The Massive Refi Explosion

The Massive Refi Explosion

Watch Delinquent Loans

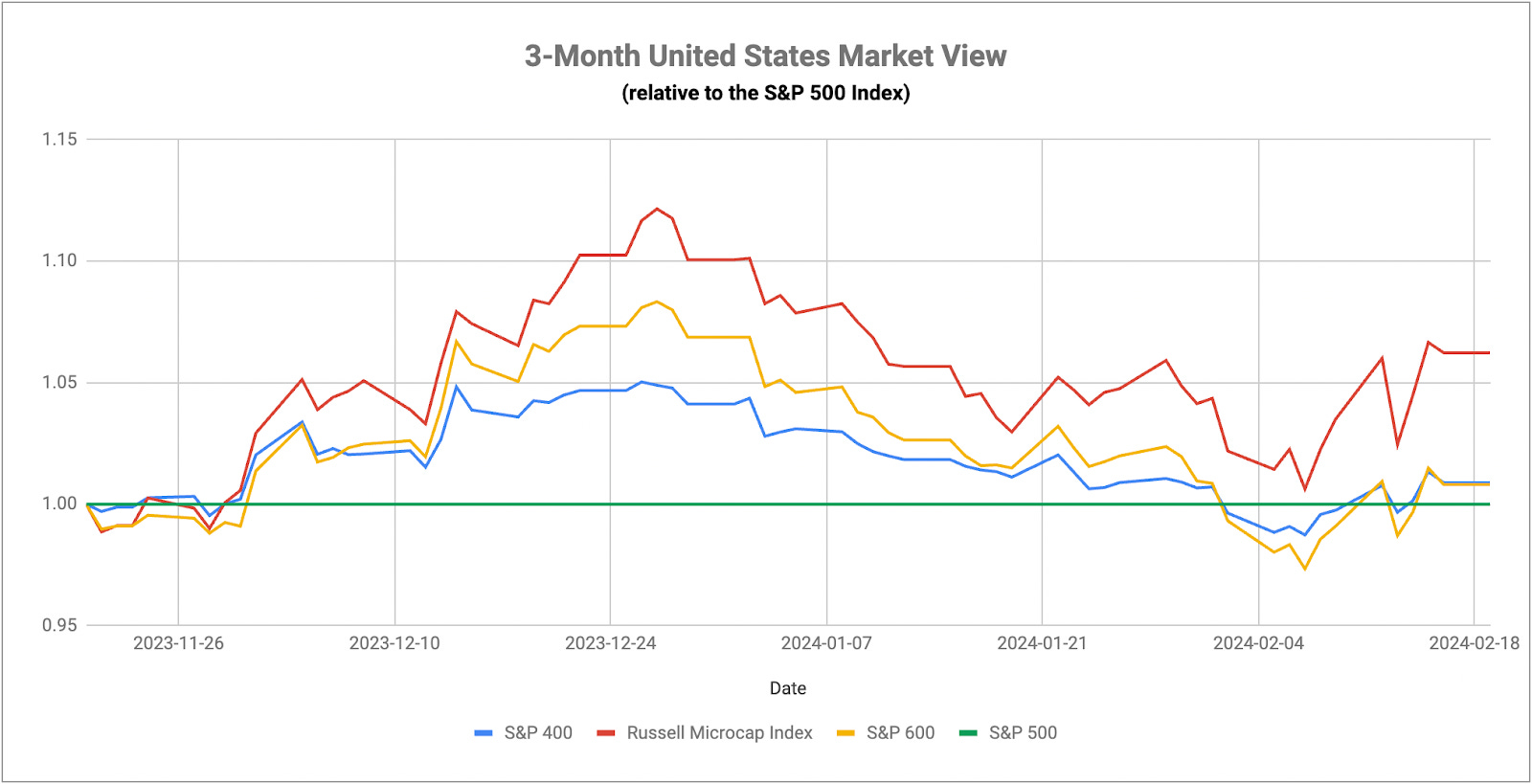

The major averages are starting to level off here, a sign that investors are removing the most bullish expectations from their 2024 outlooks and acknowledging the fact that the Fed won’t be instituting rate cuts any time soon. That’s mostly being reflected in long-term Treasury rates, where the 10-year yield has risen by more than a quarter-point off of the February low. Negative Treasury yield spreads have shrunk considerably since last summer, but they’re also nowhere near normalizing. For all of the expectations for a soft or no landing outcome here, the bond market is still showing a fairly significant disconnect between current conditions and forward-looking expectations.

While the signals have been correctly giving the green light for investors, a plethora of longer-term concerns, including commercial real estate, rising debt burdens and unsustainable consumer spending, still remain. The signals may be slowly picking up on that change in sentiment, particularly with utilities. Over the past week and a half, utilities have been sharply outpacing the S&P 500, essentially confirming the broad pivot to defensive investing that has occurred in response to the January inflation numbers. If last week’s sentiment carries forward into this week (early returns so far show that it is), March could be the time when we finally see a broader shift to risk-off conditions. Lumber/gold is already indicating that it could be ready to turn with prices for both assets holding up well lately. That would be both a short-term and intermediate-term signal flipping to risk-off in the early part of March and that’s when we really need to start paying attention to risk management.

Not that I want to get too deep into individual earnings reports, but the commentary coming out of Home Depot’s Q4 numbers was particularly interesting. Same store sales are still falling and the company issued disappointing guidance again, but they also noted that they see demand conditions normalizing again. This may be anecdotal or it may be a sign of a broader shift, but it generally runs counter to a lot of what we’ve heard regarding consumer weakness and falling demand. They did note, however, that the increased demand is coming on the services side, not the goods side. The desire to start new home improvement projects is getting delayed and that’s a direct reflection of higher interest rates and the lagged effects of the Fed’s rate hiking cycle. The slowdown resulting from tighter monetary conditions is definitely here and we may see this trend continue well into 2024 as further lagged effects show up. The markets aren’t pricing in the first rate cut until at least June and that gives the economy plenty of time to continue slowing further before any easing impact from the Fed will ever show up.

Not much new on the CRE front that we’re not aware of already. According to the FDIC, delinquent commercial real estate loans at the big banks have tripled over the past year, while reserves for these loans are at multi-year lows. If you don’t realize that this is very likely going to end VERY badly, you haven’t been paying attention. And that isn’t even considering the massive refi bomb that’s soon going to be dropped on this sector.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.