The Biggest Developments Internationally

The Biggest Developments Internationally

What's Going On With China?

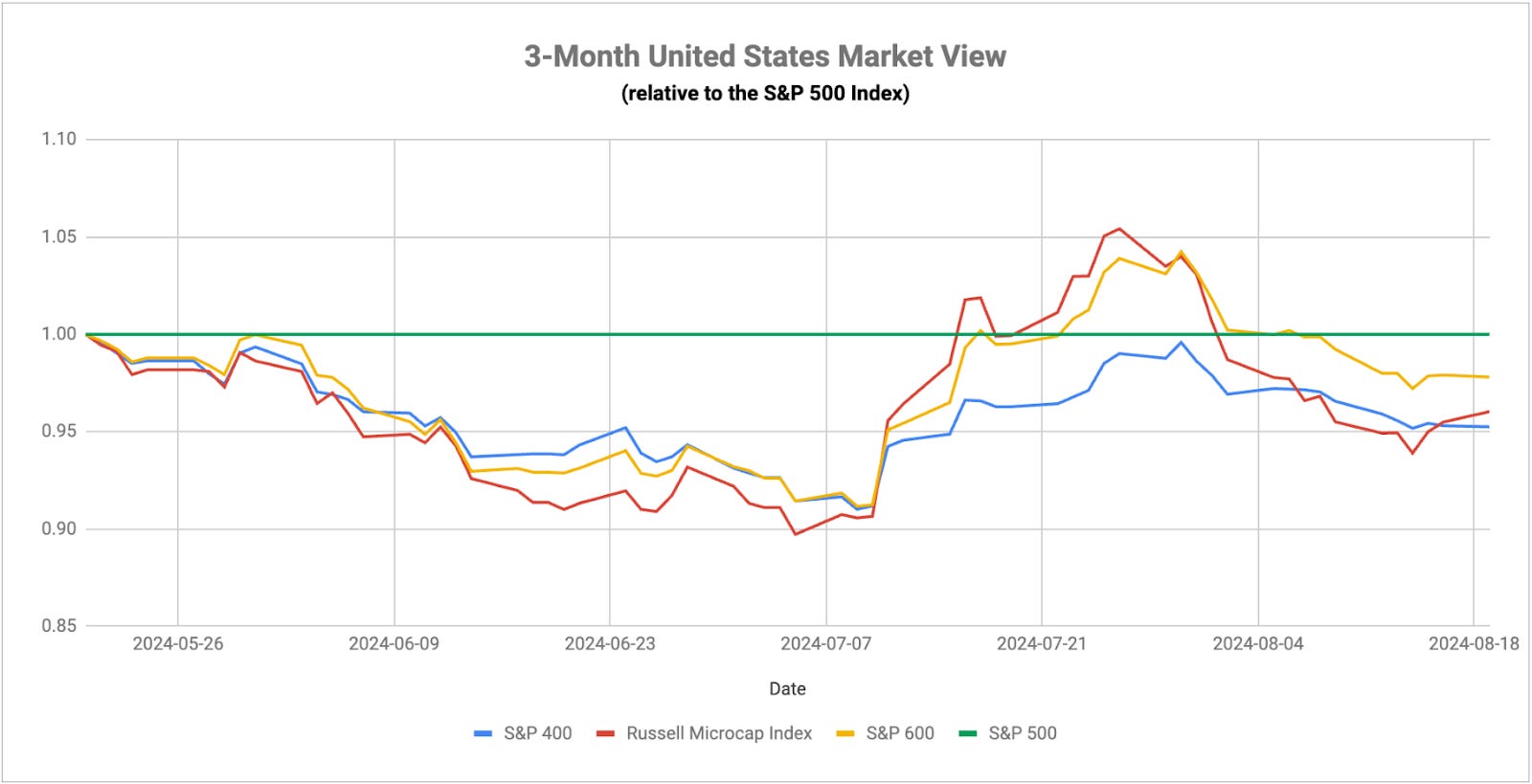

Market sentiment is pretty much back to where it was pre-VIX spike, which is to say that we’re back to an environment dominated by mega-cap tech. There are a couple of differences this time around though. The magnificent 7 stocks aren’t dominating in quite the same way that they were just prior to the reverse yen carry trade unwind. Communication services stocks are not really participating this time around either as it continues to disconnect from tech. Discretionary stocks are still mostly lagging, demonstrating that not all growth areas of the market are doing quite so well. If we also consider that credit spreads are still elevated compared to where they were a month ago, there’s a bit less confidence being signaled in the markets right now. Three of my signals are still risk-off, while gold and Treasury prices are still trending higher. This is all pretty consistent with my stance that investors are being sucked in by another bear market bounce. We already know that there are a number of economic signals indicating caution, but the fact that a number of financial market signals are confirming the same suggests that this market rebound isn’t as strong as it might seem.

At the core, I believe, is still the housing market. For as much as people want to talk about how this is the new AI economy, the correlation between the housing market and the broader economy is well-established. There are a few factors here that I find quite concerning. Much of the housing market has seized up over the past 12 months as the affordability gap has failed to bridge buyers and sellers. We may be finally seeing it thaw in a way that brings price discovery back to the market. Existing home sales are way down. Housing starts are way down. Building permits are way down. There simply isn’t the demand for home construction that there was in the past and I think we’re seeing that in lumber prices. The one factor that’s changing, however, is available housing inventory. That’s starting to move higher again and has climbed to 2022 levels. If supply starts to normalize, I’m guessing that we’re going to see home prices start moving lower due to the laws of supply & demand if nothing else. If people start feeling that they’re homes are becoming worth less and feeling less wealthy, in general, it could have all sorts of negative cascading effects.

U.S. inflation rose by 0.2% in July, landing right at expectations and clearing the way for the Fed to cut rates in September. The markets are pricing in a 100% chance of a cut at that meeting, the only question is whether it’ll be 25 or 50 basis points. There’s a clear argument to be made for both. A 50 basis point cut allows the Fed to catch up from what probably should have been a quarter-point move in July. That at least gets them back on schedule and then they can proceed with gentler quarter-point cuts from there based on conditions. Powell may opt for a quarter-point here though due to core and shelter inflation, which are still too high. Core is just above 3% and rent inflation is north of 5%. Given the significant impact of shelter inflation, I don’t think the Fed wants to risk sending that higher again, but if the housing market scenario I laid out above plays out, that number could come down quickly.

We’ll hear a lot about this at Jackson Hole this week, most notably from Powell at the end of the week. The more interesting speech could come from Governor Ueda of the Bank of Japan. Their policy path is likely being watched even more closely than that of the Fed. He’s got quite a balancing act to pull off and he may provide some hints this week.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.