Staying Alive

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: THE TREASURY TRADE IS STILL ALIVE

Technology (XLK) – A Dangerous Trend

Last week marked the return of a trend we’ve seen all throughout 2023 - the domination of mega-cap growth and tech. While it makes the major market averages look good, it’s not a good sign for longer-term market strength. The FAAMG names remain the one corner of the market where investors seem comfortable coming back to, but it’s dangerous for such a narrow segment of the market to keep leading. Tech was the only sector to beat the S&P 500 last week.

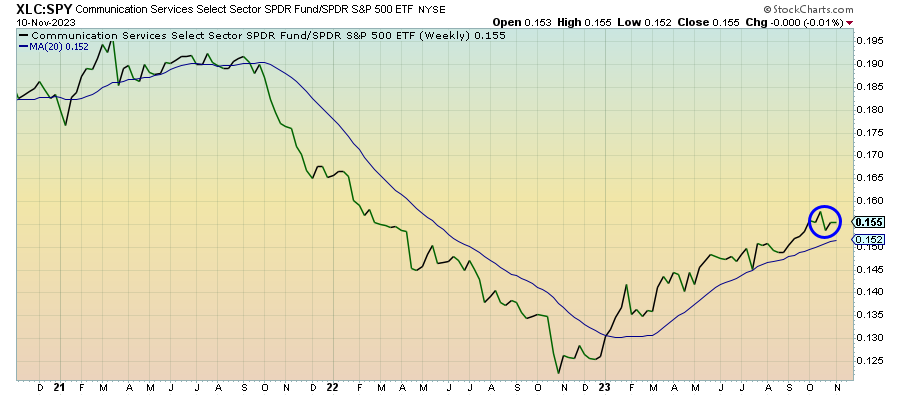

Communication Services (XLC) – FANG And Little Else

While tech has dominated the market landscape recently, this tech-adjacent sector looks like it’s finally begun to level off a bit. Traditional telecom names continue to be the anchor of this sector, but it’s struggled to get meaningful and consistent gains out of anywhere besides Facebook and Google. Last week was really just an extension of the trend where the FANG names lift the entire sector.

Long Bonds (VLGSX) – Treasury Trade Is Still On

After a promising start to last week, long bond yields got turned back at 4.5% and might need another catalyst to renew their push lower. Despite volatility, long-dated Treasuries are still posting gains here and shouldn’t be viewed as out of favor. The magnificent 7 rally may distract investors from bonds for now, but smart investors know that market breadth is awful right now and the Treasury trade is still on.

Treasury Inflation Protected Securities (SPIP) – Expectations Remain Steady

The October CPI data we’ll get later this week will very likely suggest that inflation is still moderating, but nowhere near the Fed’s target 2% rate. The market seems to have long since priced in a longer-term inflation rate of ~3% through the end of 2024, so there’s no huge demand for inflation protection at the moment. I suspect that’ll continue for the near-term barring some type of major economic developments.

Junk Debt (JNK) – Negative Long-Term Conditions Still Remain

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.