The Lost Decade: Zero Real Returns

The Lost Decade: Zero Real Returns

While The Rich Get Richer

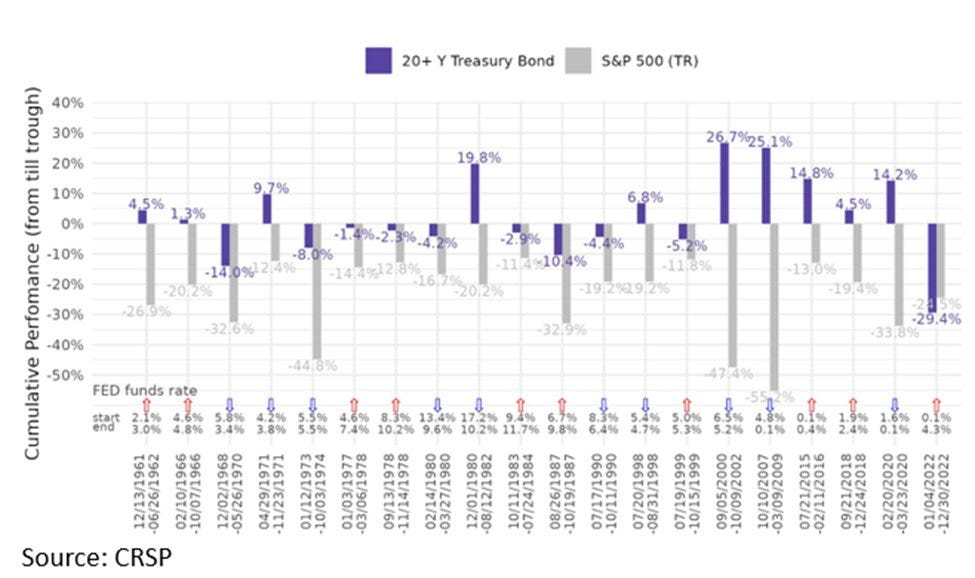

2022 will be remembered as one of the worst years for the financial markets as a whole in history. Sure, there have been periods where the S&P 500 fell a lot more than the 24% peak-to-valley drawdown last year, but we’ve never seen a time where both stocks AND bonds fell by this much at the same time. I’ve used the following chart often on Twitter, but it bears posting again.

We often hear and read about the benefits of asset allocation strategies because of how the two primary asset classes used are often negatively correlated. If one goes down, the other usually goes up. This helps diversify away some avoidable risk and smooth out the path of long-term returns.

2022 was one of the few times where the 60/40 portfolio failed to deliver. This has been the bane of my existence for the past few years - the fact that the risk-off asset didn’t behave at all like a risk-off asset. You’d probably have to go all the way back to the stagflation 1970’s to find another period that even resembles 2022.

Investors are in a lot better mood in 2023. The U.S. economy has remained resilient far longer than originally expected. Inflation is coming down. The Fed is at or near the end of its rate hiking cycle. Long-term Treasuries are still roughly flat on the year, but the S&P 500 is up 18% on the year and the Nasdaq 100 is up more than 40%. Even economic red flags, such as the number of corporate bankruptcies, soaring credit card balances, a near government debt default & the corresponding credit downgrade, the Chinese real estate crisis or the failure of Silicon Valley Bank, haven’t done much to put a dent in investor confidence. The major U.S. averages haven’t yet recaptured all-time highs, but they’re within a few percent of doing so, which has a lot of folks talking about the beginning of a new bull market.

Should they be so optimistic? Ehh, not so fast!

There’s that pesky little issue of inflation to consider. The goal of investing in equities, fixed income, real estate or anything else is to generate above and beyond the cost of living. Bonds, for example, have historically generated around a 1-2% real return. Stocks are closer to 4-6%. Nominal returns, which are what’s plastered all over the financial media, are great, but it’s inflation-adjusted returns that matter. If inflation is 8% and your investments only return 6%, you’re still coming out behind. That’s a consideration that a lot of investors are missing today.

This has especially been the case with asset allocation portfolios, the 60/40 being the one most commonly quoted. A lot of people declared the 60/40 portfolio dead over the past few years because interest rates were pitiful and they were generating very little return. 2022 made things even worse and, while yields are now at the point where fixed income and cash are once again viable fixed income options, the road to get there has been painful.

If you look beyond the success of equities this year, beyond the bear market of 2022 and even beyond the COVID recession of 2020, we find that investors running conservative and moderate strategies in their portfolios haven’t been coming out ahead for years.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.