The Delicate Balance

The Delicate Balance

Powell In Trouble

Powell is going to try to pull off a delicate balancing act at Jackson Hole - remaining hawkish enough to ensure that inflation gets back below the 2% target, yet remaining dovish enough that investors don’t feel like the economy could fall off a cliff. With headline inflation rates down into the 3-4% range, I’m guessing that buys Powell at least some time so that he can focus on the latter more than the former. Still, the Fed’s higher for longer plan on monetary policy almost certainly remains intact here and that could be trouble as the lagged effects of previous policy decisions start to become more evident. A lot of people are still talking about a soft landing or no landing outcome and I don’t think they’re anywhere near appreciating the tighter conditions that are still yet to come over the next 9-12 months.

The issues within both the banking and commercial real estate sectors continue to seemingly get worse by the week. S&P Global this week cut its ratings on several banks citing high commercial real estate exposure and more challenging operating conditions. This follows on the heels of what Moody’s did just a few weeks ago, although the impact this time around spilled over into the big banks as well. This is another prime example of “slowly and then all at once” that investors still aren’t prepared for. The S&P 500 is about 4% off of its recent peak, but the major equity averages still aren’t showing a particularly negative tilt given the credit risks that are continuing to build here. The commercial real estate sector, in particular, looks like it’s in real trouble and any financial institution that’s significantly exposed to it runs the risk of getting hit hard. Even without China sitting in the background, U.S. real estate is likely to keep deteriorating here until credit spreads finally start pricing in some risk and volatility picks up.

I’m still watching Treasuries for a turnaround, but I’m not sure Powell will give the bond market the ammunition for it this week. I’m expecting his speech will emphasize growth with a confirmation that inflation is slowing. This could be a trend of investors capitulating on safe haven assets one last time before a risk-off event sends yields plunging again.

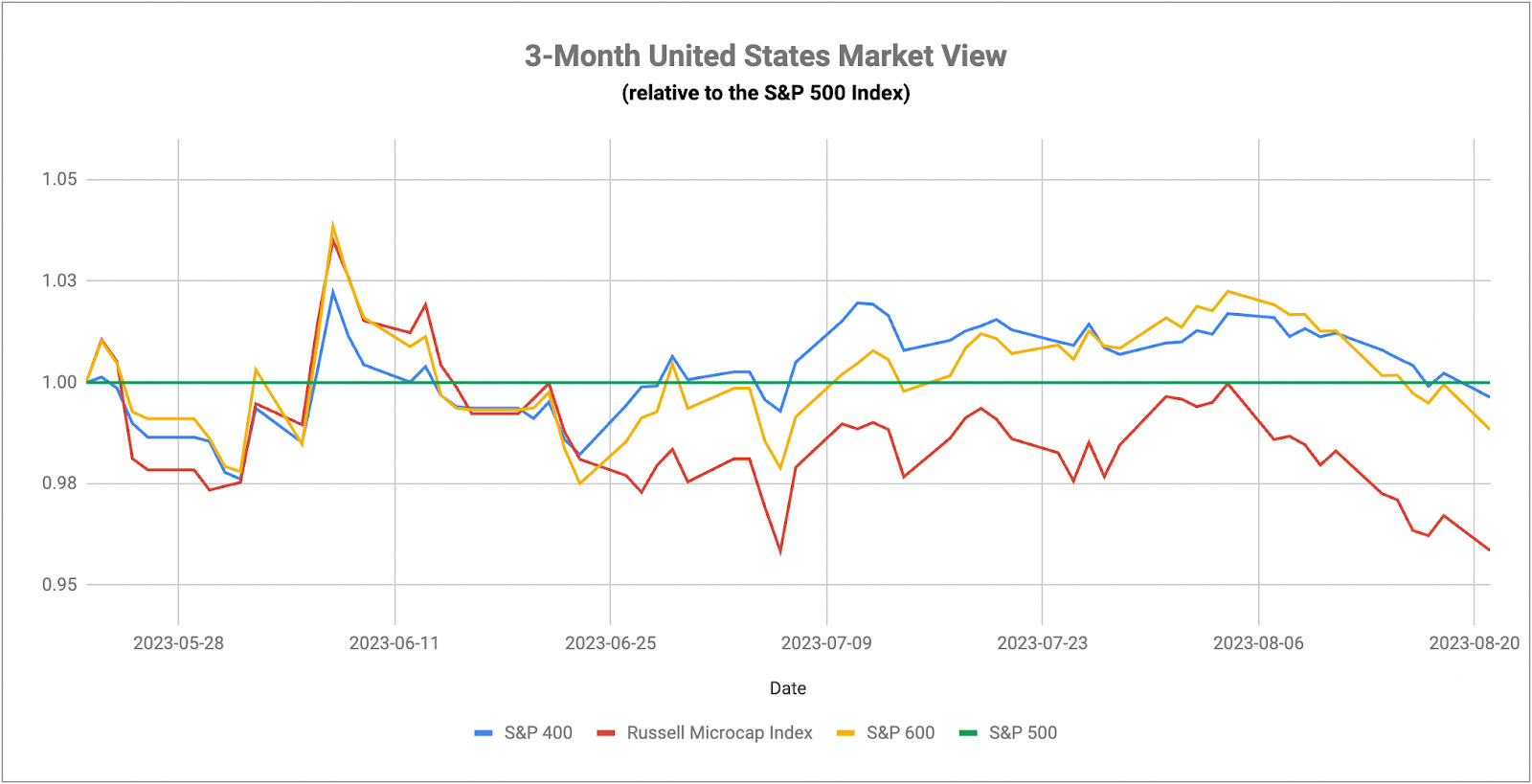

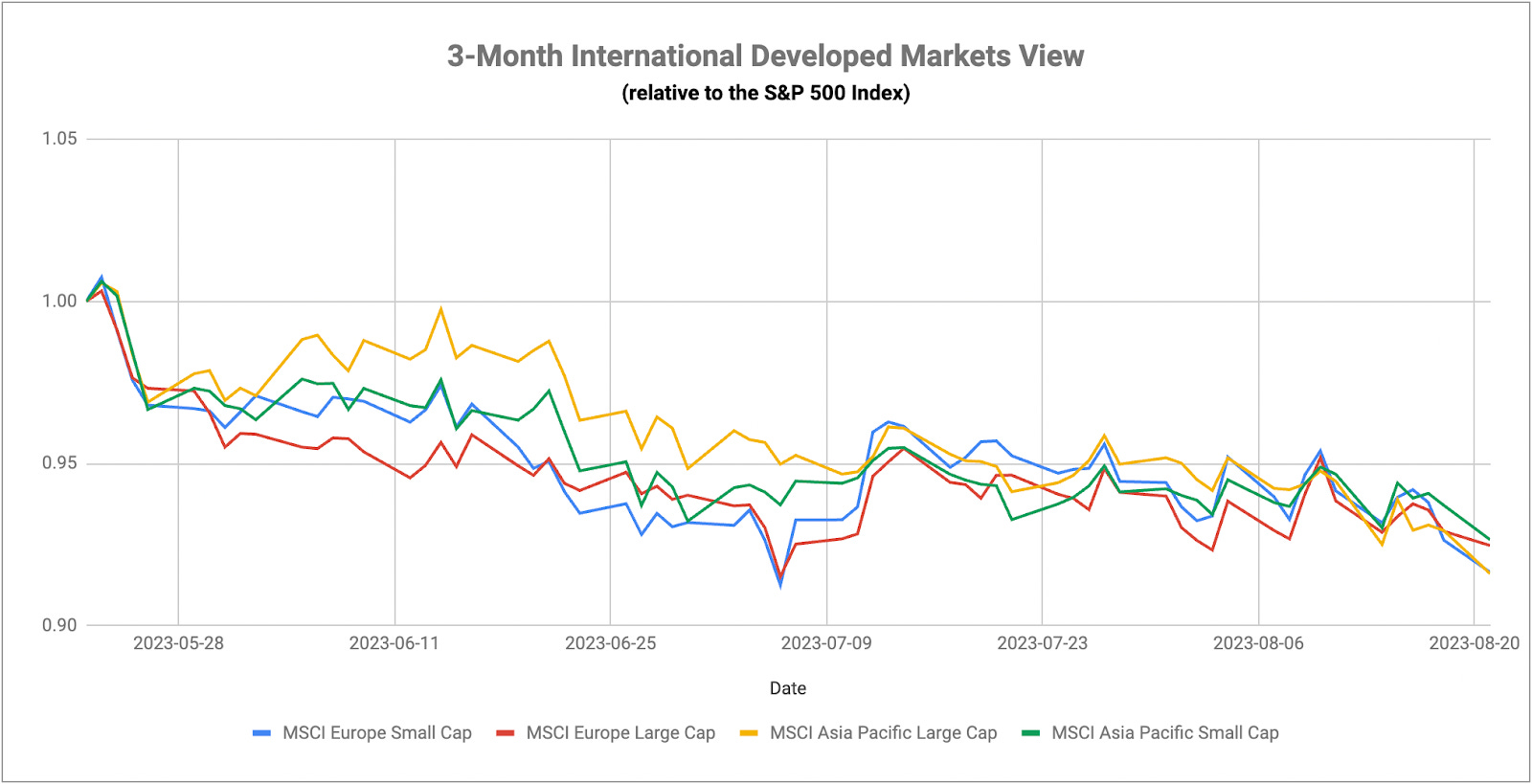

With Jackson Hole in focus in the United States, market watchers will naturally try to figure out what other global central banks will do with their respective policies.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.