The Fed Just Confirmed That A Credit Event Is Coming

The Fed Just Confirmed That A Credit Event Is Coming

The Confession

At this week’s Fed news conference, Jerome Powell took a hawkish stance once again. While the market was hoping (expecting) that Powell was going to say that we’ve hit the terminal Fed Funds rate, he decided to throw another curve ball. He explained instead that one more rate hike was likely before the end of the year and the markets reacted accordingly. While stocks and long-term Treasuries were little changed in the immediate aftermath of the rate announcement, they both quickly turned south and carried that negative momentum into Thursday. Both have lost more than 2% since the Fed meeting.

The thing I found most concerning on Wednesday was Powell’s tone when he was speaking. It was confidence with a little arrogance sprinkled in. Cocksure that every step the Fed has taken thus far is going to thread the needle and achieve an idyllic outcome for the U.S. economy.

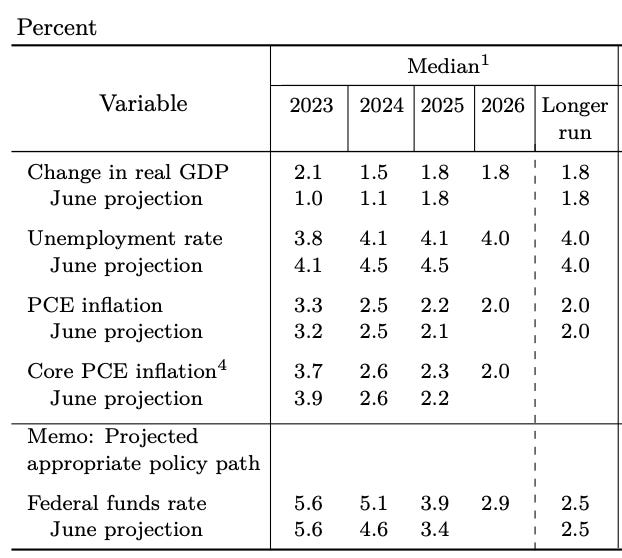

Let’s start by taking a look at the latest projections from the Fed and see if you can find a theme.

Compared to their June projections, the Fed has adjusted growth projections higher, the unemployment rate lower & core inflation lower (and eventually down to a modest 2.6% rate next year). In other words, the Fed thinks it’s going to pull off the soft landing that the market pretty much has priced in at this point. Powell said, “What we have right now is what’s still a very strong labor market that’s coming back into balance. We’re making progress on inflation. Growth is strong.”

In other words….

That’s what Powell’s saying publicly at least. Atlanta Fed President Raphael Bostic, however, may have just spilled the end game and it sounds like they may know what’s coming.

At a recent conference in South Africa, Bostic said the following…

“We have a lot of existing debt out there that is at very low prices. When that comes due, they’re not going to be able to refinance into comparable prices. There’s going to be an adjustment that needs to happen on that. So I actually think there’s a shaking out that’s about to happen at all levels.”

Read that last statement again. There’s a “shaking out” that’s about to happen “at all levels”. That sure sounds like a credit event to me. I think they know it’s coming and they’re going to let it happen.

This is exactly what I’ve been warning about for months, especially the part about refinancing debt. A lot of this short-term corporate debt is about to mature over the next year or two and it’s going to need to be rolled over into debt. Only this time, the rate is going to be about 5% higher than it was before. This was one of the events that I felt was going to potentially push corporate credit over the edge. Bostic essentially confirmed that something like this is coming.

The other problem is that I think the Fed is actually losing the narrative that inflation is coming under control and a soft landing is likely. They’ve already hiked by more than 500 basis points and we still have well-above average inflation, healthy GDP growth and a tight labor market. Granted, some of those rate hikes have yet to be felt and those numbers will start trending more negatively, but it may not happen soon (just look at the latest initial jobless claim numbers). If policy adjustments still haven’t moved the needle that much on inflation control and you want to bring it back down the hard way, what better way to do it than let the credit market do it for you.

Investors might already be seeing through the Fed’s public stance on inflation.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.