The Global Credit Event Looms

The Global Credit Event Looms

Path.

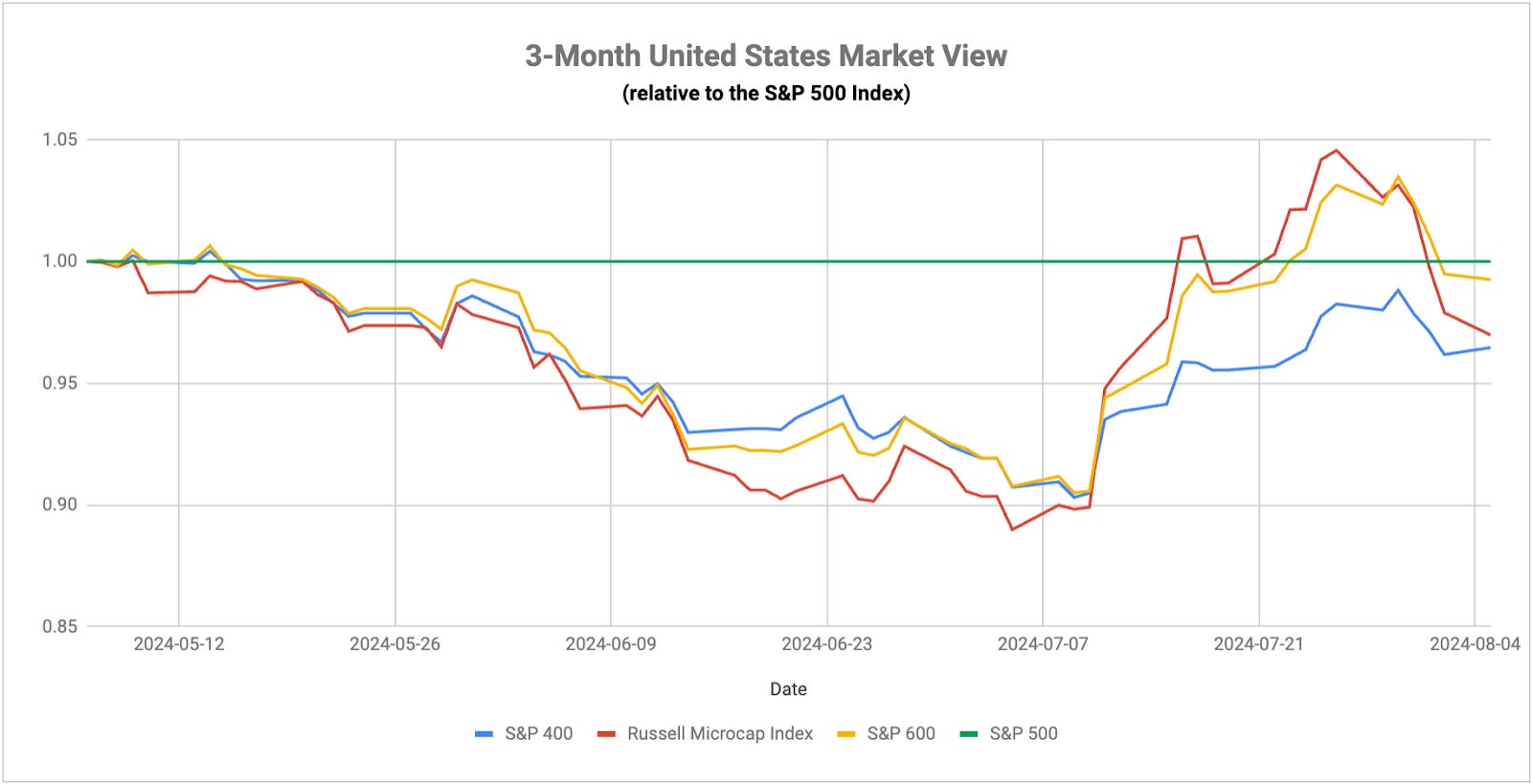

I think the chart above pretty much sums up the U.S. equity market in 2024. Months of dominance from the mega-caps. A cooler than expected inflation reading in early July triggered a massive rotation within equities that ignited one of the biggest small-cap rallies ever. And then just last week - a BoJ rate hike, another Fed hold and a bad jobs report - triggered a huge deleveraging of tech stock positions and the return of the flight to safety trade.

I’ve been talking about the risk of the reverse yen carry trade for roughly a year. These massive one-sided trades usually just need a small catalyst, a small push, in order to turn really ugly, really quick. Turns out it was a 15 basis point rate hike from the Bank of Japan, a surprisingly hawkish tone and the threat of future rate cuts to do it. A rising unemployment rate and slowing inflation rate were just the undercards in all of this. Japan has always been the main event and the biggest risk to a global meltdown.

Now, both the Fed and the Bank of Japan are in really tough positions (the latter I’ll talk about below). Just a month or two ago, we were talking about the risk of cutting too early while core inflation was still hovering around 3-4%. But there was never really any consideration given to the threat of near-term recession, so stocks were able to keep moving higher. Fast forward and Powell is about to be forced to choose between causing damage to the financial markets and causing a lot of damage to the financial markets.

The decision to pause again in July is looking like a policy mistake. The Fed had the opportunity to cut slowly and steadily without disrupting the markets. Now it looks like they were caught off guard by the Bank of Japan rate hike and a surprisingly bad jobs report. If there was ever evidence that the Fed has no more ability to see the direction of economic conditions ahead than you or me, this is it. The damage in the financial markets has been done and the Fed looks like it’s behind the curve yet again.

So now the Fed can cut rates more decisively in September or even make an emergency inter-meeting cut (which I think is unlikely). But that would only further accelerate the reverse yen carry trade and probably drag stocks lower still. Or they could wait another six weeks and risk the labor market and credit conditions getting worse (and probably drag stocks lower). It’s almost a no-win situation for the Fed. The only thing that might salvage equities is some type of coordinated global central bank facility or swap line that ensures there’s enough liquidity available to prevent a breakdown. That would almost certainly send stocks higher in the short-term, but it could prove to just be a fakeout in the longer-term that sucks investors in one more time. We do know already that there’s more government liquidity on the way in the form of additional Treasury buying and the FX market is finally back to a net long position in Japanese yen contracts. That could add some stability in the short-term.

The real market risk is the severe mispricing in the junk bond market. The situation in Japan has finally instigated a significant widening of credit spreads, but the real blowout has yet to happen. As I write this, high yield credit spreads are at Q4 2023 levels. The latest spread as of Monday was 393 basis points, up 91 basis points in less than two weeks. While that’s a huge increase in a short period of time, that level is only average over the past 15 years. Historically, the 600 basis point mark is where the bad stuff usually starts happening. In the 2000s, every time the high yield spread broke through this level, it ended up blowing up to at least 800 basis points (it broke above 1000 basis points during the tech bubble and roughly 2000 basis points during the financial crisis). The only exception was 2022 when it came up near the 600 basis point mark but turned back lower. At current levels, there is still a LOT of room for junk bonds to be massively repriced lower. That’s the global credit event risk that still looms.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.