The Great Dollar Comeback

The Great Dollar Comeback

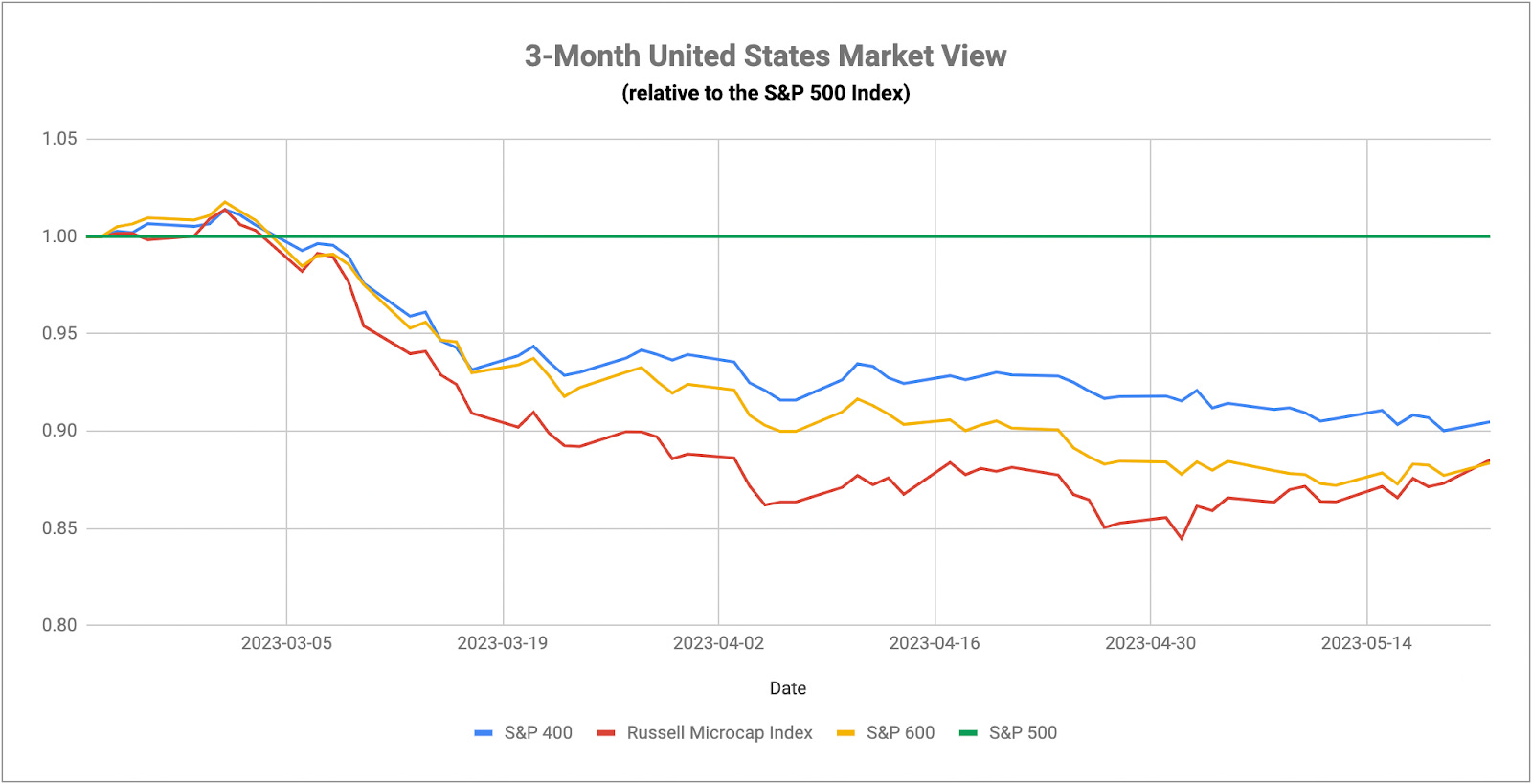

Opposing Forces Battle for Currency Supremacy

The debt ceiling has become a tiresome topic to talk about, but it can’t be ignored either. We’re down to one week left until the June 1st deadline, but the markets have yet to react in any meaningful way. Bond market volatility has remained elevated but steady over the past month. Save for a single day earlier this month, the VIX has been below 20 since late March. Not exactly the investor panic that looked possible based on what happened in 2011. We may get a volatility spike yet, but the overwhelming consensus that there’s no real chance that the government will default on its debt is likely contributing to the sense of calm. The real unknown at this point is what the ultimate resolution will look like. A series of major spending cuts could lead to a more dour economic outlook, but another increase in debt spending pushes us closer to the fiscal cliff. As much as I believe that market risk is being underappreciated here, there’s a possibility that risk assets produce another rally once a debt ceiling deal is reached.

While the cash markets are still expecting interest rate cuts in the 2nd half of the year, the Fed is doing its best to warn investors that this likely won’t be the case. Kashkari has already said that a June pause doesn’t mean that we’re at the end of the hiking cycle. Bullard, although he is currently a non-voting member, thinks that two more hikes would be appropriate given current conditions. That sure doesn’t sound like a committee that’s ready to pivot monetary policy back in the other direction. While I think the Fed has probably overtightened already considering the lagged effect of interest rate increases in the economy, it's also tough to make the argument that they should be cutting with inflation still running at a 5% annualized clip. The markets will see the headline rate drop up until the June reading. After that, it’s likely to move higher again and stay there through at least the end of 2023 barring a significant slowdown in the meantime. Is that a risk-off catalyst for complacent investors who think we’ll soon be back to the Fed’s 2% target rate?

The latest round of economic data pretty much confirms what we already know - the economy continues to expand, but it’s being driven entirely by the services sector. The May U.S. Composite PMI came in at 54.5, the 5th consecutive month it’s moved higher. The services PMI also moved higher for the 5th straight month, but manufacturing badly missed its forecast and slipped back into contraction. This isn’t all that surprising given what we’ve been seeing in lumber and industrial metals prices. Both are indicating a lack of demand for goods and factory output. I think it’s safe to say at this point that while China continues to expand following the end of the COVID lockdowns, the recovery hasn’t been nearly as swift and robust as the markets had been hoping for. I’m a big believer in lumber as a signal and that means conditions don’t favor a sudden rebound for the manufacturing space. Wage growth may support services activity for a while longer, but soaring credit card debt, higher rates and warnings from most of the big retailers suggests that this may not last.

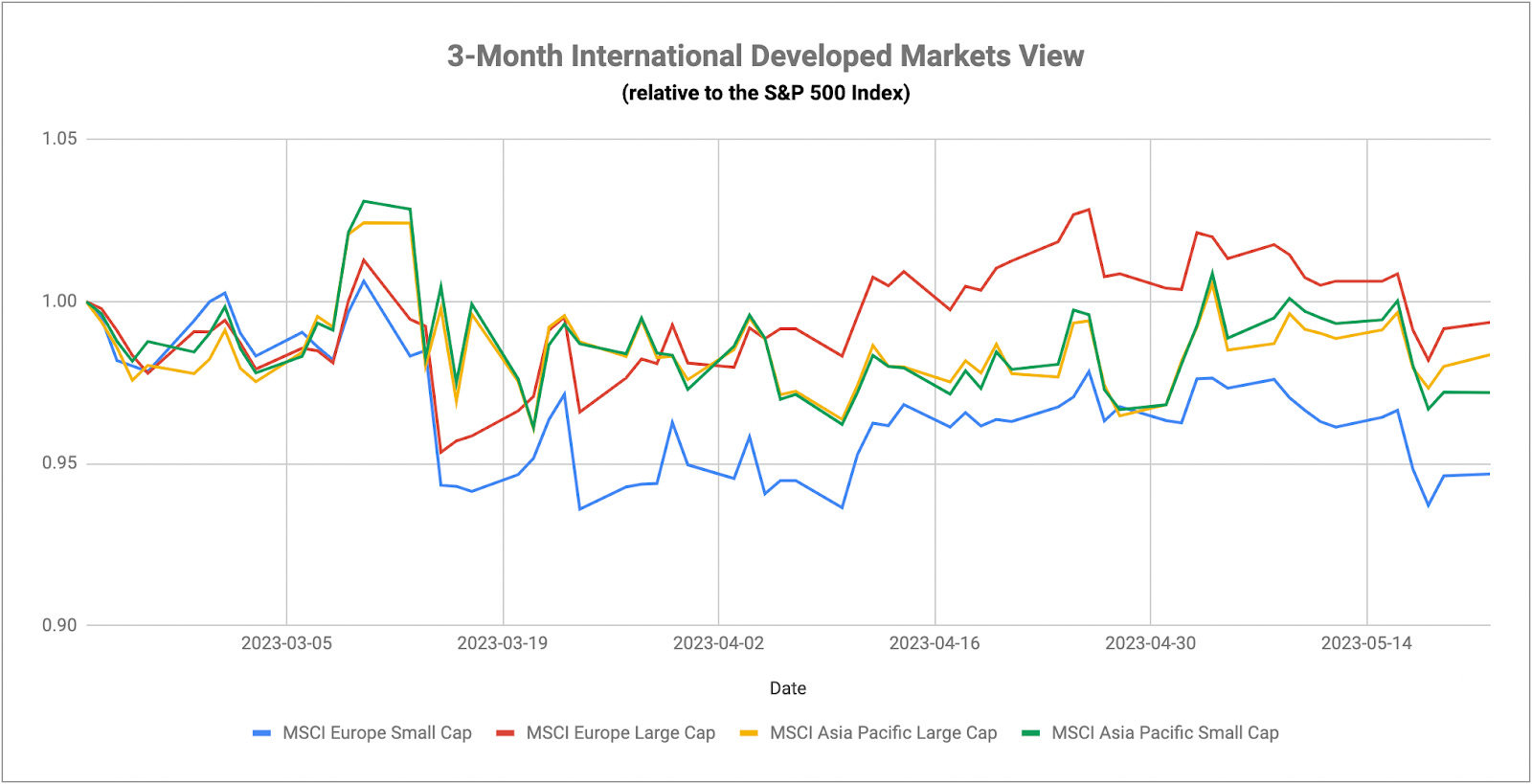

Could Japan finally be on the road to recovery?

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.