The ECB Is Next

The ECB Is Next

And South Korea Gets Quite Interesting

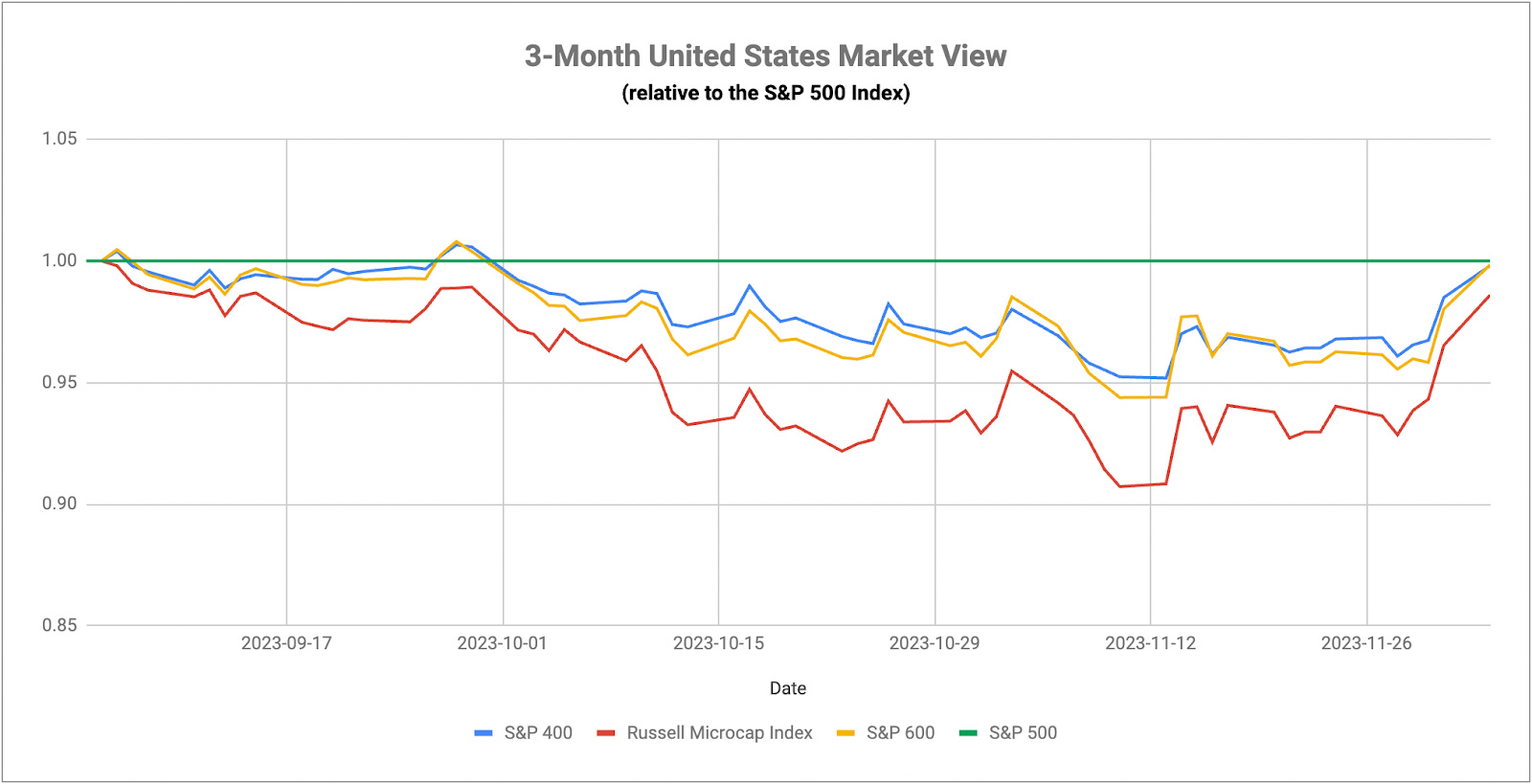

November delivered big gains for both equities and long-term Treasuries, but December, thus far, has presented a bit of a different narrative. There’s been a fairly decisive shift from large-cap growth & tech to small-caps, value stocks, cyclicals and long duration Treasuries. In reality, this is a trend that’s been building over the past few weeks and comes in the follow-up to the Fed’s neutral stance and cooling inflation trend. Investors seem to be buying more and more into the soft landing narrative that would be fueled by Fed rate cuts, currently anticipated to start as early as March. Cyclicals and value stocks tend to outperform in early stage economic recovery cycles, but the question now becomes is this a genuine turn or just a fake-out before the approach to recession?

The tell might come from small-caps, but not in the way that many may think. On the surface, investors view small-cap leadership as a bullish sign that riskier investments are outperforming. Right now, small-caps are being swept up in the cyclical recovery trade. Back during the tech bubble, small-caps led large-caps heading into recession as investors began seeking out cheaper stocks to provide downside protection against losses in overpriced large-cap tech. Sound familiar? The fact that small-caps are currently leading at the same time that the Nasdaq 100 and the “magnificent 7”, in particular, are lagging the market as a whole doesn’t seem like a coincidence. I’ve been pounding the table on X/Twitter that small-caps hold the key here and they could be signaling that the bear market isn’t over yet.

The non-farm payroll report will be what everybody is watching this week and could be a key trigger for a major event happening yet this year. We already know that job creation has been slowing for a while. The October jobs added number was the second lowest since the start of 2021 and missed expectations by a wide margin. This week, the October JOLTS number also came in at its lowest level since early 2021 and has steadily been trending lower for nearly two years (although it has some ways to go yet to get to pre-pandemic levels). Clearly, the labor supply/demand imbalance is nowhere near what it was even a year ago and is quickly approaching the neutral level again. In general, the month-over-month jobs added number tends to turn negative just ahead of the onset of a recession. We’re not there yet, so a recession may not be imminent, but that doesn’t mean that a shock to the system isn’t. Another below forecast number coupled with slower wage growth could fuel worries that a slowdown is happening at a faster rate than anyone is expecting. Since labor market strength is the one thing that’s been propping up optimism at this point, it could trigger a huge reversal when it finally breaks.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.