Short-Term Versus Long-Term

Short-Term Versus Long-Term

A Pre-Emptive Strike

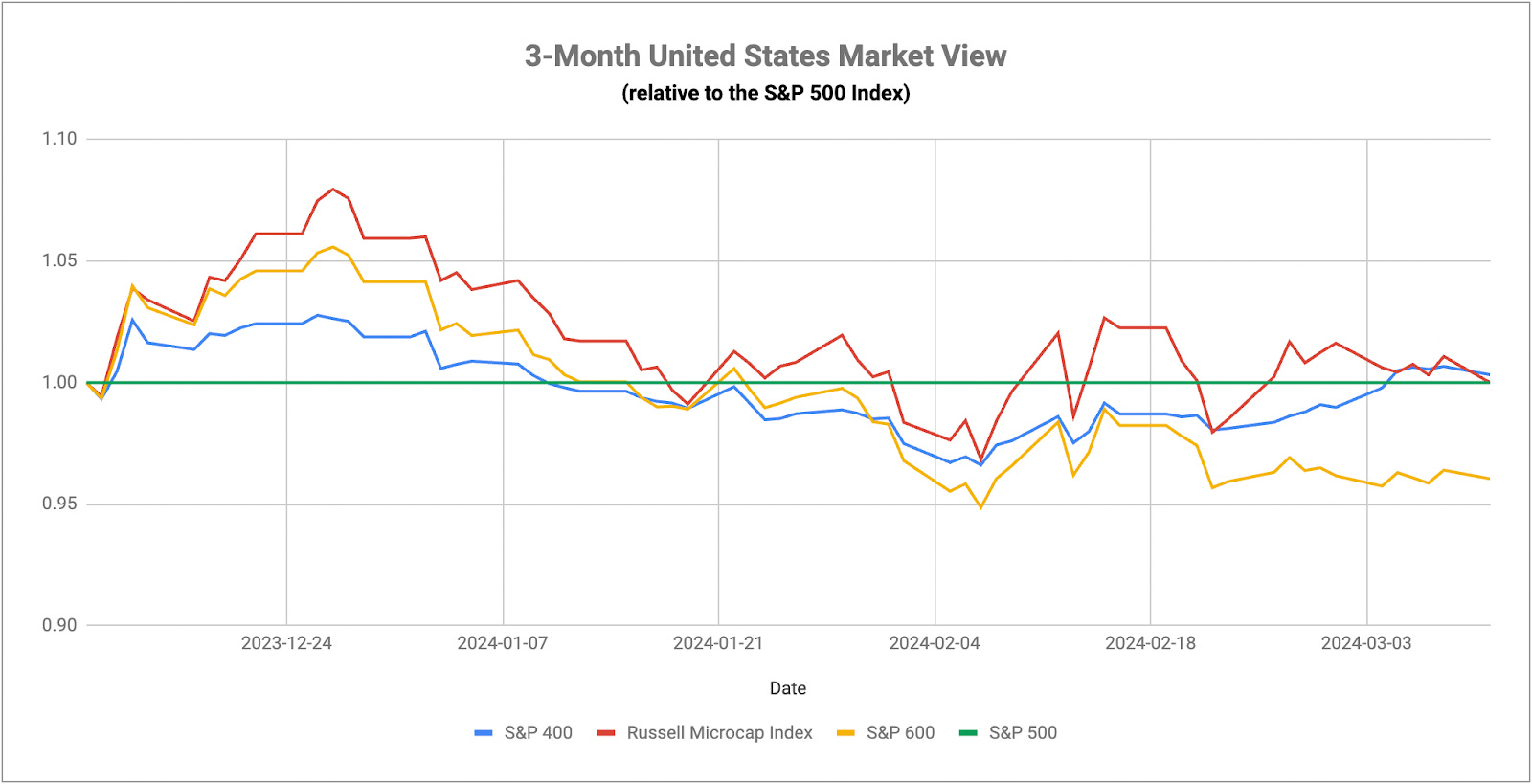

With the rallies in gold, Treasuries and utilities entering their third week, sustainability becomes the key thing to watch. A digestion of recent gains would be considered fairly normal at this point, but I wanted to see if these assets were at least able to hold on to those gains. So far, they’ve done OK. Monday was a continuation of the trend, but Tuesday’s inflation report was taken as a confirmation that rate cuts are still coming, which boosted large-caps and tech again. Overall, I think the trend towards defense is still intact. At this point, I think any development that is supportive of the rate cut narrative, whether that’s dovish rhetoric from the Fed itself or some new data point, is probably going to pop growth and tech stocks, but sentiment absent any of those catalysts seems to be trending defensive. The risk signals tend to get it right much more often than not (even if the expression of that signal doesn’t always work out). They’re signaling that a shift is happening as we speak, so I’m not writing off the possibility of a further extension in defensive strength.

Speaking of inflation, this week’s February CPI report didn’t tell us a whole lot that we didn’t already know. The headline rate ticked up slightly to 3.2%, while the core rate dipped to 3.8%. Both, however, came in above expectations. The larger takeaway, in my opinion, is that inflation could be in the process of becoming a much bigger issue again. Core inflation rose by 0.4% for the second straight month, which puts its 3-month annualized rate at around 4.3%. That’s typically not where you’d start cutting rates, but it appears that’s what’s going to happen just a few months from now. It raises questions about what the Fed may or may not know and what they’re ultimate goal is. If it’s not inflation control, then what? Perhaps they’re worried about the labor market? The unemployment rate in February hit 3.9%, up from a low of 3.4% in April 2023. Most investors are focused strictly on the jobs added number, but an increase of 0.5% in the unemployment rate over a relatively short period of time generally indicates a shift happening in the labor market. Granted, it’s beginning from such a low starting point that maybe it’s not a red flag just yet, but this increase should not be ignored. Maybe we should give the Fed some credit for a potential pre-emptive strike against labor market weakness, something they should have done with regards to inflation in 2021.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.