Junk Bonds Become The Primary Driver Of The Bond Market

Junk Bonds Become The Primary Driver Of The Bond Market

This Should Scare You

While the events in Israel, the dysfunction in the U.S. House of Representatives and rising Treasury yields dominate the headlines for the time being, let’s not forget the fact that a potentially major credit event still looms. The conditions that would support such a tail event occurring are still very much in place. In spite of the fact that the “stronger for longer” market narrative and persistently tight labor market are pushing away short-term concerns about recession, we’re actually getting MORE evidence that credit event risk is increasing.

For example, there was this post on X/Twitter.

The fact that there’s more junk-rated debt out there today than AAA-rated debt seems a little concerning. The big catalyst, of course, is Fitch’s downgrade of U.S. government debt from AAA to AA+, but that shouldn’t underscore the larger trend in the bond market. Years of debt accumulation at ultra-low interest rates have swollen the number of zombie companies out there to unsustainable levels, companies that likely would have had trouble surviving under a normal rate environment. Now we’re likely entering an era of prolonged higher interest rates that is going to drive a lot of these names into bankruptcy.

And it might happen sooner rather than later.

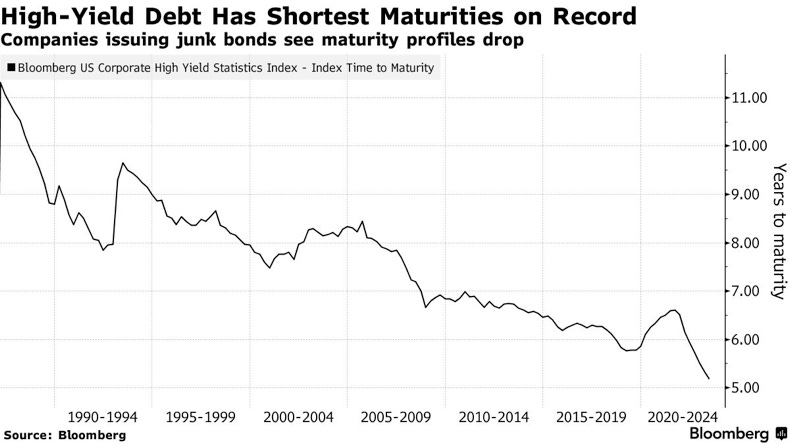

As interest rates have soared, the term to maturity has shrunk. Three decades ago, junk bonds averaged 9 years until maturity. Today, that number is approaching just 5 years. I’ve mentioned repeatedly the risks that are coming from this mountain of debt maturing and needing to be refinanced at much higher rates. This, in fact, is probably going to be one of the biggest factors that ushers in a major credit event. As maturities drop, the fuse to that ticking time bomb gets shorter.

I dove into these Bloomberg articles a little more and found these nuggets, which should put an additional scare into just about anybody.

Cool! If you do the math, the current risk-free rate of 3-month Treasury bills is about 5.4%. The current spread on B-rated corporate debt is about 4.4%. Add those two numbers together and you get 9.8%, roughly the 10% benchmark mentioned above (it’s a very crude, back of the envelope calculation, but it should be directionally correct). We could deduce from this that nearly ⅓ of all outstanding junk debt is rated single-B or worse, which is not even close to the qualification for investment-grade. As economic conditions worsen and debt gets refinanced, we’re facing an environment where tens, if not hundreds, of billions of bonds risk falling into default.

In fact, it looks like we’re already headed well down that path.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.