Soaring High

Soaring High

Unraveling the Dollar Index's Surprising Rebound & the Forces Behind It

The S&P 7 has been lifting the broader market averages throughout 2023, but the AI mania spurred on by NVIDIA’s Q1 earnings report is only a week old. That leaves open the possibility that we’re still in the early innings of another tech bubble that ignores all rhyme and reason. NVIDIA now trades at more than 200 times earnings and even the tech sector as a whole is back up to a forward P/E of 27. Regardless, investors seem to be back on board the tech train and are willing to ride it until the end of the line when they’re literally thrown off. Rallies, such as this one, that get way out over their skis have a good chance of ending very badly. That means there’s a lot of risk for FOMO investors, but opportunities for disciplined ones. Almost every non-tech sector of the market is lagging the S&P 500, but that could quickly reverse once this rally pushes too far.

While the mega-cap names pull the averages higher, there’s very much a case building that could see utilities and Treasuries quickly vault back into leadership. Investors aren’t terribly interested in fundamentals or valuations at the moment, but they were all throughout 2022 and into parts of 2023. The helped value, dividend, quality and low volatility stocks outperform the S&P 500 by a wide margin last year and even helped small-caps stay ahead of large-caps for much of the year. Right now, there’s a very real possibility that we see a repeat of 2011 where one of the major credit agencies issues a credit watch on U.S. government debt before officially downgrading it around the whole debt ceiling fight. We’ve already got the credit watch from Fitch and the downgrade may come soon if this comes right down to the final hour of the new June 5th deadline. If that happens, conditions would be ripe for a swift and sudden return to both utilities and Treasuries as part of what could be the beginning of the larger credit event that I’ve been talking about for months. The overdone rally in tech, growth and high beta could also end up playing into this as valuations and euphoria start to unwind.

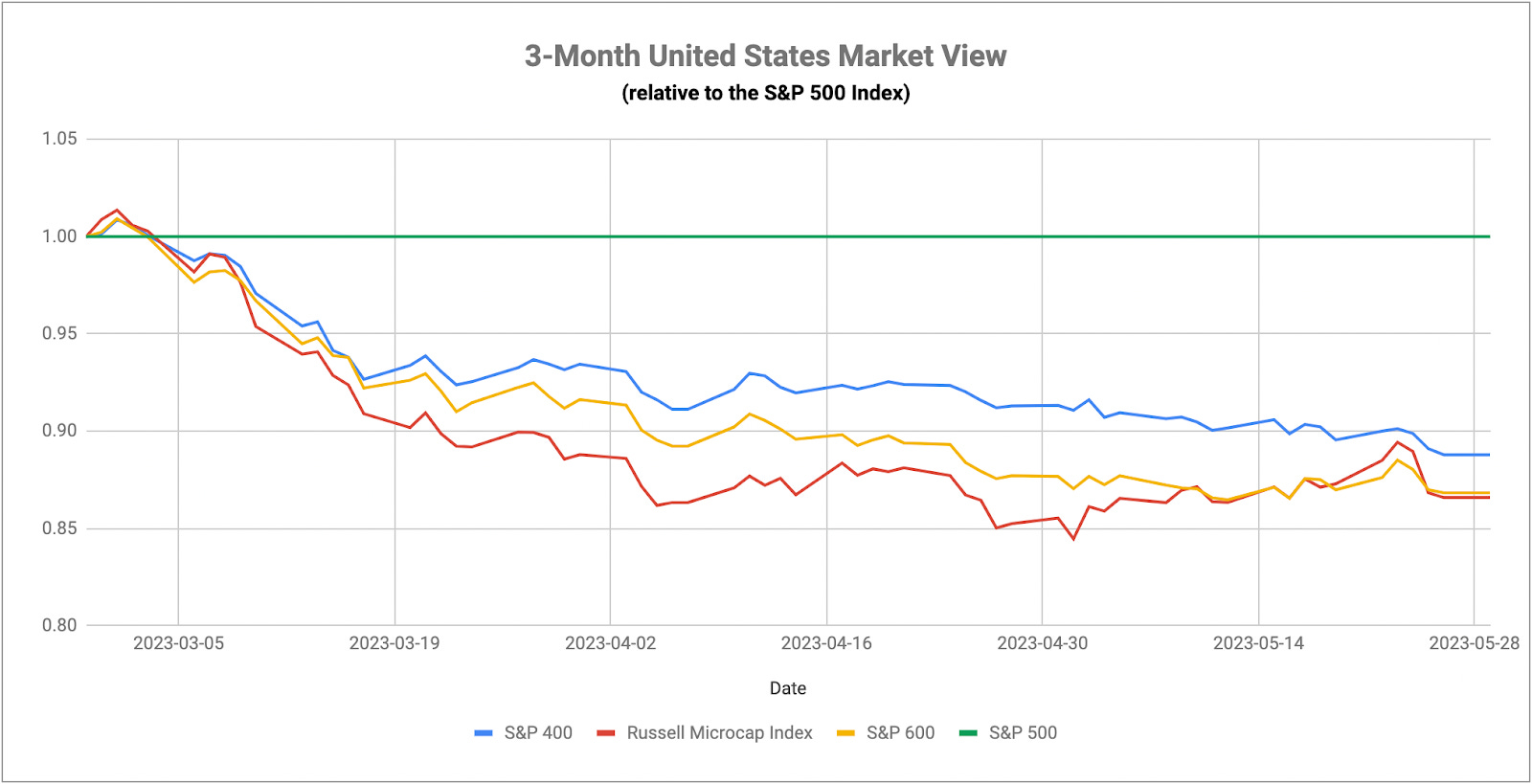

Either way, be very careful here. The equal-weight S&P 500 is flat on the year and trailing the traditional index by more than 10%. The gap on the equal-weight vs. cap-weighted S&P 100 is 12%. On the Nasdaq 100, it’s 15%. On tech stocks, it’s 17%. Since March, the Nasdaq Composite has consistently been setting more new 52-week lows than 52-week highs. It seems misguided to think that a new bull market is beginning here.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.