The Clock Is Ticking

The Clock Is Ticking

And It’s Made In Japan

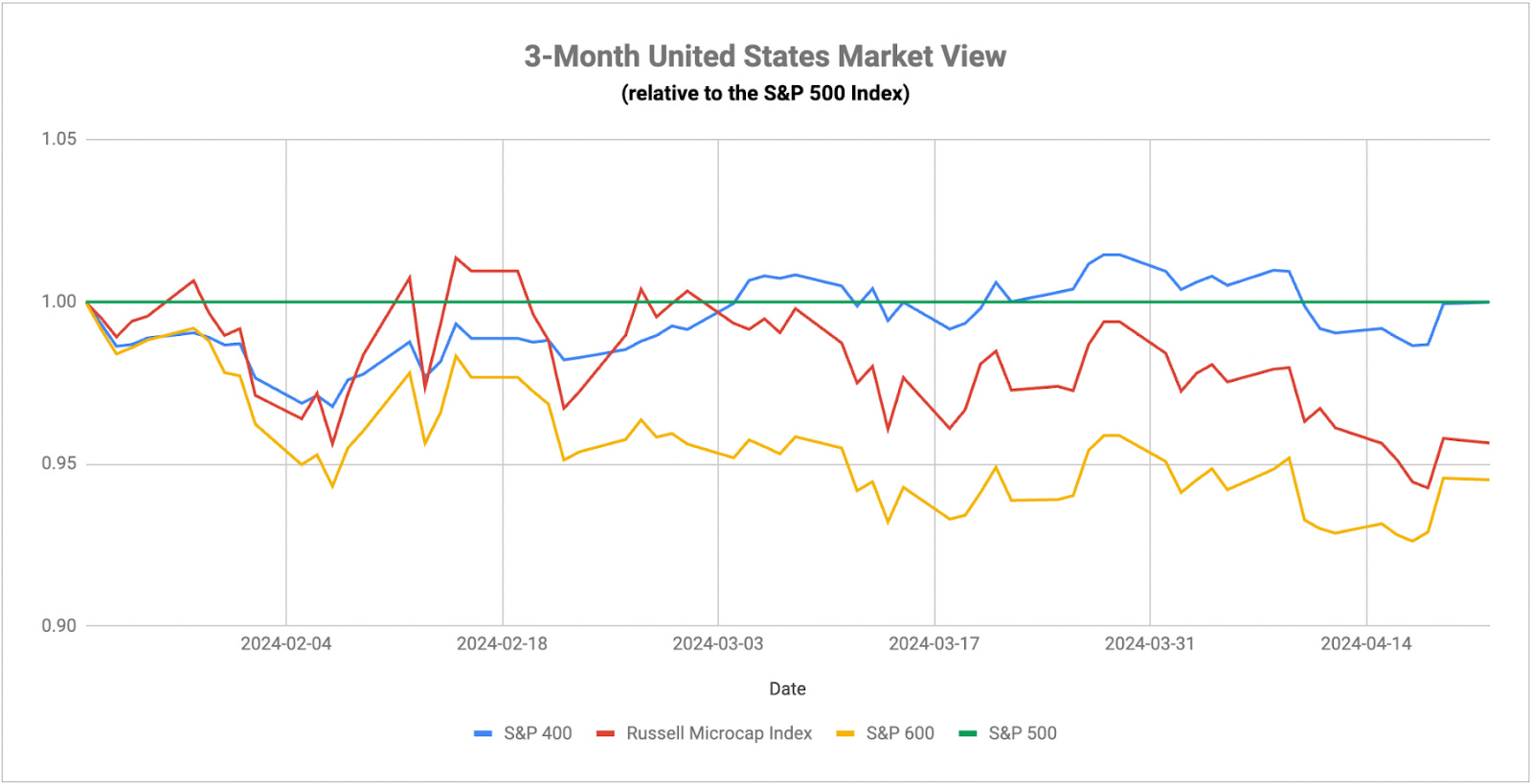

While I noted earlier this week that I believe we could be early in the cycle favoring utilities, I think we’re looking at a fairly specific timeline where the sector could be signaling a volatility spike. Yesterday’s leaders/laggards piece showed that utilities have been outperforming the S&P 500 since February, but the trajectory has really accelerated in just the past few weeks. Historically, sharp outperformance like we’ve seen produces about a 3-4 week window following the signal where conditions really favor a volatility spike. And I think that signal is still holding this week. Most investors will look at the S&P 500 and see a 2% rebound and think that the bottom is in and a reversal has begun. In reality, utilities are still holding here. They’re only underperforming by a negligible amount. That indicates to me that this risk-off trend we’ve seen over the past several weeks is still in place, which means that volatility watch is still on.

All of the major pieces are already in place and we could even see this volatility spike yet this week. Coming up in the next few days is PCE inflation data (which will likely be confirming the reinflationary trend), the first read on Q1 GDP (which could signal a slowdown, although growth is probably still at healthy levels) and big tech earnings (Netflix has already taken a hit, Apple looks vulnerable and who knows about Alphabet/Facebook). If any of those show weakness, it could pull the bears back off the sidelines and see them liquidating risk asset positions further. The latest economic data has been fairly supportive of the resilient economy narrative so perhaps it’s less than likely that we get any kind of significant disappointment here, but things are definitely setting up where it could happen.

Lumber/gold is also looking really ugly here and that’s another reason why the market is vulnerable to a volatility spike here. We’ve been talking about the gold rally a lot over the past several weeks, but the drawdown in lumber prices is just as significant. Commodities are rallying almost across the board, yet lumber is the one holdout that’s moving lower. Why is that? Is it the unwinding of expectations that the Fed will deliver multiple rate cuts leaving home building costs higher for the foreseeable future? Is it the lack of demand for housing with buyers continually getting priced out? Is it just the general belief that the U.S. economy is trending in the wrong direction? It’s probably a combination of all these, but the fact that it’s happening as gold is taking off is especially concerning. I know people will argue that retail investors aren’t really getting involved in the gold buying here and all the demand is coming from Asia, but I think the reason or the source matters not. Somebody is hoarding gold in a major way and that’s almost certainly because they believe something is wrong with the system and they’re preparing for it. Gold might be overbought at the moment, but the implications of the trend are clear.

As mentioned, three of the magnificent 7 components - Facebook, Alphabet and Apple - are reporting earnings this week. Big tech earnings have generally done a pretty good job of supporting asset prices in recent quarters and it may very well happen again, but there are risks. Apple, in particular, looks like it’s losing some share and it might be vulnerable to the same issues that befell Netflix earlier. The other two have done a relatively reliable job of growing revenues. We’ve seen in recent weeks that the magnificent 7 can drag the major averages down in the same way that they pulled them up over the past year. We could see some added volatility during the latter half of this week.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.