The Big Question Of The Week

The Big Question Of The Week

Few?

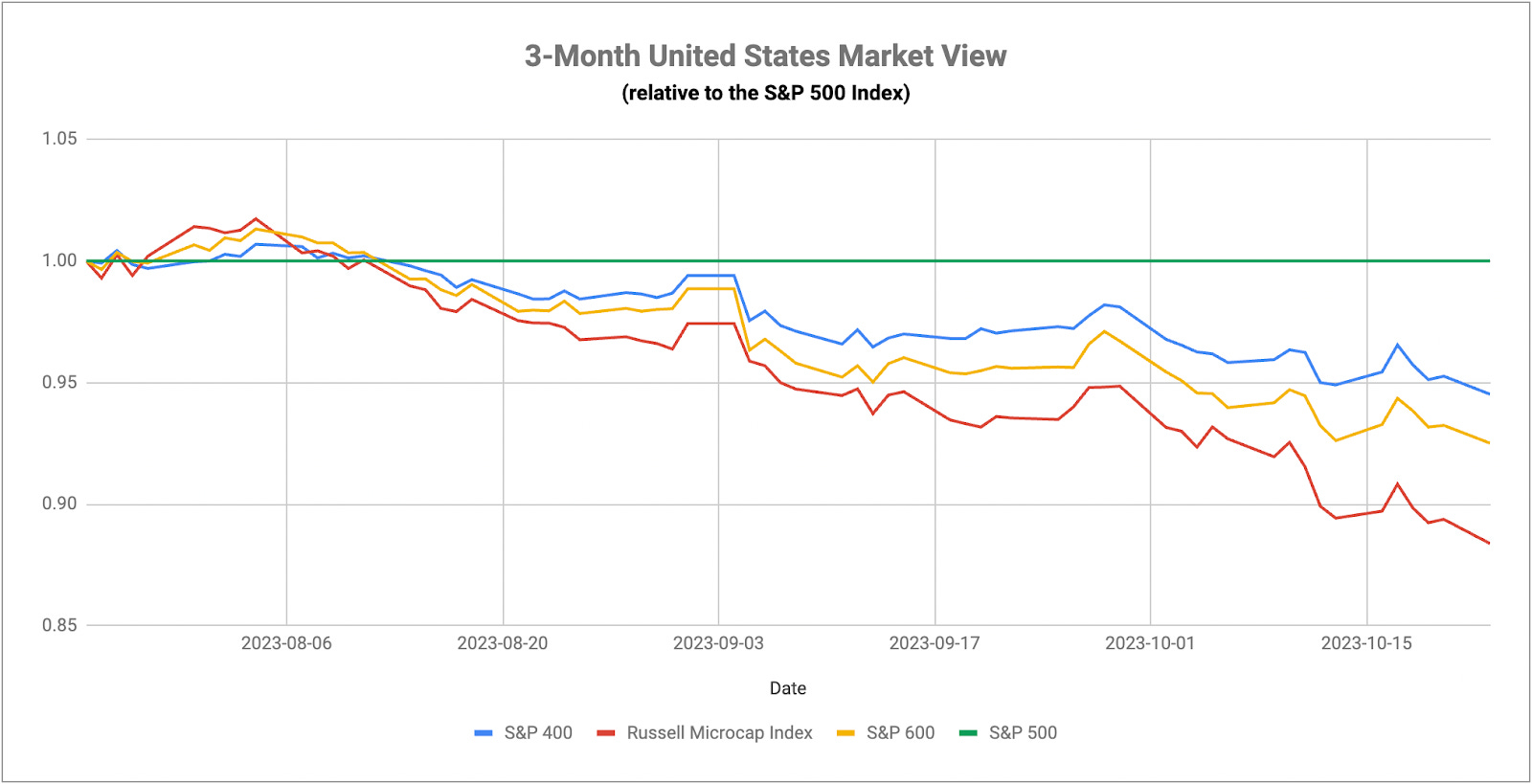

The return of the flight to safety trade continues to develop this week that even a better-than-expected U.S. PMI reading and solid tech earnings have been able to slow down. Over the past two and a half weeks, we’ve seen gold gain 8%, utilities lead the broader market by 5% and small-caps by 7%. The larger development may be that long-term Treasuries have gained nearly 3% during the first two days of this week alone, while the S&P 500 is down. It’s this negative correlation between stocks and bonds that needs to return in order to confirm that the risk-off trade has fully arrived. High yield spreads are starting to widen again. The 10Y/2Y Treasury yield spread is within range of un-inverting in the near future. The S&P 500 just crossed below its 200-day moving average for the first time since March. There are simply too many warning signs flashing red right now to ignore. The financial media wants to talk about this being the 1-year anniversary of the new bull market. In reality, the S&P 500 only got to within about 4% of its previous all-time high before correcting in the past few months. It’s looking more and more likely that we just experienced one of the biggest bear market rallies, not a new bull market.

The 10-year Treasury yield topped out earlier this week almost exactly at the 5% level before retreating back to 4.83%. I think 5% is a very psychologically important level because it represents the nice round number that triggers people to rethink their positions. For Bill Gross and Bill Ackman, it meant closing out short positions in bonds believing that they’ve peaked. Perhaps that motivated other investors to consider long positions again, but it seems pretty clear that there’s some built-up pressure here that could spark a rally. People will point out the current relative lack of demand for Treasury debt given the negative fiscal outlook, but money has been flowing into Treasury funds, long-term and short-term, for most of 2023. If the upcoming Treasury auctions show there’s still reasonable demand for government securities, we could be setting up for a short-term rip.

The participation of bitcoin in this risk-off move is really interesting. Investors have traditionally treated crypto as an aggressive growth stock in the past, but the fact that both gold and bitcoin are moving strongly higher here suggests that investors may be hedging counterparty exposure here. By that, I mean that they’re worried about corporate bankruptcies, debt default and even U.S. government shutdowns and debt loads. They’re looking for assets that aren’t necessarily exposed to the risk of something going sideways. Gold is simply a hard asset that can be held in your hands, while crypto is a decentralized asset separated from the global financial system. Bitcoin, in particular, is especially volatile, so it’s tougher to discern consistent trends, but there is a bit of a history of gold and bitcoin correlating positively during periods of market stress - the Silicon Valley Bank collapse in March being the most recent example. The possibility of a bitcoin ETF approval by January is probably influencing prices to some degree, but I think there’s a story being told here.

With regard to gold and oil, it looks like both prices are being heavily directed by events in the Middle East. Escalating tensions tend to lift both assets and vice versa. It’s hard to determine what information is real and what isn’t at this point, but there are suggestions that Iran is about to get more involved, which means the United States is likely to get more involved. If that happens, it’s reasonable to believe that safe haven assets - gold, the dollar, maybe Treasuries - all catch a bid since geopolitical tensions are almost always risk-off catalysts. Gold, especially, has been in the background for much of 2023, drowned out by the tech and AI rallies, but I think it’s about to become much more involved in the discussion.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.