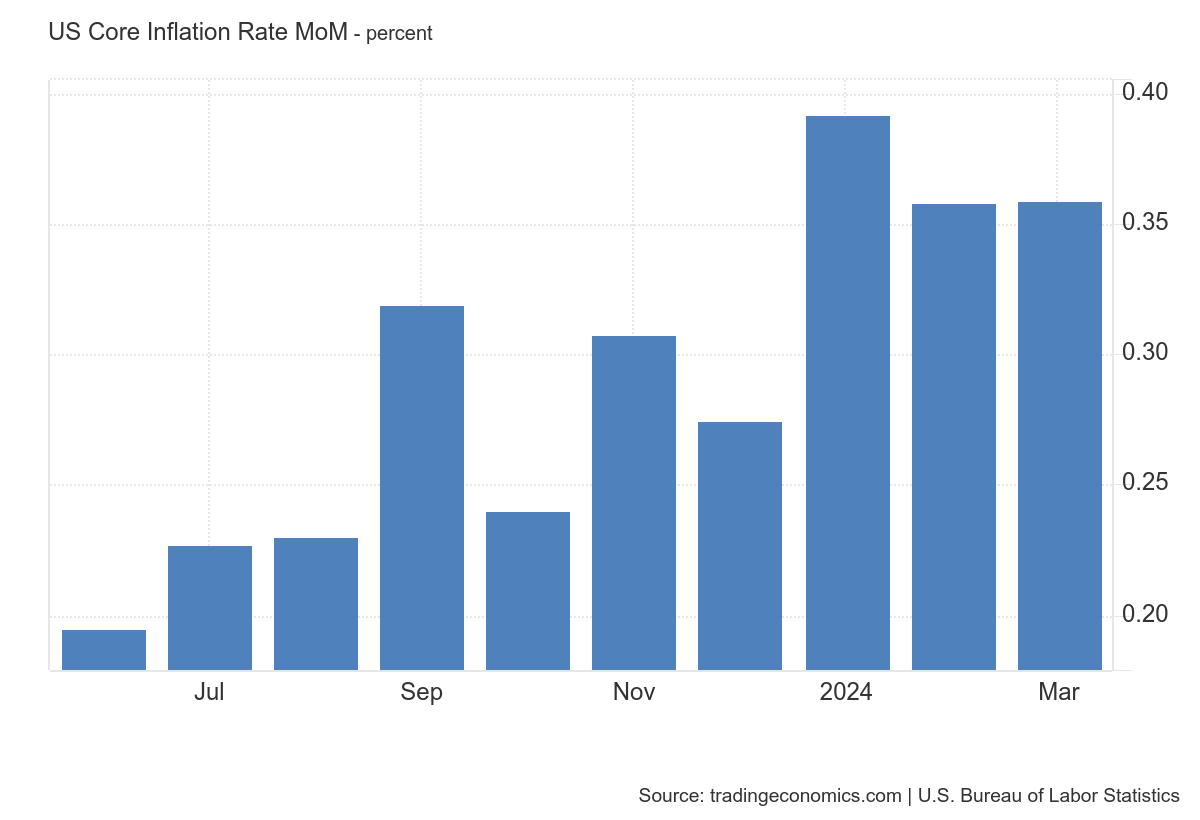

Inflation Is Re-Accelerating

Take a look at the graphic below. This is for U.S. core inflation on a month-over-month basis going back to last summer.

Does this look like a disinflationary trend to you? This is particularly troublesome because it’s the stickier kind of inflation that can have trouble easily getting back down to target. Over the past 12 months, the core inflation rate is 3.8%. On a 3-month annualized basis, core inflation is at 4.5%. If you take away the Fed’s dot plot report and you take away the preferences of those in Washington, there is no reasonable case to be made for why the Fed should be considering rate cuts here with core inflation trending at 4-5%.

The problem is that investors just can’t quit their hope for rate cuts. The futures market still has 1-2 rate cuts priced in and the junk bond market is priced for perfection as it relates to high yield spreads. If Powell walks up to the podium at some time in the next few months and says he just can’t imagine cutting rates until inflation gets back under control again, I don’t think the markets will take it well at all.

Lumber/Gold Is Screaming Risk-Off

You may already be aware that gold prices have been rising steadily and sharply over the past 2-3 weeks. What you may not be aware of is the fact that the rally in gold has been mirrored by a virtually identical move down in lumber prices.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.