Tech Rally Showdown

Tech Rally Showdown

Is it Peaking or Simply Taking a Breather?

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: IS THE TECH RALLY PEAKING OR JUST PAUSING?

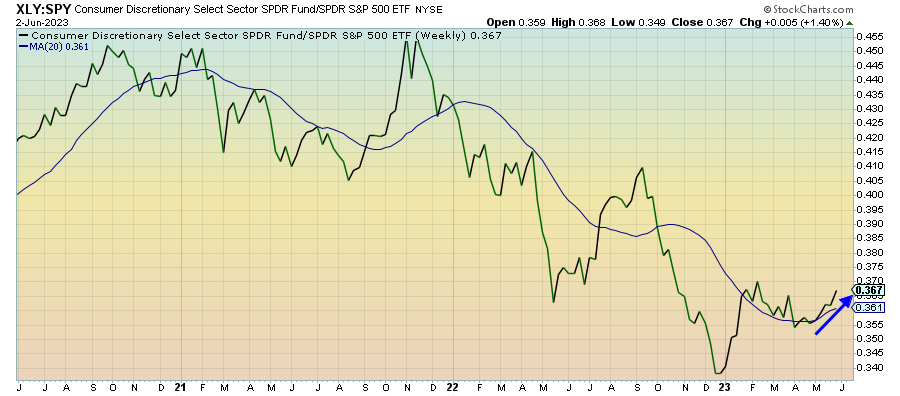

Consumer Discretionary (XLY) – Jobs Boost

Discretionary stocks continue to push higher and demonstrate that growth stocks are still in charge. Last week’s strong jobs report will no doubt help investors that if consumers’ employment situation is secure, they’ll be more comfortable spending. I’m still concerned about so many retailers issuing warnings about consumer behavior (Macy’s and Costco are the latest), but the high level data still looks reasonable.

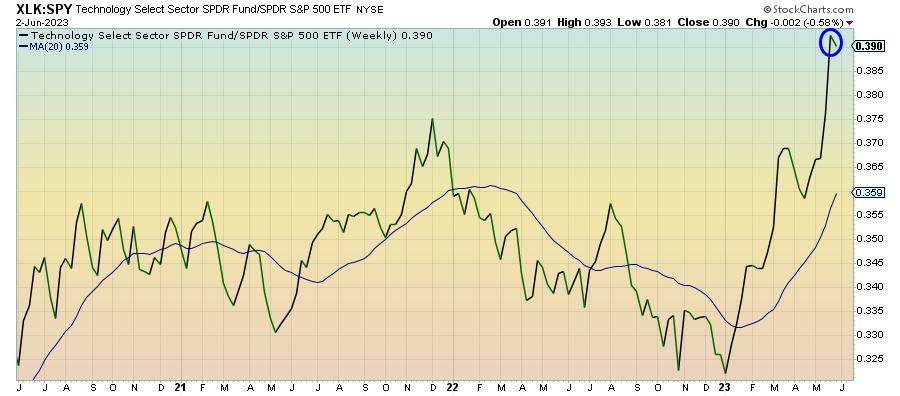

Technology (XLK) – Peak Or Pause?

The tech trade finally takes a bit of a breather, but is this a peak or a pause? Given that the gains in the major market averages, especially the Nasdaq 100, are being driven by just 7 stocks, there’s a potentially very serious consequence to investors if this trade breaks down. The equal weight S&P 500 is flat on the year, so there’s not a lot of strength out there that can pick this market up if the FAAMG trade begins to fail.

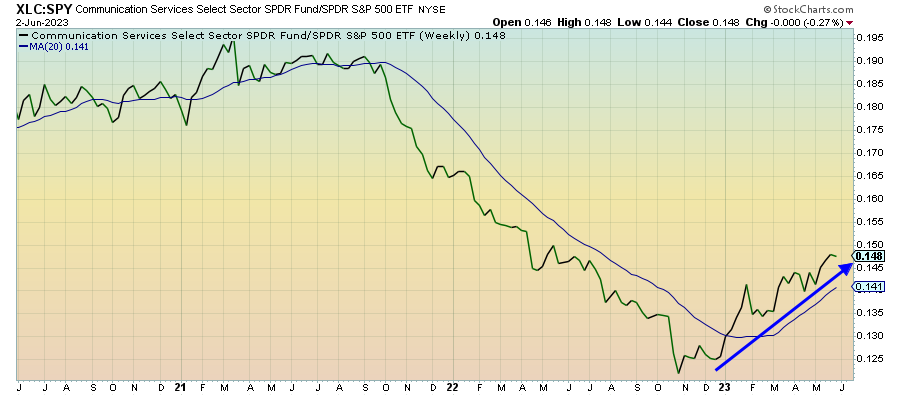

Communication Services (XLC) – Extreme Idiosyncratic Risk

Communication services continues moving higher in lock step with the tech sector. The same things we’ve said about tech can pretty much apply here as well - Facebook and Alphabet are almost entirely driving this sector’s gains and remain vulnerable to a pullback. Even though investors are no doubt happy with 2023’s performance, the idea of having just two stocks accounting for more than half of the sector puts it at extreme idiosyncratic risk.

Treasury Inflation Protected Securities (SPIP) – Balanced Expectations

The TIPS market is still indicating that investors are pretty neutral when it comes to inflation expectations. The hot jobs report will probably cement the notion of “higher for longer” for at least a little while more and could put some pressure on rates to remain elevated. Still, there’s no real drive to add protection in the way there was leading up to the start of the Fed rate hiking cycle. Expectations appear to be fairly balanced.

Junk Debt (JNK) – No Flight To Safety…..Yet

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.